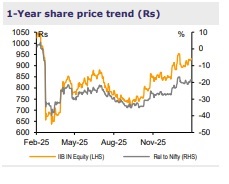

Buy IndusInd Bank Ltd for the Target Rs.1,100 by Emkay Global Financial Services Ltd

We upgrade IndusInd Bank (IIB) to BUY from Reduce while hoisting our TP by ~38% to Rs1,100 from Rs800. This is on the back of reinforced confidence on the new management’s decisive push on fixing structural gaps—reorienting the asset-liability mix, strengthening governance/internal controls, and rebuilding leadership, thus setting the stage for a sustained turnaround. IIB has turned profitable after a loss in 2Q and has given guidance for system in-line credit growth and an exit-RoA of ~1% in FY27. We expect the RoA to further improve to ~1.3-1.5% over FY28-29E, as the growth/asset-quality recovery gains further traction and thus drives a stock re-rating. Improving sectoral tailwinds (growth/margin/asset quality) and favorable sentiment toward large private banks should further aid IIB’s re-rating, akin to Federal Bank (also in the early stages of transformation). Accordingly, we boost our TP to Rs1,100, valuing the bank at 1.3x FY28E BV/11x FY28E EPS (based on the 2-stage Gordon growth model) vs 1x/9x Dec-27E BV earlier. Further re-rating will be contingent on sustained execution of the management strategy and no asset-quality/ regulations based interruptions.

Re-building leadership, business functions before re-accelerating growth After a sub-par 2003–08 phase, IIB saw sharp transformation under Romesh Sobti (then MD) for nearly a decade. However, over time, the pursuit of a higher RoA resulted in higher risks, balance-sheet inefficiencies, and weaker governance. Post the IL&FS crisis, Sumant Kathpalia took charge, though his tenure was volatile amid systemic shocks, microfinance stress, and then the derivatives fiasco – culminating in losses and senior management exits. Following a brief interregnum, Rajiv Anand, a veteran banker from Axis Bank, took charge in Aug-25. The new MD is rebuilding a senior leadership team with high integrity, strengthening credit-risk and HR functions, and rightfully integrating the asset-liability vertical in a ‘One IndusInd Bank’ framework. We believe this foundational reset will restore balance-sheet discipline and enable a sustainable recovery phase from FY27 onward.

Retail reset to deliver sustained healthy RoA/RoRWA IIB plans to recalibrate its business model, from a self-employed and commercial-retailheavy entity to a more balanced bank, with better focus on consumer retail, across both assets and liabilities. On the asset front, IIB plans scaling up consumer retail loans (gold, AFH, PVs) while capping MFI exposure at 7-8% (vs ~10% now). With an already strong branch network (better than Kotak’s), IIB’s strategic focus will be on improving branch productivity to mobilize deposits at lower CoF and reducing business sourcing from DSAs. This is likely to lead to healthier margin/core profitability without reliance on earlier highyield risky lending strategy. Parallelly, scaling up mid-corporate and SME businesses is likely to aid CA deposit claw-back and fee moat, thus supporting sustained RoA/RoRWA improvement to 1.3-1.5%/1.6-2.0% by FY28-29E from a low of 0.1%/0.1% in FY26E.

The IIB story – Repeated setbacks and turnarounds, but hopes abound for a sustained recovery now

Since 2003, IIB has witnessed repeated cycles of setbacks and turnarounds. Entering the millennium as a young PVB focused on corporate banking/VF, NRI deposits, and trade finance, IIB lacked a strong retail liability base. This resulted in weak margins, higher NPAs, and RoA at only ~0.2-0.4% during FY06–08. A sharp turnaround followed under Romesh Sobti (from Feb-2008), marked by rapid branch expansion, CASA rising from ~16% to ~44%, strong retail/VF-led growth, and RoA peaking at ~1.8% through to FY18. However, the aggressive push for profitability eventually coincided with rising risks, with cracks becoming visible around the IL&FS crisis in 2018 and persisting till 2020. The subsequent phase under Sumant Kathpalia (a protégé of Sobti from Mar-20) was marred by multiple shocks—Covid, Yes Bank contagion, MFI stress, and a derivatives setback—culminating in losses (4QFY25) and seniormanagement churn, thus exposing long-standing gaps in governance, risk management, siloed balance-sheet decisions, and a botched attempt at a turnaround.

With the appointment of Rajiv Anand (a veteran from Axis Bank), we believe there is bound to be a sustained turnaround of the once formidable retail bank (as seen during 2008-18). We believe that the bank does not need to be built from scratch, but requires restoring of the structural portfolio, bridging the leadership gaps, and strengthening the governance/internal controls. The new leadership has already initiated a balance-sheet clean-up to reduce assetquality risks from spilling over into FY27, while simultaneously rebuilding a credible senior management team, upgrading internal controls, and breaking internal business/departmental silos under a ‘One IndusInd Bank’ approach. The management has articulated an initial milestone of an exit-RoA of ~1% in FY27. Beyond this, we believe a re-orientation of the asset-liability mix toward consumer retail will help the bank deliver a sustainably healthy RaRoC. A clearer and detailed articulation of this medium-term strategy is likely to emerge post 1QFY27 results, and thus set the stage for a more durable recovery.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354