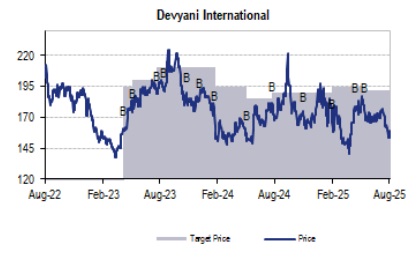

Buy Devyani International Ltd for the Target Rs. 192 by JM Financial Services Ltd

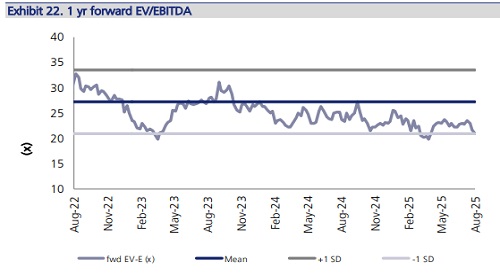

Weak demand and lower store openings across formats resulted in 3% miss to our 1Q revenue estimates despite consolidation of Sky Gate Hospitality (Biryani by Kilo - BBK) revenue for 20 days. The company added 8 stores in KFC while it closed 12 stores in PH. SSSG for KFC and PH declined ~1% and 4% respectively despite a weak base, resulting in 6- 8% decline in ADS in the formats. This along with (i) RM inflation, (ii) high marketing spends, (iii) GST on reverse charge basis on lower rentals, and (iv) higher off-premises sales resulting in higher aggregator expense led to EBITDA margin contraction of ~320bps YoY. The management remains cautious in terms of store openings and the focus is to drive higher SSSG and online sales. Higher compelling offers online led to 10% higher online transactions vs. dine-in and led to a positive SSSG in the delivery format. The company is looking to balance the offers/promotions in a manner that will avoid consumer shift from offline to online and also aid in positive SSTG. In BBK, the focus will be to first get the model right and achieve brand level profitability post which the brand will be expanded aggressively. Profitability in the international business was better vs. our expectations largely due to better gross margin in Thailand. We concur with the management’s strategy of driving higher transaction growth through more value offers/combo, which can impact margins in the near term but can help revive the ADS growth momentum, which is the need of the hour. Baking in the same, we cut our Pre-Ind AS EBITDA estimates by 4-10% as we cut our EBITDA margin estimates by 50-90bps. We maintain BUY with an unchanged TP of INR 192, based on 29x EV/EBITDA Pre Ind AS 116 as cuts in estimates are negated by roll-forward to Jun’27.

* Miss on all fronts: Consolidated revenue grew 11% YoY to INR 13.6 bn; 3% below JMFe despite consolidation of Sky Gate Hospitality from 10th Jun’26. EBITDA declined 8% YoY to INR 2 bn (12% below JMFe) as EBITDA margin contracted ~320bps YoY to 15.1% (JMFe: 16.7%) led by ~100bps contraction in gross margin to 68.2% (JMFe: 68.3%) and higher employee/other expense (~110/120bps YoY higher). APAT declined 93% to INR 27mn (JMFe: INR 143 mn) led by 13%/6% higher depreciation/interest expense partially offset by 36% YoY higher other income. Consolidated brand EBITDA declined 11% YoY to INR 1.8bn as margin contracted ~220bps YoY to 13.1%. Pre-Ind AS EBITDA declined 23% YoY to INR 1.1bn as margin contracted ~350bps YoY to 8.1% because corporate overheads grew by 50% YoY to INR 682mn (higher by ~130 bps YoY).

* SSSG & store additions still tepid; international margins above estimates: KFC revenue grew 10% YoY to INR 6.1bn (2% below JMFe) with brand margin at 15.5% (down ~410bps YoY; JMFe: 16.3%); it added 8 stores QoQ. Pizza Hut (PH) revenue grew 3% YoY to INR 1.9bn (5% above JMFe) and brand margin was -1.1% (down ~610bps YoY; JMFe: 1%); it closed 12 stores QoQ. Franchise brands revenue grew 14% YoY to INR 519mn (3% below JMFe) with brand contribution margin down ~200bps YoY at 13% (JMfe: 16%); it added 2 stores QoQ. KFC/ PH SSSG was -0.7/-4.2%. ADS for KFC/PH/Costa Coffee fell 6/8/7% YoY. International revenue grew 11% YoY to ~INR 4.3bn (2% below JMFe) with brand contribution margin at 16.7% (up ~190bps YoY; JMFe: 15.5%).

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361