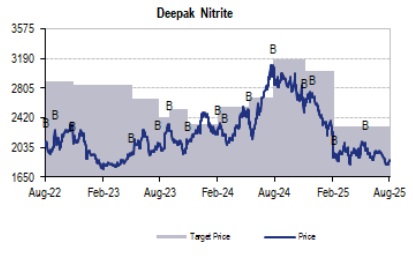

Buy Deepak Nitrite Ltd for the Target Rs. 2,265 by JM Financial Services Ltd

Deepak Nitrite’s 1QFY26 earnings print was weaker than our and consensus expectations due to less-than-expected sales. During the quarter, the company’s performance was weak on account of weakness in both advanced intermediates and phenolics segments. In phenolics, Deepak saw slight improvement in phenol spreads, with improvement likely to have continued in 2QFY26TD. In our view, volume in the AI segment is likely to normalise from 2HFY26. Moreover, backward integration capacities in AI segment including nitric acid, photochlorination are likely to improve AI segment margin from 2QFY26. On the phenolics side, benefits from commissioning of MIBK/MIBC and acetophenone capacities are likely to flow through from 3QFY26. Additionally, we are also building in some improvement in phenol-acetone spreads. Factoring in 1QFY26 performance and management commentary, our FY26-28 EPS estimates are revised downwards by ~4%. Since Deepak Nitrite’s long-term growth story remains intact with potential to more than quadruple its EBITDA over the next 5 years, we maintain our BUY rating on the name with a revised Sep’26 TP of INR 2,265/share (based on 30x Sep’27E EPS) (from INR 2,375 earlier).

* EBITDA miss due to less-than-expected sales: Deepak Nitrite’s 1QFY26 consol gross profit was 14% below JMFe at ~INR 5.3bn (down 21%/21% QoQ/YoY) as sales was 13%/11% below JMFe/consensus at ~INR 18.9bn (down 13%/13% QoQ/YoY) and gross margin was slightly lower than expected at 28% (vs. JMFe of 28.3% and 30.6% in 4QFY25). Other expenses came in lower at ~INR 2.3bn (vs. JMFe of ~INR 2.5bn and ~INR 2.5bn in 4QFY25). As a result, EBITDA was 28%/23% below JMFe/consensus and stood at ~INR 1.9bn (down 40%/39% QoQ/YoY) and PAT came in 32%/25% below JMFe/consensus at ~INR 1.1bn (down 45%/45% QoQ/YoY). In 1QFY26, Deepak Nitrite received Government incentive in one of its subsidiaries amounting to ~INR 172mn. Excluding this incentive, 1QFY26 EBITDA would be ~34%/30% below JMFe/consensus at ~INR 1.72bn.

* Phenolics and Advanced Intermediates EBIT lower than expected: Deepak’s Advanced intermediates EBIT was less than expected at INR 355mn (vs. JMFe of INR 549mn, INR 449mn in 4QFY25) as EBIT margin stood at 5.9% (vs. JMFe of 8%, 6.9% in 4QFY25) while revenue was lower than expected at ~INR 6.1bn (vs. JMFe of ~INR 6.9bn, ~INR 6.5bn in 4QFY25). Phenolics EBIT was lower than expected at ~INR 1.2bn (vs. JMFe of ~INR 2bn, down 51%/43% QoQ/YoY) as phenolics EBIT margin declined to 9% (vs. JMFe of 13% and 15.6% in 4QFY25) and revenue was below our estimates at ~INR 13bn (vs. JMFe of ~INR 15bn, ~INR 15.3bn in 4QFY25). The company indicated highest-ever production volume in phenolics in 1QFY26, which is likely to remain at that level in FY26.

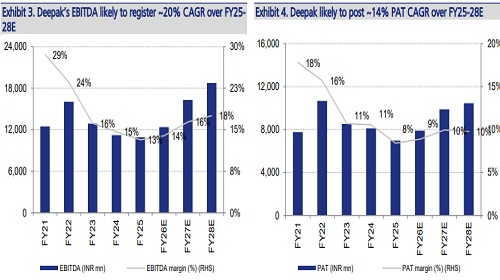

* Estimate 14% EPS CAGR over FY25-28E; maintain BUY: Factoring in 1QFY26 results and management commentary, we lower our FY26-28 EPS estimates by ~4%. We expect Deepak to register ~20% EBITDA CAGR over FY25-28E. Owing to sharp increase in depreciation from large capex, EPS CAGR is expected at ~14% over the same period. We maintain BUY with a revised Sep’26 TP of INR 2,265 (based on 30x Sep’27E EPS).

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361