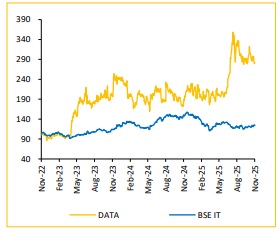

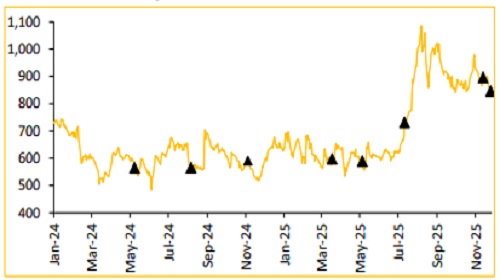

Buy Datamatics Global Services Ltd For Target Rs. 1130 - Choice Broking Ltd

Key takeaways from management meet

We interacted with the management team of Datamatics Global Services Ltd (DATA) comprising Mr. Rahul Kanodia, Vice Chairman & CEO, Mr. Ankush Akar, SVP & CFO, and Mr. Mitul Mehta, CMO. Key takeaways from the meet are; (1) Digital Operations business has scaled up meaningfully following the TNQTech acquisition, (2) The early-mover investments in AI, GenAI and Agentic AI are now translating into better traction within Digital Technology business (3) DATA’s strategy remains focussed on mid-sized client organizations with niche vertical leadership and enterprises undergoing business transformation. (4) The company serves over 300 active clients and sees significant growth opportunities in the US and Europe — with top client presence across BFSI, Publishing & Proctoring (Customer Experience), Retail and Logistics verticals. (5) DATA is actively scaling net-new client additions to lower concentration risk and strengthening its enterprise platform play through Microsoft, AWS, and newly added Salesforce capabilities via Dextara. (6) It plans to invest INR 400–500Mn annually in innovation to stay ahead of evolving technology landscape, while driving cost optimization to sustain profitable growth. We believe DATA’s niche vertical strengths, AI-driven execution and disciplined focus on profitable growth position it well for sustained performance. We maintain BUY rating with an unchanged TP of INR 1,130.

Niche vertical expertise scaled up by AI adoption in Digital Operations

RPA-led automation has evolved as enterprise data volumes surged, driving demand for complex document and workflow processing across ERP, CRM and SCM platforms. DATA now leverages Agentic AI within Digital Operations to automate processes which require reasoning, system-to-system interactions and swift decisionmaking. Key use cases span across content creation and publishing, human migration workflows, end-to-end insurance and underwriting, banking operations, travel and helpdesk services, and manufacturing processes.

AI-enabled KAI tools accelerating clients’ POC time-to-market in Digital Tech

DATA’s Digital Technology services span application development, modernization and maintenance, supported by in-house testing with 1–2-day POC turnaround. This enhances conversion of pilots into full-scale engagements. DATA is an early mover in AI, GenAI & Agentic AI through its Intelligent Automation suite—TruBot, TruCap and TruAgent—powered by proprietary KAI tools & accelerators built on the Kaizen philosophy of continuous improvement. KAI accelerators automate legacy logic extraction into modern architectures and enable real-time, data-driven decision-making across client enterprises, which we believe would drive faster scale-ups and superior delivery versus peers.

Digital Experience segment to grow with a lag as clients move to captives

Clients' captive shifts to weigh on Digital Experience in the near term, but DATA’s proven GCC build-and-run capabilities position it well as CIO-led decision centres migrate to India and Philippines for back-office operations.

Net-new logos to enhance scale over existing marquee clients

Large deal sizes are scaling up steadily from ~US$0.2Mn-$3Mn, with a visibility to expand into US$5Mn–$10Mn range. DATA is also focusing to grow net new clients in range of US$1Mn–$10Mn to gradually reduce dependence on its Top-20 clients.

Valuation – Maintain BUY rating with a TP of 1130

We maintain our financial estimates, supported by consistent execution discipline and expect Revenue/EBIT/PAT to expand at 11.8%/ 24.4%/ 16.4% CAGR, over FY25–28E. Thus, we maintain a ‘BUY’ rating on DATA with Target Price of INR 1130, based on FY27E and FY28E average EPS of INR 51.5, with a 22x PE multiple.

Key Risks

* High concentration risk, led by Top 10–20 clients at ~39–52% of topline

* Digital Experience recovery could modestly weigh on near-term growth

Optionality

DATA remains selective on M&A, targeting sustainable businesses aligned with its GTM strategy at reasonable valuations and with clear ROI visibility. Acquisitions remain focussed on enhancing technology capabilities and scaling up operations and client access — as demonstrated by Dextara (deal value scaled up from ~US$0.07Mn-US$3Mn post acquisition) and TNQTech, through which DATA now ranks 9th globally among publishing service-providers, strengthening content creation and publishing capabilities across both, offline and digital, channels.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131