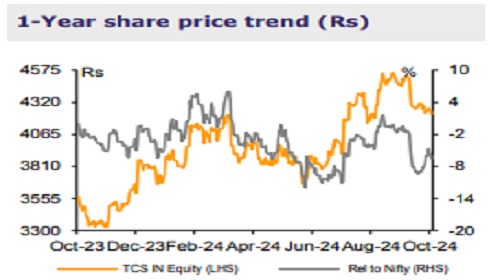

Reduce TCS Ltd for the Target Rs.4,500by Emkay Global Financial Services Ltd

TCS’s operating performance missed expectations in Q2. Revenue grew 2.2% QoQ (1.1% CC) to USD7.67bn, in line with expectation. Although, revenue composition was weaker than expected with higher-than-estimated contribution from the BSNL deal, partly negated by softness in mature markets. EBITM declined by 60bps QoQ to 24.1% and missed expectations. Deal wins were steady at USD8.6bn (book-to-bill ~1.1x) and remained within the guided comfort range of USD7-9bn per quarter. Management highlighted some signs of demand improvement, notably in BFSI in North America; however, weak discretionary spending, client-specific challenges, slower decision-making, and client’s cautious behavior amid macro uncertainties weighed on revenue growth. We cut earnings estimates by 1.2-2.4% for FY25-27 considering the Q2 miss. After ~5%/13% underperformance compared to Nifty IT index over 3M/6M, TCS’s relative valuation is not demanding. Given the lack of any nearterm trigger, we retain REDUCE with TP of Rs4,500/sh at 28x Sep-25E EPS.

Results Summary Revenue grew 2.2% QoQ (1.1% CC) to USD7.67bn, in line with our estimate. Cost of equipment and software licenses increased USD128mn QoQ, partly reflecting ramp up of the BSNL deal. EBITM fell by 60bps QoQ to 24.1%, below our estimate of 24.8%, due to higher third-party expenses and continued investments in talent and infrastructure, partly negated by currency benefits and absence of one-off costs. Among geographies, India, MEA, and APAC led growth with 21.3%, 7.3%, and 4.8% QoQ, followed by UK and Continental Europe which grew 2.8% and 3.6%, whereas North America declined 1.7% (in USD terms). Growth was led by Regional Markets & Others, ERU, BFSI, Consumer, and Technology & Services which grew 13.1%, 4.0%, 1.9%, 0.2%, and 0.9% QoQ. Communications & Media, Manufacturing, and Life Science & Healthcare declined 2.7%, 0.1%, and 3.4% QoQ. What we liked: Signs of recovery in BFSI, steady deal intake. What we did not like: EBITM miss, muted revenue growth excl. regional markets.

Earnings Call KTAs

i) The demand environment remains cautious with clients prioritizing spend on initiatives oriented toward cost optimization, which offer immediate ROI. The management though is hopeful of some recovery in Q4, led by gradual easing of inflation and interest rates, and a good holiday season.

ii) BFSI is seeing signs of improvement with growth in North America, Europe, and UK led by banking, insurance, and risk and compliance, while capital markets was a laggard. i

ii) Retail customers continue to follow a cautious approach owing to macro uncertainties. Consumer spending during the coming holiday season may lead to uptick in discretionary and overall tech spending.

iv) Manufacturing is seeing some pressure in the short term as labor and supply-chain issues are weighing on demand.

v) Life Sciences and Healthcare saw weakness in Q2 due to client-specific challenges also impacting growth in North America.

vi) CME continues to face growth headwinds. Interest rate cuts may be a trigger for higher capex spending by clients.

vii) There are over 600 AI/GenAI engagements (vs 275 in Q1) including 86 engagements moving to production in Q2 (vs 8 in Q1).

viii) BSNL deal is expected to maintain similar levels for another quarter before tapering down. Management expects improvement in margin as third party expense for the BSNL project tapers down in coming quarters. It is aspiring for EBITM at 26-28% in the medium term and exit EBITM of 26% for Q4.

ix) The management expects furlough impact in Q3 to be similar to last year

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354