Buy Mphasis Ltd for Target Rs. 2,625 by Choice Institutional Equities

AI-led Momentum Drives Resilient Growth

MPHASIS reported strong Q4FY26 performance, with 6% QoQ INR revenue growth and 2.5% QoQ CC growth, driven by steady execution and AI-led deal momentum. Deal TCV grew strong by 67.5% YoY in FY26 along with improved conversion rates. The underlying trajectory appears resilient, aided by a strong and expanding pipeline (+38%) led by BFSI. Mphasis’ NeoIPTM is exhibiting platform-led differentiation; winning through IP-led capabilities. Notably, the increasing mix of AI-led deals (69% of pipeline) signals a structural shift in demand, positioning MPHASIS well to benefit from enterprise adoption cycle led by growing AI opportunity. Accordingly, we expect Revenue/EBIT/PAT to expand at a CAGR of 12.2%/14.3%/14.2% over FY26–FY29E. We maintain our ‘BUY’ rating, with revised target price of INR 2,625 based on FY28E EPS of INR 131.3, implying PE of 20x

Revenue Strength Supports Steady Earnings Delivery

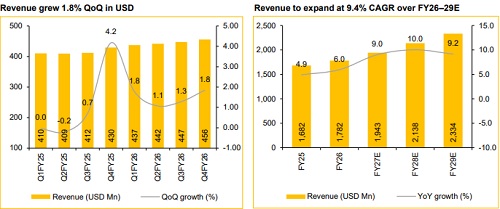

* MPHASIS reported Q4FY26 revenues in INR 42,427 Mn, up 6.0% QoQ and 14.4% YoY (vs CIE estimate of 4.7% QoQ). In CC terms, revenues grew by 2.5% QoQ and 7.1% YoY. For the full year, revenue in USD stood at USD 1,782 Mn, up 6.0% YoY, whereas, in INR terms, revenue clocked in at INR 158,796 Mn, up 11.6% YoY.

* EBIT margin expanded by 17 bps QoQ to 15.4% for Q4FY26 (vs CIE estimate of 15.2%). For the full year, EBIT margin came in at 15.3%.

* PAT for the quarter came in at INR 5,096 Mn, up 15.3% QoQ and up 14.1% YoY (vs CIE estimate of 10.1% QoQ). PAT for FY26 came in at INR 18,626 Mn, up 11.7% YoY. EPS stood at INR 26.7 in Q4 and INR 97.5 in FY26.

AI-led Deals Drive Pipeline Strength Despite Near-term Softness

MPHASIS won new deals (including four large wins) with TCV of USD 407 Mn in Q4FY26, down 4.9%, of which 64% is AI-led. For the full year, deal TCV stood at USD 2.1 Bn, up 67.5% YoY, of which 60% is AI-led. The overall pipeline value increased 38% YoY, with BFSI driving growth with 13.4% QoQ, Healthcare and others segment grew at 5.1% QoQ driven by recent deal wins in healthcare. On the other hand, TMT (-10.4% QoQ) & Logistics (-3.6% QoQ) experienced nearterm softness due to project completions and delayed decision cycles; and revenue restructuring from a large global client respectively. We believe that MPHASIS continues to leverage on strong pipeline momentum supported by disciplined execution. Additionally, with ~69% of the pipeline is now AIled, which reflects a structural shift in client demand towards AI-driven transformation, for which MPHASIS is well-positioned.

Margins Hold Steady Amid Near-Term Hedge Pressures

Q4 EBIT margin expanded by 20 bps sequentially to 15.4%, while full-year margin remained stable at 15.3%. Margin tailwinds included FX gains, which were offset by hedge losses, excluding which the margin would be significantly higher at ~16.5% for Q4. The management expects the headwind from hedge losses to continue through at least H1FY27 before it tapers down. Any margin headroom created by operational efficiency is intended to reinvest back in business mainly on AI capabilities (specifically Decision Intelligence stack), sales GTM, and leadership. The company remains committed to operating within its stated target band of 14.75% to 15.75% for FY27.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131