Buy Biocon Ltd for the Target Rs.450 by Motilal Oswal Financial Services Ltd

Temporary constraints weigh on performance

Launch traction key to unlocking operating leverage in biologics/generics

? Biocon (BIOS) delivered lower-than-expected financial performance for the quarter. Temporary constraints in the biologics and CRDMO segments impacted revenue for the quarter.

? Re-prioritization of high-margin products in the biologics segment was offset by operating deleverage during the quarter. ? BIOS has about four molecules with USD200m+ annual sales in the biologics segment. It has disclosed three biosimilar assets, which are a work-in-progress. These products are scheduled to lose exclusivity over the next five years.

? The Generics segment continues to scale from new launches and market share gains in existing products.

? Regarding the CRDMO business, BIOS has expanded its commercial capacity and chemistry capabilities.

? We reduce our earnings estimate by 4%/4%/5% for FY26/FY27/FY28 to factor in: a) manufacturing constraints for one of the customers in the CRDMO segment, b) a gradual scale-up in the biologics business, and c) higher opex from recently commissioned facilities in the generics segment.

? We value BIOS on an SOTP basis (22x 12M forward EV/EBITDA for the Biologics business, 53% stake in Syngene, and 10x EV/EBITDA for the Generics business) to arrive at a TP of INR450.

? BIOS has built considerable capacity across major segments. The operational cost is largely baked in. Product launches and commercial traction remain the key. We expect a 39% earnings CAGR over FY26-28. Reiterate BUY.

Geography/segment mix benefit offset by lower operating leverage

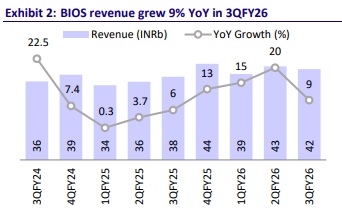

? BIOS's 3QFY26 revenue grew 9.2% YoY to INR41.7b (est. INR45.4b).

? Gross margin (GM) expanded 350bp YoY to 65.5%.

? EBITDA margin contracted 60bp YoY to 20% (est: 19.7%) (employee expenses/other expenses rose 55bp/280bp YoY as a % of sales). R&D costs inched up (75bp YoY as a % of sales) for the quarter.

? EBITDA grew 6.1% YoY to INR8.3b (est: INR8.9b). ? BIOS had an exceptional expense of INR3b related to: a) one-time employee expense w.r.t. changes in the labor code (INR1.7b), b) advisory and legal consultancy, premium on hedges, and bridge financing costs (INR2.2b), c) provision for liquidation of inventories (INR762m), d) fair value change of investment (INR50m), and e) gain on remeasurement of the derivative liability related to Mylan Inc.’s investment in BBL (INR1.8b).

? Adj. for the same, PAT came in at INR1.2b (est. INR1.6b) vs INR439m YoY.

? In 9MFY26, Revenue/EBITDA grew 14%/16% YoY, while PAT came in at INR2.5b, compared to a loss of INR800m in 9MFY25.

? Revenue growth was led by Biosimilars (58.5% of sales), rising 9.4% YoY to INR25b. Research services (21.5% of sales) declined 2.8% YoY to INR9.2b. Generics (20% of sales) rose 24% YoY to INR8.5b.

? Biocon Biologics' EBITDA was INR7b, with margin at 27.9%, up 560bp YoY.

? Syngene's (Research services) EBITDA margin was 24.4% for the quarter, down 750bp YoY.

? This implies a generics EBITDA margin of 3.1%, down 250bp YoY.

Highlights from the management commentary

? BIOS recently submitted the Pertuzumab (b-Perjeta) filing with the USFDA.

? The company has reiterated annualized interest cost savings of INR3b from FY27 onwards.

? It has taken certain steps to upgrade operational/manufacturing facilities in the biologics segment, impacting growth in 3Q.

? BIOS indicated EBITDA margins of mid-20s in the biologics segment in FY26.

? Given the commercial success of Adalimumab, with annualized sales of USD200m+ and potential to gain further business, BIOS has acquired full global rights to the product.

? In the generics segment, while the addressable market for liraglutide is declining, the product continues to offer a potential opportunity for BIOS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412