Buy Avenue Supermarts Ltd for the Target Rs.5,000 by Motilal Oswal Financial Services Ltd

Acceleration in store additions to drive growth

* Avenue Supermarts (DMart)’s revenue growth trajectory improved to 19% YoY in 4QFY26 (vs. 15% YoY in 9MFY26), driven by acceleration in store additions (though most of it was back-ended) and likely recovery in SSSG (vs. ~6% in the last few quarters).

* While competitive intensity from Quick Commerce (QC) remains intense in the metros and tier 1 markets, we have maintained that the acceleration in store additions, especially given notable whitespaces in North and East India, remains the key trigger for DMart to revert to a 20%+ YoY revenue growth trajectory.

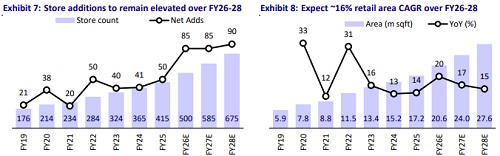

* The execution on store openings notably improved in FY26 with 85 store openings (vs. 50 in FY25 and the street’s expectations of ~60-65 stores).

* DMart added 46 stores in its existing cities while entering 39 new cities (out of which 34 were tier 2+ cities) during FY26, including entry into five new states (namely UP, Haryana, Odisha, Uttarakhand, and Goa) in FY26.

* The throughput in tier 2+ cities would likely be lower than DMart’s existing cities, but we believe the cost structure would also be lower, thereby ensuring returns are protected.

* Further, we believe that despite competitive intensity from QC, DMart’s gross margins have likely bottomed out in 1QFY26 (up ~5/50bp in 2Q/3QFY26), which could provide further upside to consensus estimates.

* We raise our FY27/28E EBITDA by 5-7% and PAT by ~2-4%, driven by higher store additions (85-90 stores annually). We now build in a CAGR of 19%/ 20%/16% in DMart’s consolidated revenue/EBITDA/PAT over FY26-28.

* We reiterate our Buy rating on DMart with a revised TP of INR5,000, premised on 45x FY28 EV/EBITDA (implied ~80x FY28 P/E).

Acceleration in store additions to fuel growth amid intense competition

* We have maintained that acceleration in store additions remains the key trigger for DMart, given that its high-throughput metro stores are either saturated or are facing intense competition from the QC.

* DMart accelerated store additions by adding 85 stores in FY26 (vs. ~50 in FY25 and higher than the street’s expectations of 60-65 stores), taking the total store footprint to 500 stores across 184 cities.

* DMart added 46 stores in its existing cities while entering 39 new cities (out of which 34 were tier 2+ cities) during FY26, including entry into five new states (namely UP, Haryana, Odisha, Uttarakhand, and Goa) in FY26.

* DMart’s store expansion in FY26 was fairly balanced between deepening presence in Metro/Tier 1 cities (40 stores, five new cities) and entry into tier 2+ cities (45 stores, 34 new cities).

* In metro/Tier 1 markets (~57% of DMart’s store base), the focus remains on operational efficiency measures such as reducing queuing, increasing billing capacity, improving service levels through staffing, and checkout efficiency.

* In contrast, tier 2+ entry is driven by the high resonance of DMart’s valuebased proposition and the lower competitive presence of QC companies.

Growth could revert to 20%+ in FY27; margin likely to have bottomed out

* Driven by acceleration in store additions to 20%+ (vs. ~13-14% YoY in the past few years), we believe DMart’s revenue growth could accelerate to more than 20% in FY27 (+19% YoY posted in 4QFY26, despite back-ended store additions).

* While the revenue throughput would likely be lower (vs. blended average) in some of the recently opened tier II+ cities, we believe lower competitive intensity bodes well for DMart’s value-focused model. ? We now build in ~19% revenue CAGR over FY26-28, driven by 85-90 annual store additions (~16% CAGR) and likely mid-to-high-single-digit LFL growth.

* Further, we believe that despite competitive intensity from QC, DMart’s gross margins have likely bottomed out in 1QFY26 (up ~5/50bp in 2Q/3QFY26).

* The sharp margin expansion in 3QFY26 was partly aided by GST-led benefits, but we believe a part of the benefit could be sustained as DMart has likely tweaked discounting on certain SKUs, which are not as relevant in QC.

* Additionally, DMart had front-loaded investments on improving service levels in high-throughput Metro/tier 1 cities to tackle the rising competition, and going ahead, the rising share of tier 2 expansion is likely to come at lower costs.

* We build in a modest ~5bp EBITDA margin expansion over FY26-28, with margins still lower than FY25, which could provide upside risks to our estimates.

Valuation and view

* Acceleration in store additions continues to remain the key growth trigger for DMart, in our view. We now raise our FY27-28 store additions to 85-90 stores (vs. 70-80 openings earlier), given significant white spaces in densely populated states such as UP, Bihar, and West Bengal.

* While the competitive intensity from QC could remain elevated in the near-tomedium term, we believe DMart’s value-focused model and superior store economics would ensure its competitiveness and customer relevance over the long run, especially in tier 2+ towns, where the potential for growth remains significant.

* We raise our FY27/28E EBITDA by 5-7% and PAT by ~2-4%, driven by higher store additions. We now build in a CAGR of 19%/20%/16% in DMart’s consolidated revenue/EBITDA/PAT over FY26-28, driven by ~16% CAGR in retail store/area and a mid-to-high-single-digit LFL growth.

* We reiterate our BUY rating on DMart with a revised TP of INR5,000 (earlier INR4,600), premised on 45x FY28 EV/EBITDA (implied ~80x FY28 P/E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041