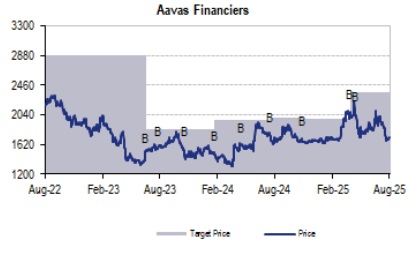

Buy Aavas Financiers Ltd for the Target Rs. 1,767 by JM Financial Services Ltd

In 1Q26, Aavas reported a miss of 13% on PAT at INR 1.4bn (+10% YoY, -9% QoQ) leading to RoA/RoE of 2.9%/12.6%. The miss was led by decline in NIMs (calc.) of -45bps QoQ and higher than anticipated credit costs of 22bps. AUM growth remained steady at +16%/+2% YoY/QoQ, however, disbursements declined by -5% YoY, -43% QoQ, driven mainly due to shift in accounting methodology to realize disbursements. Management highlighted that the disbursements will normalize from Q2 onwards. Headline asset quality saw seasonal weakening, with GS3/NS3 rising to 1.22%/0.83% (+14bps QoQ, +10bps QoQ). The deterioration was mainly due to seasonality and local stress in states such as Maharashtra, MP, and KA, particularly in the sub-INR 0.5mn ticket size loans which also led 1+DPD to rise up to 4.15% (+76bps QoQ). However, Jul’25 1+DPD has already gone down below 4% which suggests normalization in coming quarter. We believe that the current quarter was only affected seasonally in terms of growth and asset quality while we expect 2H to be stronger led by a) pick-up in growth momentum, b) margins stabilization with CoFs re-pricing and c) improvement in asset quality. We maintain BUY with a revised TP of INR 1,990 (valuing it at 2.9x FY27E BVPS vs 3.3x FY27E BVPS earlier) in return for avg RoA/RoE of 2.6%/12% over FY26E/FY27E.

* Steady growth: AUM growth remained steady at +16% YoY, +2% QoQ. However, disbursements declined by -5% YoY, -43% QoQ, driven mainly due to shift in accounting methodology to realize disbursements. Disbursement growth is expected to normalize from Q2 onwards as the cheques which are yet to be passed will be included in upcoming disbursals. This normalization is already evident in Jul’25 disbursements, which management indicated at INR 5.5–6bn (+15% YoY). AUM growth was primarily led by MSME segment (+66% YoY, +7% QoQ), while the HL portfolio remained flat QoQ. LAP grew +2% QoQ, -11% YoY. Management reiterated its FY26 AUM growth guidance of ~20–22%, with a further acceleration to 22–25% expected in FY27. We build in an AUM CAGR of ~18% over FY25-27E.

* Miss in operating performance and profitability: Operating profit was a miss at INR1.9bn (+12% YoY, -5% QoQ, -10% JMFe), primarily due to a sequential decline in NII (-3% QoQ, +18% YoY). The decline was driven by a -45bps QoQ compression in NIMs (calc.), which in turn was led by a -52bps QoQ decline in yields (calc.). CoFs declined -22bps QoQ to 8.02%. Opex was largely in line with expectations, however, higher-than-anticipated credit costs at 22bps (+6bps QoQ) resulted in PAT miss (+10% YoY, -9% QoQ, -13% JMFe). Management indicated that there were no changes to PLR during 1Q or in July/August but may consider revising rates in 2Q/3Q depending on the trajectory of CoFs. As of 1Q, 69% of liabilities are floating rate leading to faster repricing.

* Asset quality impacted by seasonality: Headline asset quality saw seasonal weakening, with GS3/NS3 rising to 1.22%/0.83% (+14bps QoQ, +10bps QoQ). 1+ DPD increased to 4.15% (vs 3.39% QoQ), reflecting broader stress. Segment-wise, GS3 for HL rose to 1.15% (vs 1.02% QoQ), while non-HL GS3 stood at 1.47% (vs 1.32% QoQ). The

deterioration was mainly due to seasonality and local stress in states such as Maharashtra, MP, and KA, particularly in the sub-INR 0.5mn ticket size loans. Management highlighted that 1+ DPD has moderated in Jul’25 and is now ranging below 4%, suggesting early signs of stabilization. PCR on stage-3 declined -89bps QoQ to 31.6%, while total ECL cover stood at 0.7% (vs 0.66% in 4Q). We build in avg. credit cost of ~25bps over FY26E/27E in line with management guidance.

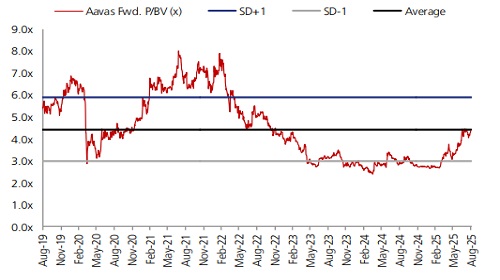

* Valuation and view: We believe that the current quarter was only affected seasonally in terms of growth and asset quality while we expect 2H to be stronger led by a) pick-up in growth momentum, b) margins stabilization with CoFs re-pricing and c) improvement in asset quality. We maintain BUY with a revised TP of INR 1,990 (valuing it at 2.9x FY27E BVPS vs 3.3x FY27E BVPS earlier) in return for avg RoA/RoE of 2.6%/12% over FY26E/FY27E.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361