Automobiles Sector update : Wholesales continue to remain healthy in Jan by Motilal Oswal Financial Services Ltd

Jan dispatches were strong for 2Ws, aided by a low base

* Auto demand continued to deliver strong growth in Jan’26 also aided by lean channel inventory across segments at the end of 3Q.

* While domestic ICE 2Ws grew 25% YoY in Jan’26, PV volumes rose ~13% YoY.

* On a YTD basis, the domestic 2W ICE segment has posted 6.7% YoY growth with Scooters (+12.5%) outperforming motorcycles (+4.1% YoY). The mopeds segment continued to underperform, with volumes remaining flat YoY.

* On a YTD basis, among the listed players, TVS and EIM were able to post healthy double-digit growth at 18.1% / 25% YoY respectively. On the other hand, while growth for HMCL and HMSI stood at 4% each, BJAUT volumes declined 3% YoY. ? The other factor to highlight is that the 125cc (2% volume decline YTD) has underperformed the motorcycle industry this fiscal relative to other segments.

* In, domestic PV, volumes rose 6.7% YoY on a YTD basis, led by UVs, which rose 9%, while cars grew 2.3% YoY. On a YTD basis, outperformers included MM (+19%), Toyota (+18%), and Kia (+14%). On the other hand, Hyundai saw a volume decline of ~4% YoY, while MSIL posted a moderate growth of ~3% YoY.

* Retail demand continued to be strong going into 2026, driven by post-GST momentum, healthy rural volumes supported by Pongal/Makar Sankranti, marriage season, better affordability and financing comfort. The near-term outlook remains positive, supported by an infra- and agri-focused budget, continued wedding/festive tailwinds, and improving rural liquidity. Within OEMs, our top picks are TVSL, MSIL, and MM.

ICE 2Ws: TVSL’s outperformance continues

* Domestic 2W ICE sales grew by a strong 25% YoY in Jan’26, albeit supported by a low base. On a YTD basis, the segment witnessed a growth of 6.7% YoY. ? For FY26YTD, ICE scooters outperformed motorcycles, posting 12.5% YoY growth, compared to 4.1% growth for motorcycles. Demand for mopeds remained weak, remaining flat YoY on a YTD basis.

* Among the listed players, TVS and EIM posted healthy double-digit growth of 18.1%/25% YoY, respectively, on a YTD basis. On the other hand, growth for HMCL and HMSI stood at ~4% each, while BJAUT volumes declined 3% YoY.

* TVS gained ~180bp share to 18.9% for FY26YTD.

* On the other hand, while HMCL and HMSI lost 80bp and 70bp market share, respectively, BJAUT lost 100bp on a YTD basis.

Segmental trends: Scooters continue to drive growth, rising 12.5% YTD

Motorcycle segment:

* Domestic motorcycle sales grew 20.3% YoY in Jan’26, while for FY26YTD, sales grew 4.1%.

* Outperformers included RE (+24.8%) and TVS (+16.4%) on a YTD basis.

* HMCL and HMSI grew below the industry at 2.5% and 2% YoY, respectively. Among the top four players, BJAUT was the only one to post a YoY decline in volumes (-3%).

* As a result, while RE saw a 140bp increase in market share to 8.5%, TVSL saw a ~120bp increase to 11%. HMCL saw a 70bp decline in market share to 42%, while HMSI saw a marginal decline of 40bp to 19.8%.

* Conversely, BJAUT saw a ~120bp decline YoY in market share to 15.7%. Its motorcycle market share declined below 16% for the first time since FY18.

100cc segment:

* The 100cc segment posted a strong ~25% YoY growth in Jan’26. All players have posted healthy double-digit growth in Jan’26. Despite this revival, YTD volume growth for the segment was a marginal ~2% YoY.

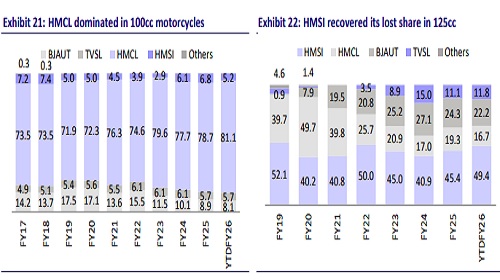

* On a YTD basis, only the market leader HMCL has posted positive growth of 6% in this segment. The worst impacted were HMSI/BJAUT, with volumes declining 26%/11% on a YTD basis.

* As a result, HMCL has further strengthened its position in this segment, gaining 320bp share to 81.1%, its highest market share in this segment. HMSI lost 190bp share to 5.2%, while BJAUT lost ~110bp share to 8.1%.

* For HMCL, both HF Deluxe and Splendor drove growth, now accounting for ~95% of its 100cc portfolio. HF Deluxe saw a 6% YoY growth, while Splendor posted a solid 5.3% YoY growth on a YTD basis. Passion Plus posted a healthy 11.8% YoY growth during FY26YTD, but its contribution has now reduced to just 5% of HMCL’s 100cc segment mix.

* For HMSI, Shine 100cc saw a significant improvement in wholesales for Jan’26, growing ~55% YoY. However, on a YTD basis, volumes declined 5.5% YoY. The Livo series continues to see a YoY decline, posting ~28% dip on a YTD basis.

125cc segment:

* The 125cc segment underperformed the broad motorcycle industry, growing ~7% YoY in Jan’26. Consequently, on a YTD basis, this segment saw a 2% YoY decline in volumes.

* On a YTD basis, although HMSI has outperformed its peers, posting a 9% YoY growth, it is seeing signs of slowing growth (Jan sales down 5%). Additionally, TVSL witnessed ~4% YoY growth in volumes on a YTD basis (but a healthier 32% growth in Jan’26). HMCL and BJAUT, on the other hand, saw a significant decline in volumes of ~17% and 11% YoY, respectively, on a YTD basis.

* As a result, HMSI saw a sharp ~500bp increase in market share YoY to 49.4% on a YTD basis. HMCL and BJAUT declined ~300bp and ~240bp to 16.7% and 22.2%, respectively. TVSL gained about 60bp share to 11.8% for FY26YTD. ? For HMSI, Shine grew about 5% YoY on a YTD basis. CB125 Hornet saw a slight pickup, selling about 8.7k units in Jan’26.

* BJAUT’s Pulsar 125cc sales declined ~4% YoY on a YTD basis. The company sold 1,157 units of its CNG model, Freedom, in Jan’26.

* For HMCL, while Super Splendor volumes declined ~21% YoY, Xtreme125R volumes declined ~30% YoY on a YTD basis. Glamour sales, on the other hand, saw a pickup in volumes, growing 8.2% YoY since the launch of a new variant.

* The new TVS Raider posted only a 3.7% YoY growth on a YTD basis, selling about 35k units per month.

150-250cc segment:

* This has been one of the highest growth segments, recording 34% YoY growth in Jan’26. Led by a strong pick-up in demand post the GST cut, the segment saw 11.7% YoY growth on a YTD basis, reversing the ~2% decline seen as of 1HFY26.

* On a YTD basis, TVS has significantly outperformed peers with ~40% YoY growth. While Apache posted a healthy ~32% YoY growth in volumes, TVS Ronin grew 2.5x on a YTD basis.

* As a result, TVS gained ~600bp market share to close at 29.5%.

* BJAUT maintained its share at 31% (+40bp) on a YTD basis. Its Pulsar range saw a ~12% YoY growth on a YTD basis. Demand for KTM continues to sustain, averaging at ~6k units per month this fiscal. ? Further, while HMSI lost 235bp share to 19.4%, Yamaha lost 320bp share to 16.8%.

? HMCL continues to underperform, with market share declining 50bp to 2.8%.

>250cc segment:

* This segment posted a 20% YoY growth in Jan’26 and a 23.7% growth on a YTD basis.

* RE and HMSI were the key growth drivers in this segment. RE saw a strong 24.8% YoY growth on a YTD basis, while HMSI saw a 25.8% YoY growth. Although TVSL saw a surge of 70.8% YoY in YTD volumes, it still occupies a small position within this segment. ? Given its outperformance, RE gained a 70bp share to 87.3% in the >250cc segment. Excluding Bullet (which is up 55% on a YTD basis), RE grew ~18% YoY on a YTD basis.

* Triumph, in partnership with BJAUT, posted a 33% YoY growth and averaged 3.9k units per month on a YTD basis. It clocked 4.8k unit sales in Jan’26, growing 18.7% YoY.

ICE scooters

* The segment witnessed a strong 35% YoY growth in Jan’26. On a YTD basis, scooters posted a 12.5% YoY growth.

* Key outperformers in this segment were TVSL (+25.7%) and HMCL (+26.5%) on a YTD basis. HMCL’s new Destini 125 saw a strong reception, growing 87% YoY on a YTD basis. Xoom also showed a healthy 34% YoY growth, selling ~5.2k units per month. However, HMCL’s Pleasure volumes continued to decline, dipping 29% YoY.

* Market leader HMSI posted a modest 5.7% YoY volume growth on a YTD basis. It saw a healthy revival in demand for Jan’26, posting a strong 55.2% YoY growth. However, it lost 290bp share at 44.8% for FY26YTD. For HMSI, Activa sales rose 8% YoY on a YTD basis, while Dio volumes declined 21% YoY.

* TVS gained a substantial 290bp share in scooters, reaching 27.7% on a YTD basis. The key growth driver was the upgrade of Jupiter 110, which is witnessing strong demand, with the brand recording 35% YoY growth on a YTD basis. Ntorq sales rebounded in Jan’26, registering a 20% YoY growth, which led to a turnaround in YTD performance to 3% growth from a prior decline.

* Suzuki maintained market share at 16.5% on a YTD basis. Growth of its flagship model, Access, has been moderating; it grew 11.3% YoY on a YTD basis. Meanwhile, Burgman remains the key growth driver, posting a 26.8% YoY growth.

PV update: UV mix now stands at 66%

* PV volumes grew by a strong 13% YoY in Jan’26. While UVs posted a healthy 20% growth YoY, cars saw a marginal decline of ~1% in Jan. As a result, passenger cars growth slowed down to 2.3% YoY on a YTD basis, while SUVs continued their growth trajectory, rising 9% YoY.

* On a YTD basis, outperformers included MM (+19%), Toyota (+18%), and Kia (+14%).

* In contrast, Hyundai saw a volume decline of ~4% YoY, while MSIL posted a slower growth of ~3% YoY. ? Overall, MM and Toyota have gained 150bp and 80bp share, respectively, in PVs on a YTD basis.

Car segment:

* Car wholesales declined marginally 1% YoY in Jan’26. However, excluding MSIL, industry volumes actually rose 23% YoY. It is also important to note that MSIL continues to face supply constraints, which are restricting its near-term volume upside potential. Consequently, on-ground car demand remains significantly stronger than levels seen prior to GST rate cuts. ? Key outperformers in this segment on a YTD basis included Tata Motors (+15.5%) and Toyota (+13.3%). Tata Motors witnessed a significant 120bp increase in estimated market share to ~10% for FY26YTD.

* Conversely, HMIL lost a 120bp share to close at 13%. Hyundai saw a decline across models, with i20 and Verna facing the largest decline of ~18% and ~40% YoY, respectively. Aura, however, saw a 21.3% YoY growth on a YTD basis, aided by Hyundai’s launch of the Prime Taxi range.

* For MSIL, YTD volume growth slowed to 2.8% YoY, marginally ahead of the market growth. It still maintains its leadership position, occupying ~67% of the car segment. Dzire was the primary driver for growth (+40%), while Swift and Baleno showed a more moderated growth of 7.1% and 1.6% YoY, respectively, on a YTD basis. On the other hand, the worst hit models were Celerio (-40%), Ignis (-14%), and Alto (-13%).

* Toyota Glanza saw a 13% YoY growth in volumes.

UV segment:

* The UV segment continued to maintain its growth trajectory, posting a 20% uptick in volumes for Jan’26. On a YTD basis, volumes rose 9% YoY.

* Outperformers were MM (+19%), Kia (+14%), and Toyota (+19%) on a YTD basis.

* On the other hand, MSIL (4%) and Hyundai (-3%) underperformed the segment on a YTD basis. However, it is pertinent to note that MSIL has seen a marked pickup in volumes post the GST rate cut (even Jan volumes rose 16% for MSIL).

* While MM has gained ~180bp share, reaching ~22% on a YTD basis, Toyota has gained a 90bp share, reaching 10.1%.

* On the other hand, MSIL lost 120bp share to 24.6%, and Hyundai lost 170bp share to 13.2%.

* Growth for MM was driven by Bolero (+14%), Scorpio (+9%), and Thar (+57%). Additionally, EV sales reached 38.5k units as of FY26YTD. On the other hand, XUV700 volumes declined 12% YoY on a YTD basis. The new 7XO has seen over 10k sales in Jan’26.

* As highlighted above, MSIL continues to face supply constraints. The new Victoris saw a strong 15k unit sales in Jan’26, with total sales since launch at 51.5k units. Brezza also witnessed a good pickup in volumes, clocking 17.5k units in Jan’26. Fronx volumes rose 9% YoY on a YTD basis. Moreover, while Ertiga volumes rose just 2% YoY on a YTD basis, they have witnessed a healthy pickup post the GST rate cut (+26% in Jan’26). Grand Vitara volumes declined to 7k units in Jan’26, largely due to supply constraints.

* HMIL volumes were flat YoY in Jan’26. On a YTD basis, only Creta posted a 3.5% growth. Venue saw a 2.5% YoY decline, while Exter dipped 15% and Alcazar declined ~27%.

* Kia Seltos witnessed a recovery, delivering 4.6% YoY growth on a YTD basis, aided by the positive reception of the new model launch. Meanwhile, Carens continued to witness good demand, growing 24% YoY on a YTD basis.

* For Toyota, Innova Hycross continues to outsell Crysta, with the mix now at 66:34. The Urban Cruiser remained the primary growth driver, registering a ~58% YoY uptick on a YTD basis.

Valuation and view

* Following the GST rationalization, demand has picked up across segments and remained intact even after the festive season. A notable trend is the marked pickup in demand for entry-level vehicles across both 2Ws and PVs. The demand momentum continued to remain healthy in 4QFY26 as well. With a recovery in demand, we expect discounts (in the PV segment) to gradually reduce.

* Within auto OEMs, TVSL, MSIL, and MM are our top picks.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Logistics Sector Update : Freight and cargo monthly by Emkay Global Financial Services Ltd