Buy CIE Automotive India Ltd for the Target Rs.539 by Motilal Oswal Financial Services Ltd

India to remain the key growth driver

India business above our estimate, Europe disappoints

* CIEINDIA’s consolidated PAT at INR 2.1bn was in line with our estimates. However, while India’s business performance was ahead of our estimates, Europe's performance missed our estimates.

* The India business is expected to be the primary growth driver for the company even in CY26. CIEINDIA remains focused on sustaining profitability through operational efficiencies. The stock trades at 19x/18.1x CY26E/CY27E consolidated EPS and is attractive. Reiterate BUY with a TP of INR539 (based on 21x CY27E consolidated EPS).

India margins ahead of our estimates, while Europe remains weak

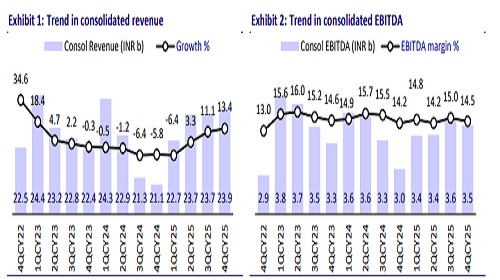

* CIEINDIA’s 4QCY25 consol. revenue grew 13.4% YoY to INR23.9b, coming in slightly below our estimate of INR24.5b. Primary drivers for this growth were good business growth in India and a positive exchange rate translation effect in Europe.

* Adjusted for the new labor code impact (INR 132m), EBITDA stood at ~INR3.5b(in-line), and grew 16% YoY. Adjusted EBITDA margin stood at 14.5% (in line), +30bp YoY/-50bp QoQ.

* Margins contracted due to one-off costs of ~INR200m related to the restructuring at its subsidiary, Legazpi. ? Adj. PAT grew 17% YoY and stood at INR2.1b (in-line).

* India business performance: Revenue grew 10% YoY to ~INR15.9b (in line). Adjusted India EBITDA margin was 15.9% (est. 15.3%), up 130bp YoY. The 4Q margins were hit by higher energy tariffs in Maharashtra (30bp impact).

* EU business performance: The EU business revenues saw a healthy 20% YoY growth to INR8b, slightly below our estimated INR8.3b. Positive foreign exchange translation aided revenue growth, far ahead of the 4%+ sales growth in EUR terms. EBITDA margin was 11.8% (est. 12.3%), down 140bp YoY. Margins were hit by a one-time CIE Legazpi restructuring-related cost.

* CFO/FCF grew ~36%/76% YoY in CY25.

Highlights from the management commentary

* GST rate reduction in Sep’25 has led to immediate demand improvement across segments, and management expects demand momentum to sustain into CY26.

* Order inflow momentum remains strong, with INR8.7b of new business wins in CY25.

* Management will focus on improving India's margins in the coming years.

* Metalcastello restructuring is complete, with profitability restored to predownsizing levels and no further major actions expected.

* Legazpi remains exposed to EV programs, and with the slower-thanexpected EV ramp-up in Europe, utilization levels have been impacted. Further actions will depend on market evolution.

* European auto demand continues to face structural headwinds from EV transition uncertainty, Euro-7 investments, and competition from Chinese OEMs.

* Strategic focus in Europe remains on protecting profitability, footprint optimization, and selectively targeting incremental opportunities from supply chain consolidation rather than pursuing aggressive growth.

Valuation and view

* Domestic demand in India is picking up across segments post the GST rate cut. However, Europe’s outlook remains subdued, although it seems to be stabilizing at lower levels. Thus, Indian business is expected to be the primary growth driver for the company even in CY26.

* Some of the financial attributes unique to CIE India include being net debt-free, having strict capex/inorganic expansion guidelines, generating positive FCF, and tracking an improving return trajectory.

* CIEINDIA remains focused on sustaining profitability through operational efficiencies. The stock trades at 19x/18.1x CY26E/CY27E consolidated EPS. Reiterate BUY with a TP of INR539 (based on ~21x CY27E consolidated EPS)

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412