Consumer Sector Update : Recovery green shoots visible; optimism building across segments By Motilal Oswal Financial Services Ltd

Jewelry and Food categories outperform; paint remains soft

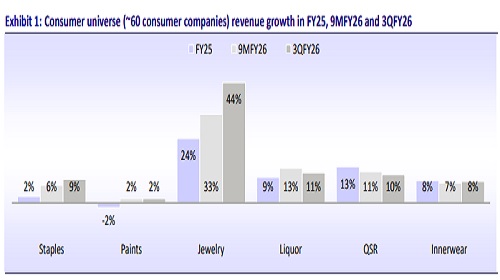

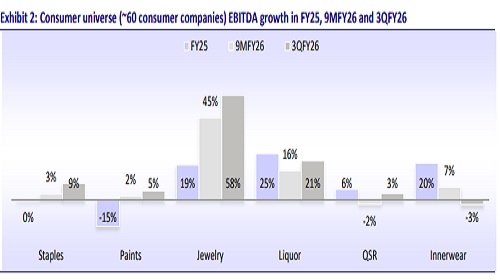

* Our widespread consumer coverage universe, a compendium of ~60 consumer companies with combined revenue of ~INR1.4t in 3QFY26/~INR3.9t in 9MFY26 (INR4.6t in FY25) and a market cap of ~INR35t, delivered aggregate revenue/EBITDA growth of 17%/15% in 3QFY26 and 13%/8% in 9MFY26. Excl. jewelry, aggregate revenue/EBITDA growth was 8%/9% in 3QFY26 and 6%/4% in 9MFY26.

* Revenue/EBITDA/APAT performance of all our coverage sub-segments in 3QFY26: staples +9% each, paint & adhesives +6%/+12%/+14%, innerwear +6%/+5%/+5%, liquor +9%/+22%/+26%, QSR +10%/+11%/NA (2x growth in 3QFY26 albeit smaller amount), and jewelry +43%/+55%/+63% YoY.

* In 3QFY26, demand trends saw gradual improvements across most categories, except paint. Staples witnessed resilient demand conditions. Cooling inflation and government initiatives are driving consumption recovery. While Oct’25 was affected by GST-related trade disruptions, subsequent months saw a normalization in trade channels. Food companies fared better than their personal care peers, backed by GST-led tailwinds. In paint, demand in Oct’25 was muted due to a curtailed festive period and an extended monsoon. However, marginal demand recovery was seen Nov onward. In alcobev, spirits continued to perform well, driven by strong P&A-led consumption and premiumization across key players (UNSP was impacted due to Maharashtra), while beer demand remained soft due to early winters. Innerwear demand saw some sequential recovery in 3Q, while broader demand trends remained soft. Revenue growth was driven by a favorable product mix. QSR players saw slight improvement in SSSG, and witnessed an encouraging demand uptick in Jan’26 vs. 3Q. Jewelry players continued to report strong revenue growth, aided by a strong festive season despite high gold prices.

* Most staple companies witnessed stability in raw material prices, leading to a better gross margin print, and companies expect this trend to continue in the near term. EBITDA margin also remained in a similar trajectory. In alcobev, margin improvement was supported by benign input costs and strong premium mix gains. Innerwear EBITDA margins remained flat YoY. QSR gross margins saw modest improvement, and restaurant margin saw sequential expansion due to ADS improvement. In jewelry, amid elevated gold price scenario and high coin sales, the studded mix deteriorated for most companies. That said, some companies witnessed inventory gains, particularly for silver (low hedging companies on gold as well) in 3Q.

* Outliers and underperformers in 3QFY26: Among our coverage companies, TTAN, BRIT, NEST, RDCK, and UFBL were the outliers, whereas CLGT, JYL, HUL, Devyani and Westlife underperformed

* Sector outlook and recommendation: As highlighted in our sector note and 3QFY26 preview, packaged food companies were expected to be the key beneficiaries of the GST transition, with minimal trade disruption. The 3Q performance of food companies validates this thesis, delivering robust growth across categories and channels. We expect supportive macroeconomic factors to act as a catalyst for boosting consumption sentiment in quarters ahead. Moreover, the industry expects a strong summer season, and thus summer products’ offtake from Mar’26 onward should support growth. Paint is expected to see a gradual recovery on a soft base. In liquor, premiumization continues to support healthy double-digit spirits growth. The innerwear segment is seeing a slow but steady recovery as GT channel trade sentiment improves.

* Our top picks are Titan, Britannia, Radico Khaitan and Zydus Wellness.

Performance summary of all categories and key areas to monitor

* Staples: Our staple companies reported sales growth of 9% (est. 8%); excl. ITC, revenue growth was 10%. EBITDA growth was 9% (est. 7%), with 9% APAT growth YoY (est. 8%). The companies witnessed resilient demand conditions in India and remained optimistic about a steady recovery in consumption over the coming quarters. Key government initiatives are driving consumption recovery on its desired path. Milder inflation, improved affordability after the recent GST rate rationalization, and falling interest rates are driving rural/urban consumption catalysts. While Oct’25 was affected by GST-related trade disruptions, subsequent months saw a normalization in trade channels. Food companies fared better than their personal care peers, backed by GST-led tailwinds (NEST +19%, ITC FMCG +13%, Britannia 10% vs. mid- to high-singledigit growth of most personal care companies). Most staple companies witnessed stability in raw material prices, leading to a better gross margin print, and companies expect this trend to continue in the near term. EBITDA margin also remained on a similar path. During the quarter, Nestle and Britannia were outliers, while Colgate and Jyothy performed below expectations.

* Paints: Despite a favorable base and multiple initiatives, the growth delivery remained soft. Management commentary on demand recovery was uninspiring, particularly after constructive commentary post 2QFY26. Demand in Oct’25 was muted due to a curtailed festive period and an extended monsoon. However, a marginal demand recovery was noted during Nov-Dec, and demand was slightly better by 3Q end. Overall paint category revenue/EBITDA grew 2%/5% in 3Q. Asian Paints delivered 4% revenue growth (-6% base), driven by 8% domestic volume growth. Indigo Paints posted 5% YoY growth (-3% base). Berger posted flat revenue, Kansai posted 2% revenue growth and Akzo revenue (LFL) declined 1%.

* Liquor: Liquor universe delivered sales/EBITDA growth of 11%/21% in 3Q. At a macro level, companies witnessed consumption green shoots, with the top end of the portfolio delivering a strong print in 3Q. The AlcoBev sector reported mixed volume performance in the quarter. UNSP posted a 3% volume decline, led by a 2% drop in P&A and a 9% fall in the regular segment. It was impacted by policy changes in Maharashtra and a high base in Andhra Pradesh. In contrast, RDCK delivered record volume growth of 17%, driven by strong premium momentum with P&A volumes up 26%, reflecting sustained premiumizationdemand. ABDL also maintained healthy premium traction with P&A growth of 19% YoY. Tilaknagar Industries reported strong 76% volume growth, aided by the acquisition of Imperial Blue in Dec’25, while underlying LFL growth stood at 17% in 3Q. Meanwhile, UBBL volumes declined 1%, impacted by higher excise duties in select states, affordability pressure, and an early winter season. Spirit companies expect the UK FTA to be implemented by mid-2026.

* QSR: QSR companies saw slight improvement in SSSG in 3Q, as the weak demand phase of Navratri moved to 2Q vs. in 3Q last year. However, most QSR companies witnessed an encouraging demand uptick in Jan’26 vs. 3Q. Players prioritized driving affordability through the value platform while maintaining strict execution discipline. In addition, they undertook select tactical initiatives in Jan’26, including targeted promotions and changes in online and offline channel strategies, which have started to show early positive results. While delivery channels remain strong, dine-in is showing a gradual improvement. Our coverage universe posted revenue growth of 10% YoY in 3QFY26 vs. 10% in 2QFY26 and 13% in 3QFY25. UFBL outperformed in 3Q.

* Jewelry: The category delivered sales/EBITDA growth of 46%/58% in 3QFY26. Jewelry companies continued to deliver robust sales growth, buoyed by strong festive demand and a significant rise in gold prices in 3Q (~60% YoY and ~20% QoQ). These companies indicated that revenue growth was driven by substantial average selling price increases, offsetting flat buyer growth. Titan (Jewelry standalone, ex-bullion), Kalyan, P N Gadgil (retail), Senco and DP Abhushan delivered revenue growth of 40%, 42%, 46%, 50% and 13%, respectively. Thangamayil revenue grew 112%. Titan/Kalyan/Senco SSSG stood at 32%/27%/39%, while Thangamayil’s SSSG was 61% in 3Q. The companies stated that despite volatility in gold prices, Jan’26 demand was healthy for them. The studded mix deteriorated for most jewelry companies, except Kalyan. We observed margins were supported by one-time inventory gains (mainly for silver, and select companies due to low hedging).

* Innerwear: Innerwear demand saw some sequential recovery in 3Q, while broader demand trends remained soft. Revenue growth was driven by a favorable product mix. The companies did not implement any price hikes during the quarter. Among key players, PAGE posted 6% revenue growth, Lux Industries/Dollar reported 22%/3% YoY revenue growth, while Rupa’s sales declined marginally YoY. Gross margins expanded YoY for most companies on the back of efficient raw material and product sourcing strategy. EBIDTA margin saw a slight contraction YoY across companies. PAGE delivered 6% YoY growth in revenue, with EBITDA/APAT growing 5% each in 3QFY26. Overall innerwear category revenue grew 8%, while EBITDA declined 3% YoY in 3QFY26.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412