Insurance Sector Update: Life Insurance : Product mix shift and cost efficiency absorbing GST hit By Motilal Oswal Financial Services Ltd

Continued VNB margin expansion in 3QFY26 as protection contribution improves

* The life insurance industry witnessed a strong performance in 3QFY26 with respect to growth as well as margins, supported by GST waiver, new product launches, recovery in ULIP momentum, improving mix toward protection and non-par, and strong growth in riders. While growth moderated slightly in Jan’26, we expect the stable growth momentum and margin expansion to continue going forward.

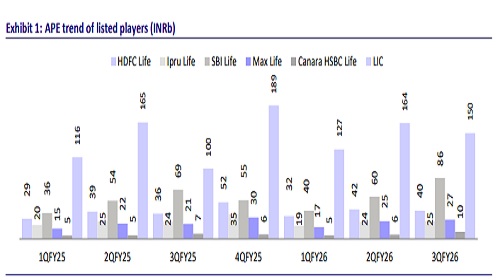

* Following the GST exemption from 22nd Sep’25, individual APE witnessed double-digit growth across Oct/Nov/Dec’25, leading to a 22% YoY growth for the industry (21% YoY for private and 26% YoY for LIC). Among the listed players, CANHLIFE witnessed the fastest growth of 28% YoY during the quarter. However, the momentum seems to have stabilized, with individual APE growing 9% YoY in Jan’26.

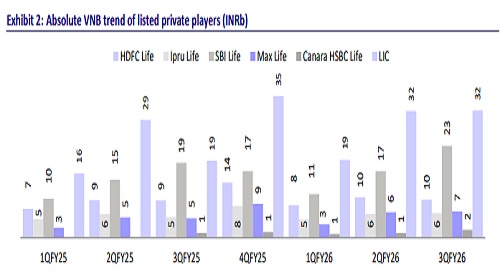

* Absolute VNB witnessed YoY growth across all listed players, with LIC reporting the fastest growth (+65% YoY). Most players witnessed VNB margin expansion YoY, with IPRULIFE reporting the highest growth of 320bp YoY. This was supported by the rising share of traditional products, strong growth in rider attachments, and increased sum assured, offset by the impact from loss of input tax credit (ITC) – which is likely to be mitigated in the next few quarters through operational efficiency and improving product profitability.

* On the regulatory front, RBI has flagged elevated distributor payouts as a risk to affordability and penetration (which dipped to 2.7% in FY25), amid rising first-year commission intensity (27% of first-year premium vs 24% in FY24). The possibility of the implementation of commission caps by IRDAI could support insurer profitability but may disrupt bancassurance economics and agent viability, posing near-term risks to new business growth and distribution expansion.

* Following 3QFY26 results, companies expect a slightly better APE growth in FY26 and sustained momentum going forward. VNB margin is benefiting from the GST boost to protection, improved product-level profitability, higher sum assured, and increasing rider attachment rates. Our preferred picks in the space are MAXLIFE (TP of INR2,200 premised on 2.3x FY28E P/EV), CANHLIFE (TP of INR180 premised on 1.7x FY28E P/EV), and SBILIFE (TP of INR2,570 premised on 2.2x FY28 P/EV).

GST boost to protection business; mitigation ongoing for loss of ITC

* MAXLIFE: The insurer continued to report 25%+ YoY APE growth for the third consecutive month (28% YoY in Jan’26). Protection products remain a key growth driver (99% YoY growth in retail protection in 3QFY26) and are expected to maintain momentum, backed by a marketing push in 4QFY26. We expect the industry-leading growth trajectory to sustain going forward. One-third of the impact from the loss of ITC (300-350bp) has been mitigated in 3QFY26, with full mitigation expected in the next few quarters.

* CANHLIFE: The insurer reported APE growth of 12% YoY in Jan’26 after witnessing strong 25%+ YoY growth for the last three months. Customers continue to favor linked products, while protection momentum remains healthy, with the insurer targeting a double-digit protection contribution (7% in 9MFY26). For the full year, the impact of ITC loss is estimated at ~185bp, which has been partially offset through renewal commission adjustments, with further mitigation possible via continued expense rationalization.

* SBILIFE: The company reported a strong 3% YoY growth in APE for Jan’26 after witnessing strong double-digit growth for the past three months. After factoring in favorable product mix benefits, the net impact due to GST for FY26 is expected to be limited to 30–40bp, underscoring strong internal mitigation through pricing, mix, and cost actions.

* HDFCLIFE: The insurer witnessed a 6% YoY decline in APE for Jan’26, while growth for the previous three months was also lower than the industry. The company posted retail protection growth of 50% post-GST exemption. Protection mix improved post-GST changes, with the segment growing 70% YoY in 3QFY26 and witnessing a rising preference for higher sum assured. The GST impact was contained to <200bp on VNB margins, and management expects to progressively neutralize the GST impact over 3–6 months

* IPRU Life: The insurer has been outperforming the private industry growth for the past two months, growing 11% YoY in Jan’26. Retail protection contribution continued to improve from 6% in 3QFY25 to 8.2% in 3QFY26 (overall protection contribution at 18.4% in 3QFY26 from 16% in 3QFY25). Partner-specific negotiations are underway to ensure VNB neutrality while maintaining distributor economics

* LIC: LIC has been the biggest beneficiary of the GST exemption, with APE growth surpassing private industry growth for the past four months (21% YoY growth in Jan’26). Protection APE grew 18% YoY during 9MFY26. The GST impact on VNB margin is expected to be offset by a product mix shift, cost optimization, and improvement in persistency.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Tag News

Insurance Sector Update : ULIP resilient; focus on PAR by PL Capital

More News

Banking Sector Update : Jul-Sep 2025 Earnings Preview - Margins to dip QoQ but may bottom by...