Add KPITTECH Ltd for the Target Rs.1,030 by Choice Institutional Equities

Ramp-downs Offset by New Wins; Recovery Momentum Building Up

We believe KPITTECH revenue growth is to be supported by a strong traction in CV/Off-highway and increasing relevance in Autonomous, Connected Vehicles and After-sales solutions. Although completion of 2 major SDV programs may weigh on H1FY27 growth, ramp-ups in new accounts should majorly offset the impact. We maintain ‘BUY’ rating and revise TP downwards to INR 1,030, valuing the stock at 25x (earlier 30x) on FY28E EPS. However, sustained execution, wallet share expansion, new client wins, product-led growth and expansion into adjacencies like Micromobility supports medium-term rerating potential

Revenue & Margin Largely In Line; PAT Misses on Forex Loss

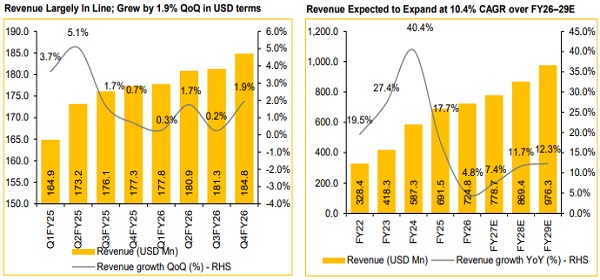

* Reported Revenue for Q4FY26 stood at USD 184.8 Mn, up 1.9% QoQ and 4.3% YoY (vs CIE est. at USD 181.3 Mn). In CC terms, revenues grew by 1.8% QoQ. In INR terms, revenue stood at INR 17,110 Mn, up 5.8% QoQ. For FY26, revenues came in at INR 64,549 Mn, up 10.5% YoY

* EBITDA for Q4FY26 came in at INR 3,533 Mn, up 6.0% QoQ (vs CIE est. at INR 3,466 Mn). EBITDAM was flat QoQ at 20.6% (vs CIE est. at 20.7%). For FY26, EBITDAM came in at 19.5 %, down 150 bps YoY

* PAT for Q4FY26 came in at INR 1,629 Mn, up 22.2% QoQ but down 33.4% YoY (vs CIE est. at INR 1,991 Mn)

Rev. Growth Resilient; CV/Off-highway to Drive FY27E Growth:

KPITTECH delivered a Q4FY26 CC growth of 1.8% QoQ, led by Commercial Vehicles and Off-highway segment, which grew 11.6% QoQ. Geographically, Asia led with a 25.1% revenue increase, whereas Europe declined 7.1% due to program shifts. Growth was supported by a healthy traction in Connected Vehicle Services, Propulsion and After-sales transformation programs. Management remains optimistic on FY27E growth, supported by robust deal visibility and expanding market opportunities. Completion of 2 major SDV programs in H1FY27 may pressure growth, but ramp-ups in newly-acquired accounts should offset impact. We anticipate temporary softness in H1FY27 revenues, followed by stronger momentum in H2FY27, driven by sustained traction in the Trucks and Offhighway segments across the US, India and China markets.

KPITTECH Boosts Platform-led Growth and Cybersecurity Capabilities:

KPITTECH is accelerating its transition towards a products and solutions-led business, targeting 50% revenue contribution from this segment in the next 3 years. The segment is growing above 30% YoY and accounts for 21% of the total pipeline. In Q4FY26, the company secured USD 349 Mn in TCV wins. Further strengthening its AI-led mobility capabilities, KPITTECH is acquiring a strategic stake in Cymotive Technologies, a leading automotive cybersecurity firm backed by Volkswagen Group. The acquisition enhances KPIT’s SDV cybersecurity offering and supports its long-term strategy of building scalable, reusable platforms and high-value cybersecurity products.

Near-term Margin Pressure Likely despite Strong Medium-term Outlook:

KPITTECH reported a Q4FY26 EBITDAM of 20.6% (flat QoQ), with FY27E guidance maintained at 20.5%–21.2%. In the medium term, the company targets 22%–24% EBITDAM, driven by AI-led products and solutions (expected to be ~60% of revenues in the next 3 years), fixed-price engagements, outcome-based delivery and Beacon platform productivity gains, supporting sustainable profitability through FY29E. However, we conservatively estimate margin expansion for FY27E to 20.9%, given headwinds from EV/Autonomous program delays, OEM pricing pressure and talent upskilling investments.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131