Add Capri Global Capital (CGCL) Ltd For Target Rs. 250 By Choice Institutional Equities

Resilient Growth across Segments:

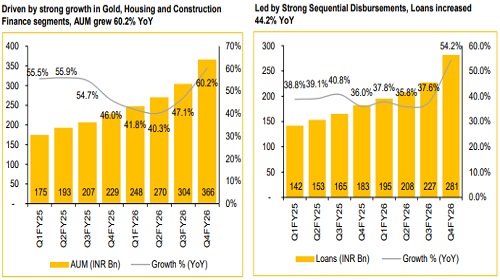

CGCL Q4FY26 performance was driven by strong AUM growth across Gold, Housing and Construction Finance segments. Total AUM grew by 60.2% YoY / 20.4% QoQ. Gold Loans AUM grew by 110.9% YoY / 32.5% QoQ to INR 169.6 Bn, while the Housing Finance and Construction Finance increased at 43.2% YoY (+14.7% QoQ) to INR 74.5 Bn and 38.1% YoY (+11.7% QoQ) to INR 57.1 Bn, respectively.

View and Valuation: We revise our FY27E/FY28E PAT estimate by +22.5%/ +9.2%, respectively, led by stronger NII growth, which, in turn, was driven by higher AUM and increase in Net Interest Margin (NIM) on account of decline in Cost of Funds (CoF). We anticipate further reduction of 10–20 bps in CoF in FY27E. We value CGCL using residual income approach at INR 250.0 and upgrade our rating on the stock to ‘BUY’. Our Target Price indicates FY27E/FY28E Price to Adjusted Book Value of 2.8x/2.3x.

Stronger Profitability led by Higher NII and Lower Operating Expenses

* CGCL reported a life-time high quarterly PAT of INR 2,828 Mn in Q4FY26, up 59.1% YoY and 10.7% QoQ, driven by higher NII led by stronger AUM growth and lower operating expenses

* Consolidated AUM grew by 60.2% YoY (20.4% QoQ) to INR 366.2 Bn, driven by robust growth of 110.9% YoY in Gold Loans, 43.2% YoY in Housing Loans and 38.1% YoY in Construction Finance

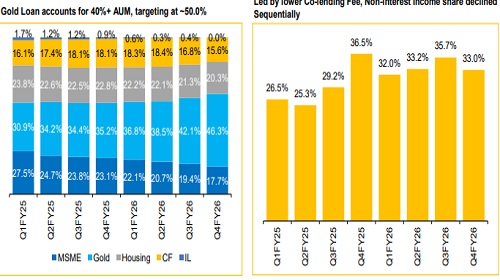

* Non-interest income increased by 33.9% YoY (7.3% QoQ) to INR 2,935 Mn, accounting for 33.0% of the total income

* Car loan origination improved 18.0% YoY to INR 34,918 Mn in Q4FY26, led by increase in average ticket size, which stood at ~INR 1.2 Mn

* Reported NIM improved sequentially to 9.2% (vs. 9.1% QoQ) driven by sharp reduction of 18 bps in CoF

* Asset quality improved sequentially. GNPA improved to 0.9% (-27 bps QoQ), whereas the NNPA declined to 0.5% (-13 bps QoQ)

Driven by Higher AUM and Improvement in Cost-to-Income, Earnings Outlook remains Robust

We forecast CGCL’s AUM and Loan growth to remain resilient at 27.2% and 29.8% CAGR, respectively, on account of rapid branch expansion. The company is anticipated to improve its network by opening 700–800 branches in the next two years, primarily led by Gold Loan branches. Despite reduction in average gold loan yields by 90 bps in Q4FY26, we expect the NIM on Interest Earning Asserts (IEA) to expand to 8.5% in the next two years, on account of reduction in CoF further by 10–20 bps in FY27E and 10 bps in FY28E. We forecast higher NII for FY27E/FY28E by +22.7%/+20.7%, respectively, as compared to our previous estimate. Higher NII and lower operating expenses are projected to drive improvement in overall profitability resulting in FY27E/ FY28E annualised RoAA to expand to 4.0% each.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131