Accumulate Bajaj Auto Limited For Target Rs. 11831 by Religare Broking Ltd

Record-Breaking Consolidated Financial Performance: Bajaj Auto delivered a transformational Q4FY26, with consolidated revenue rising 41% YoY to Rs 17,832 crore and net profit surging 93.8% YoY to Rs 3,492 crore. Full-year consolidated PAT increased 44.3% to Rs 10,574 crore, reflecting strong operational momentum across segments. Standalone revenue crossed Rs 59,000 crore for FY26, while EBITDA margins remained healthy at 20% despite inflationary pressures. Volumes surpassed 5 million units for only the second time in the company’s history. Strong free cash flow generation of over Rs 8,000 crore and surplus cash reserves above Rs 18,000 crore further reinforced Bajaj Auto’s robust balance sheet and capital efficiency.

Premium Motorcycle Segment Driving Growth Momentum: The domestic motorcycle business witnessed a strong recovery, particularly in the premium 125cc+ and 150cc+ categories, which outperformed overall industry growth. Bajaj Auto’s premium portfolio, led by KTM and Triumph, achieved its highest-ever performance with annual sales exceeding 2.25 lakh units and revenues crossing Rs 5,000 crore. Quarterly volumes for KTM and Triumph grew 43% YoY to nearly 43,000 units. The success of Triumph’s Speed 400 and multiple Pulsar upgrades strengthened market share gains and improved realizations. The premiumization strategy is helping Bajaj Auto transition toward higher-margin products, enhancing profitability and strengthening its positioning in aspirational mobility segments globally.

EV Business Emerging as a Major Growth Engine: Bajaj Auto’s EV business delivered a significant breakthrough in FY26, achieving double-digit EBITDA margins for the first time. The Chetak electric scooter crossed the milestone of 1 lakh retail sales in Q4 alone and secured nearly 23% market share in the domestic electric scooter segment. For the full year, Chetak crossed 5 lakh unit sales and generated approximately Rs 4,000 crore in revenue. Additionally, the company maintained leadership in electric three-wheelers while retaining a dominant 90% share in ICE CNG three-wheelers. The rapid scale-up of EV operations demonstrates Bajaj Auto’s strong execution capability and its readiness to capitalize on India’s accelerating EV adoption trend.

Financing Subsidiary and Export Business Scaling Rapidly: Bajaj Auto Credit Limited (BACL) emerged as a major value creator during FY26. Its Assets Under Management doubled to Rs 18,835 crore, while profit surged to Rs 665 crore from just Rs 58 crore in FY25, delivering an impressive 23% ROE. This indicates Bajaj Auto’s successful evolution into a diversified mobility and financial services ecosystem. Exports also remained a major strength, growing 25% YoY and crossing 6 lakh units for the second consecutive quarter. Strong momentum across Latin America, Asia, Africa, and Brazil supported export growth, while KTM exports from India revived sharply. The export business continues to provide geographical diversification and currency tailwinds.

Strong Capital Allocation and Shareholder Returns: Bajaj Auto demonstrated exceptional capital allocation discipline during FY26. The company generated over Rs 8,000 crore in free cash flow and announced a 100% payout of standalone PAT through a Rs 150 per share dividend and a Rs 5,633 crore buyback at Rs 12,000 per share. Even after these payouts, the company retained surplus cash exceeding Rs 18,000 crore, highlighting its strong liquidity position. This reflects management’s confidence in sustainable cash generation and limited balance-sheet stress. Bajaj Auto’s ability to reward shareholders aggressively while simultaneously investing in premium motorcycles, EVs, exports, and financing businesses underlines the strength of its business model and operational efficiency.

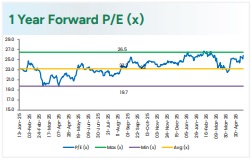

Outlook and Valuation: Looking ahead, Bajaj Auto remains well-positioned to benefit from premiumization, export recovery, EV penetration, and the expansion of its financial services business. However, near-term headwinds such as commodity inflation, moderating domestic motorcycle demand, and rising input costs could limit margin expansion in FY27. Management expects industry growth to normalize to 7-9% in the near term, although Bajaj Auto is likely to outperform supported by strong export momentum, premium motorcycle demand, EV scaling, and BACL profitability. The company’s diversified business model, healthy cash generation, and strong balance sheet remain key strengths supporting long-term growth visibility. On the financial front, we estimate Revenue, EBITDA, and PAT to grow at a CAGR of 14.7%, 15.1%, and 10.7%, respectively, over FY26-28E. Sustained execution across EVs, premium motorcycles, exports, and financial services will remain key long-term rerating triggers. Accordingly, we revise our rating to ACCUMULATE with a target price of Rs 11,831.

Strong Growth Ahead of Industry Trends: Bajaj Auto significantly outperformed the broader twowheeler industry in FY26. While industry growth remained moderate, Bajaj Auto delivered 24% YoY volume growth in Q4, supported by premium motorcycles, exports, and EV expansion. The company benefited from rising demand in the 125cc+ and premium segments, which are growing faster than entry-level motorcycles. Consolidated revenue rose 41% YoY, far exceeding industry averages. Export recovery across Latin America, Africa, and Asia further strengthened growth momentum. Bajaj Auto’s diversified presence across premium bikes, EVs, and three-wheelers helped the company outperform peers despite a challenging macroeconomic environment.

Premium Motorcycle Segment Driving Outperformance: The premium motorcycle business emerged as a major growth engine during FY26. KTM and Triumph delivered their best-ever annual performance, with combined sales crossing 2.25 lakh units and quarterly growth of 43% YoY. Triumph’s Speed 400 and Pulsar upgrades significantly improved market traction and realizations. Industry demand in the premium motorcycle category continued to grow faster than the mass commuter segment, benefiting Bajaj Auto’s strategy of premiumization. The company also gained market share through multiple product launches and upgrades. This shift toward higher-value motorcycles is improving profitability, strengthening brand positioning, and reducing dependence on lower-margin commuter segments over the long term.

EV Business Scaling Rapidly with Profitability Improvement: Bajaj Auto’s EV segment delivered a major operational breakthrough in FY26. The Chetak electric scooter crossed 1 lakh retail sales in Q4 and achieved nearly 23% market share in the domestic electric scooter market. Importantly, the EV business reported double-digit EBITDA margins for the first time, indicating improving scale efficiencies. The company also secured leadership in electric three-wheelers while maintaining dominance in ICE CNG three-wheelers. Rising EV adoption, government incentives, and improving charging infrastructure remain long-term tailwinds for the business. Bajaj Auto’s early scale-up and profitability in EVs position it favorably against competitors in India’s rapidly evolving mobility landscape.

Financing and Export Businesses Becoming Key Growth Drivers: Bajaj Auto Credit Limited (BACL) and exports emerged as strong non-core growth pillars in FY26. BACL doubled its AUM to Rs 18,835 crore and reported profit growth to Rs 665 crore with a strong 23% ROE, highlighting successful diversification into financial services. Exports also remained robust, growing 25% YoY and crossing 6 lakh units for the second consecutive quarter. Strong performance across Latin America, Nigeria, Brazil, and Asia supported export momentum. Favorable currency movements and premium motorcycle exports further aided growth. These businesses reduce dependence on domestic cycles and create multiple growth engines beyond traditional two-wheeler manufacturing.

Headwinds, Tailwinds, and Management Strategy: Despite strong performance, Bajaj Auto faces near-term headwinds from rising commodity prices, inflationary pressures, and slowing domestic motorcycle demand. Management expects industry growth to moderate to 7–9% in the near term due to cautious consumer spending. Commodity inflation is estimated to impact costs by 3.5–4% of revenue. However, the company is mitigating these pressures through selective price hikes, cost optimization, premiumization, and export growth. Tailwinds include accelerating EV adoption, recovery in exports, rising premium motorcycle demand, and improving financing penetration. Bajaj Auto’s diversified portfolio and strong balance sheet provide resilience against cyclical and macroeconomic volatility.

Management Guidance and Long-Term Outlook: Management remains optimistic about Bajaj Auto’s long-term growth trajectory, driven by premium motorcycles, EV expansion, exports, and financial services. The company expects exports to sustain momentum with a targeted run rate of over 220,000 units per month. EV penetration and profitability are expected to improve further as scale increases. Premium brands KTM and Triumph are likely to remain major growth drivers globally. While near-term domestic demand could normalize, Bajaj Auto’s diversified revenue mix should support stable earnings growth. Strong cash generation, high margins, and disciplined capital allocation continue to justify premium valuations relative to broader auto peers.

Please refer disclaimer at https://www.religareonline.com/disclaimer

SEBI Registration number is INZ00017433

600-400.jpg)