Buy RRKABEL Ltd For Target Rs.1,910 By Choice Institutional Equities

Middle East Contributes 12% to Revenues, Full Impact in Q1FY27E

RRKABEL’s exports grew 24% YoY reaching INR 22.8 Bn for FY26, accounting for 26% of C&W revenues. The West Asian conflict has disrupted almost all exports to the region; however, in Q4FY26, the impact was only for 30 days. We, therefore, believe RRKABEL’s Q1FY27E revenue will be affected, we now expect a growth of only 10% YoY for the quarter. However, rising copper prices and efficient pass-through in the domestic business will lead to an overall growth of 12.2% for FY27E.

Valuation & View

We raise our FY27E and FY28E revenue estimates by 4.6% / 7.4%, respectively, primarily on the back of persistent commodity inflation. Further, we raise our guidance for net income by 5.3% / 7.3%, reducing margin guidance by ~51bps and ~58bps for FY27E and FY28E, respectively. Our margin guidance incorporates increased logistic and energy costs. We introduce FY29E estimate, with expected Revenue / EBITDA / PAT CAGR of 14.0% / 15.7% / 19.2%, respectively, over FY26–FY29E. We value RRKABEL using the DCF approach at INR 1,910 (vs. 1,820), driven by upward revision in estimates. Our valuation implies a PE of 31.1x on FY28E EPS of INR 61.4. Thus, we retain our ‘BUY’ rating.

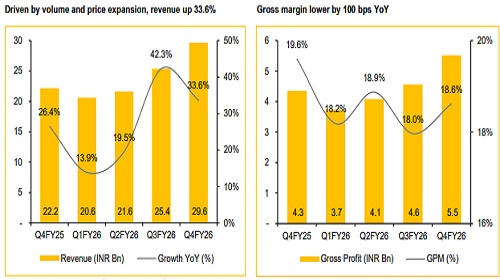

FY26 Growth Driven by Volume Increase and Elevated Commodity Prices

* For FY26, revenue grew 27.6% YoY to INR 97.22 Bn, volumes were up by 16% YoY

* EBITDA came in at INR 7.84 Bn (margin: 8.1%, +170 bps YoY), driven primarily by improving inventory management and operating efficiencies

* PAT surged ~58% YoY to INR 4.92 Bn

* C&W Segment: Revenue grew 31.0% YoY to INR 87.64 Bn, with EBIT margin expanding 143 bps YoY to 8.9%

* FMEG Segment: Revenue grew a modest 3.1% YoY to INR 9.59 Bn. EBIT margin improved 149 bps YoY to -3.4%, signalling breakeven in this segment is within reach

Higher RM Prices Boost Realisation; Margin Remain Protected

Price pass-throughs linked to elevated copper and aluminium prices led to higher realisations and faster than volume, revenue growth. Copper prices are expected to remain firm in the near term, providing a continued tailwind to the topline. The C&W industry operates on a cost pass-through mechanism which insulates margin during periods of raw material volatility. Q4FY26 exemplifies this dynamic: Volumes grew just 10% while revenue rose 33.6% YoY, reflecting RM-led price inflation. Despite this volatility, PAT margin contracted 16 bps even as PAT grew 30.1% YoY in absolute terms.

Operating Leverage to Kick in from FY28E

The capex cycle, which is to the tune of INR 12 Bn, is expected to conclude by FY27E, with FY28E being the first full year of expanded capacity. Expansion of EBITDA margin by 170bps in FY26 underscores the trajectory for RRKABEL to capitalise on new capacity and drive further margin improvement. FY27E is likely to see slower earnings expansion as depreciation burdens the bottom line in a year affected by external factors. However, we expect FY28E net income to expand by 36.0% as operating leverage and full revenue potential of the new capex kicks in.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131