Buy HDFC AMC Ltd for the Target Rs.2,700 by Motilal Oswal Financial Services Ltd

Well-positioned with reasonable valuations

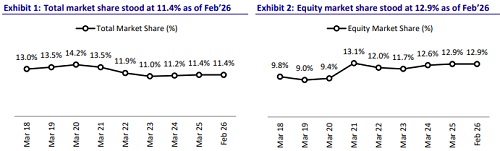

* HDFC AMC is one of the top three mutual fund houses, with QAAUM of INR9.2t and overall/active equity market share of 11.4%/13% as of Dec’25, supported by steady net inflows, robust SIP momentum, favorable equity mix, and a strong distribution network.

* Fund performance remains a key differentiator, with >69% of its AUM consistently staying in the top two quartiles on a 1-year basis since Apr’25 (~79% in Feb’26) and >70% on a 3-year basis since Jan’23 (~82% in Feb’26), reinforcing performance credibility and market share gains despite market volatility.

* Retail franchise remains strong, with SIP AUM of INR2.2t (+25% YoY; ~39% of active equity AUM), ~15.8% SIP market share and ~26% share of unique MF investors, reflecting deep retail penetration and sticky flows.

* The company retains clear cost leadership, with a cost-to-income ratio of ~19% (vs. peers at ~25-54%), translating into the best-in-class profitability (PAT-to-AAUM ratio of ~33bp), supporting strong cash generation and RoE of >30%.

* In FY25, within HDFC Bank, HDFC AMC has a share of ~28%, while for SBI, SBI MF accounts for 98%; for ICICI Bank, IPRU MF accounts for 69%; and for Axis Bank, Axis MF accounts for 35%. This indicates significant untapped potential for deeper penetration through HDFC Bank’s branch network.

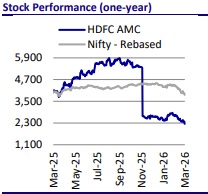

* We expect a CAGR of 17%/14%/15%/15% in AUM/revenue/EBITDA/PAT over FY26- 28E. HDFC AMC has corrected sharply by ~17% over the past month, compared to a 12-15% decline in listed peers, bringing valuations to more reasonable levels despite strong systematic inflows and consistent fund performance. We maintain BUY with a one-year TP of INR2,700 (36x FY28E core EPS).

Mutual fund industry remains on a strong growth trajectory

* The Indian MF industry continues to see strong structural inflows, led by rising retail participation (26% of MAAUM as of Feb’26) and sustained monthly SIP contributions (INR298b in Feb’26), which now form a meaningful share of incremental AUM. Growth is increasingly broad-based, with B-30 markets gaining traction (18% of MAAUM as of Feb’26) and contributing a higher proportion of flows compared to earlier cycles.

* Industry yields are expected to remain stable despite a regulatory overhang around TER, with most changes (including GST adjustments) seen as largely neutral. Adjustments to distributor commissions will be keenly watched.

* Discount brokers and fintech players have provided an additional boost to AUM growth, led by strong trends in SIP creations by giving users easy access and hassle-free interface to invest.

* Active funds continue to dominate the landscape, although passive products are gaining share (16-17%); most established AMCs are adopting a calibrated approach rather than aggressively expanding passive offerings.

* Overall, the industry remains structurally well-positioned, with retail AUM providing greater stability during volatile periods, while institutional flows continue to be more cyclical and sensitive to market movements.

Strong equity franchise and SIP momentum support AUM growth

* Mutual funds remain the core business for the company, with QAAUM of INR9.3t as of 3QFY26, translating into an overall industry market share of 11.4%.

* The company maintains strong positioning in actively managed equity, with AUM of INR5.7t and market share of 13%, supported by its established product franchise across large-cap, flexi-cap and multi-cap strategies.

* Asset mix remains favorable, with equity-oriented assets accounting for ~65.5% of QAAUM in 3QFY26 (vs. industry at 56.5%), significantly supporting yields and profitability, while maintaining a balanced presence across debt (~12.9% share) and liquid funds (~11.2% share).

* The company continues to witness strong growth in systematic flows, with SIP AUM growing 24% YoY to INR2.2t and quarterly systematic transactions (incl. SIP and STP) rising 24% YoY to INR47.3b, reflecting sustained strength in recurring retail inflows despite market volatility.

* Retail participation remains robust, with individual investors contributing ~69% of total MAAUM (vs. industry at 60.1%), supported by a large and growing investor base of ~15.4m unique investors (~26% industry penetration) and live accounts at 27.7m as of Dec’25.

* Digital adoption remains strong, with digital channels accounting for ~96% of purchase transactions as of 9MFY26, supported by the company’s proprietary platforms and third-party fintech integrations.

* The combination of a strong equity franchise, resilient SIP book and expanding retail investor base provides high visibility on incremental flows and AUM compounding. Continued industry tailwinds, including rising financialization of savings, increasing investor participation and strong SIP momentum, are expected to support steady growth in equity-oriented assets, which remain the key driver of yields and profitability. We expect a ~14% CAGR in revenue from the MF segment over FY26-28E.

Alternatives & PMS: Building a diversified asset management platform

* Beyond the mutual fund franchise, HDFC AMC has been gradually expanding its presence in portfolio management services (PMS) and alternative investment strategies as part of its broader asset management platform.

* PMS AUM stood at INR58b as of Dec’25, comprising discretionary mandates of INR8b and non-discretionary mandates of INR50b, supported by mandates from institutional investors and high-net-worth clients. The company has also won mandates from EPFO and SPFO, which have tight economics but will allow the company to build products that can be offered to other segments. Having built the team for the segment, the company expects improvement in scale and profitability for the segment over the medium term.

* In alternatives, the company is building capabilities across private credit, venture capital and private equity. Total AIF commitments stood at INR25b as of Dec’25, including INR12b in HDFC AMC Select AIF FOF-I and ~INR13b in HDFC AMC Structured Credit Fund-I, which has seen strong participation from institutional and UHNI investors at first close, with a visible pipeline for subsequent fund raises. The company is also looking to launch its second VC/PE fund of funds.

* The credit fund was launched in partnership with IFC, which will also act as an anchor investor and will invest up to INR2.2b in the fund. The partnership with IFC is based on a shared vision of expanding access to financing for midsized corporates that drive manufacturing output, employment, and regional development. ? The fund has declared its first close and has raised commitments of ~INR12.9b, of which almost 70% has come in from investors who have contributed INR250m or more.

* The platform continues to see investments in investment capabilities and product offerings, alongside expansion of the client base across institutions, family offices and ultra-high-net-worth investors, supporting a gradual scale-up of the business. Strategic partnerships and increasing engagement with global and domestic institutions are further strengthening the platform.

* While alternatives and PMS currently represent a relatively smaller share of overall assets (INR84b) compared to the mutual fund franchise, these segments typically operate at higher fee structures, providing scope for incremental revenue diversification.

* The business is currently in a scale-up phase, with focus on building capabilities, expanding mandates and deepening client relationships. Over the medium term, continued product launches, institutional participation and increasing allocation to private markets are expected to drive steady growth in the PMS and alternatives platform, contributing meaningfully to diversification of AUM and fee streams.

Diversified distribution mix driving scalable growth

* HDFC AMC benefits from a well-diversified multi-channel distribution architecture, spanning banks (~10% of total AUM as of Dec’25), national distributors (~22%), MFDs (~24%), and the direct channel (~44%), enabling stable inflows across market cycles and reducing reliance on any single channel.

* As of 3QFY26, the company manages ~INR9.2t of QAAUM, supported by a wide distribution footprint of ~106k+ empaneled partners and ~280 branches across India, enabling deep retail penetration and broad geographic coverage. ? Retail investors remain the core of the franchise, contributing ~69% of total AUM (~INR6.4t individual MAAUM) vs. industry average of ~60%, supported by a large and growing base of ~27.7m live accounts and ~15.4m unique investors (~26% industry penetration).

* In FY25, within HDFC Bank, HDFC AMC has a share of ~28%, while for SBI, SBI MF accounts for 98%; for ICICI Bank, IPRU MF accounts for 69%; and for Axis Bank, Axis MF accounts for 35%. This indicates significant untapped potential for deeper penetration through HDFC Bank’s branch network.

* Share of SIP flows through the HDFC Bank channel is meaningfully higher than overall book share with the bank. Sustained strong traction in SIP flows through this channel is expected to translate into incremental AUM share over time.

* The company has built a dedicated team for the channel and established strong engagement between its own digital channel and the bank’s digital team to build scale. Similar efforts are also underway for HDFC Securities.

* Systematic flows remain a key anchor for retail growth. In 3QFY26, quarterly SIP/STP flows stood at ~INR142b (~15.8% share), while SIP AUM reached~INR2.2t, reflecting sustained retail participation and strong distributor engagement. The increasing share of SIP flows across channels is expected to support long-term AUM compounding and improve flow stability.

* The company continues to deepen penetration in emerging markets, with 196 of ~280 branches located in B-30 cities. B-30 markets contribute ~19.5% of MAAUM (vs. ~12.9% in 3QFY20), supporting incremental mutual fund adoption and broadening the retail base.

* Fintechs as a group have registered 25m SIPs in 9MFY26, and HDFCAMC has successfully built a strong presence on leading platforms, securing a notable share, both in new flows as well as SIP registrations. Moreover, with a higher adoption of digital tools across channels, ~96% of overall transactions are executed digitally in 9MFY26.

* The combination of a diversified distribution mix, strong retail franchise, deep bank partnerships and increasing digital penetration is expected to support scalable and consistent growth in flows and AUM over the medium term.

Diversified product suite with disciplined launch strategy

* HDFC AMC maintains a diversified product suite across equity, debt, hybrid and passive categories, supported by a measured and scale-focused product strategy. The AMC has historically prioritized scaling flagship schemes with long performance track records, rather than frequent NFO-led expansion, supporting strong distributor confidence and stable retail flows across market cycles.

* The strategy emphasizes building large, well-performing funds rather than proliferating schemes, which has helped sustain long-term performance credibility. Notably, >69% of AUM has consistently been in the top two quartiles on a 1-year basis since Apr’25 (~79% in Feb’26) and >70% on a 3-year basis since Jan’23 (~82% in Feb’26), supporting distributor confidence and aiding market share stability.

* The AMC continues to gradually expand its passive offerings, including ETFs and index funds, to participate in the structural growth of passive investing, supported by increasing institutional participation and investor preference for low-cost products. ? With the introduction of the specialized investment fund (SIF) framework, the company is evaluating potential strategies under this category, with launches expected to be calibrated and aligned to client requirements and product suitability.

* The overall product strategy is expected to remain focused on deepening existing offerings, strengthening performance consistency and selectively expanding into new categories, thereby supporting sustainable AUM growth, distributor confidence and long-term profitability.

Stable yields with disciplined cost management

* HDFC AMC maintains a stable yield profile and operating margin discipline, supported by a favorable product mix and tight cost control, despite structural pressure from the telescopic TER framework.

* Yield profile remains healthy across asset classes, with equity yields at ~56-57bp (including index funds), debt yields at ~27-28bp and liquid yields at ~12-13bp in 3QFY26. The higher share of equity-oriented assets continues to support blended yields for the AMC.

* Margins remain resilient, with operating margins staying in the range of 33- 36bp, supported by operating leverage and disciplined cost management, even as TER compression impacts scale economics.

* Commission rationalization implemented earlier (Aug’24) has supported yield stability, partially offsetting the impact of telescopic pricing and competitive pressures.

* Recent regulatory changes, including the removal of the additional 5bp TER component linked to exit loads and revisions in the TER structure, are expected to exert pressure on yields, particularly in larger schemes, while smaller schemes may see limited impact due to slab realignment. The overall impact is expected to be managed through scheme-level optimization, pricing adjustments and cost discipline.

* HDFC AMC continues to demonstrate strong cost discipline and operating leverage, enabling it to sustain industry-leading profitability despite structural pressures on yields.

* The company reports operating margins in the ~33-36bp range (vs. peers at ~14- 34bp), among the highest in the Indian AMC industry, supported by a favorable product mix and disciplined cost management.

Valuation and view

* HDFC AMC remains a strong player in the mutual fund industry, backed by robust financial performance, steady AUM growth, and a strong retail presence. While short-term market fluctuations pose challenges, the company’s long-term fundamentals remain solid. With an improved market position, a well-diversified product portfolio, and digital expansion efforts, HDFC AMC is well-positioned to sustain growth and deliver value to its stakeholders.

* We expect a CAGR of 17%/14%/15%/15% in AUM/revenue/EBITDA/PAT over FY26-28E. HDFC AMC has corrected sharply by ~17% over the past month, compared to a 12-15% decline in listed peers, bringing valuations to more reasonable levels despite strong systematic inflows and consistent fund performance. We maintain BUY with a one-year TP of INR2,700 (36x FY28E Core EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041