Accumulate Navin Fluorine International Ltd For Target Rs.7,297 by Prabhudas Liladhar Capital Ltd

Quick Pointers

* 13 new molecules specialty segment introduced in FY26

* 15,000 mtpa of R32 equivalent capacity to be commissioned by Q3 FY27

Navin Fluorine International Ltd (NFIL) reported its highest-ever quarterly revenue of Rs9.4bn, reflecting robust growth of 33.8% YoY and 1% QoQ. This strong performance was driven by healthy momentum across all three business segments. The High-Performance Products (HPP) segment recorded a 20% YoY growth, supported by strong demand, improved realizations, and higher volumes. Additionally, commercial supplies of AHF commenced during Q4FY26, providing further growth opportunities. The Specialty Chemicals segment delivered a robust 39% YoY increase, with a strong product pipeline and solid order visibility already secured for FY27. The CDMO segment witnessed a strong performance, registering 61% YoY growth with 98% of its revenue was export-driven, aided by the commencement of commercial supplies from Phase 1 of cGMP4. With a healthy order book extending over the next three years, management has reiterated confidence in sustained growth momentum for this segment. We remain positive on NFIL’s long-term outlook, supported by a strong order pipeline, ongoing capacity expansion, and debottlenecking initiatives that are expected to sustain growth. At present, the stock trades at 35x FY28E EPS. We value the company at 38x FY28E EPS, arriving at a target price of Rs7,297, and maintain our ‘Accumulate’ rating on the stock.

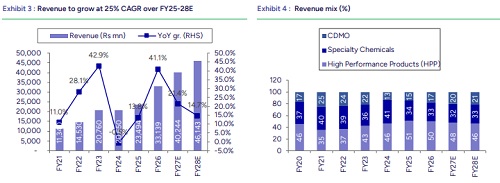

CDMO/Specialty Chemicals up 62%/39% YoY: Consolidated revenue stood at Rs 9.4bn, growing 33.8% YoY and 5.1% QoQ. For FY26, revenue grew 41.1% YoY to Rs 33.1bn. In Q3 FY26, CDMO revenue stood at Rs 1.9bn, while Specialty Chemicals contributed Rs 3.6bn. Gross profit margin expanded to 58.6% (vs. 54.2% in Q4 FY25 and 58.8% in Q3 FY26), an improvement of 440 bps YoY, supported by better realizations and lower raw material costs. On a full-year basis, FY26 vs FY25 segmental growth remained strong, with CDMO, Specialty Chemicals, and HPP revenues growing 59%, 44%, and 34%, respectively.

EBITDA margin expands by 870bps YoY: EBITDA stood at Rs3.2bn, up 79.7% YoY/ 4.4% QoQ (PLe: Rs2.3bn), While FY26 EBITDA stood at 10.8bn increased 103% YoY compared to FY25. In Q4FY26 EBITDA margin came in at 34.2% (vs. 25.5% in Q4FY25 and 34.5% in Q3FY26). Reported PAT at Rs2.1bn surged 124% YoY and 15% QoQ. while pat margin stood at 23% (vs 14% in Q4FY25 and 21% in Q3FY26

Concall takeaways: (1) In HPP segment Growth was led by improved realizations and higher volumes. (2) 15,000mtpa of R32 equivalent to be commission by Q3FY27 (3) In China R32 prices are currently at $9/kg (4) In Specialty Chemicals segment strong order visibility for FY27 Q4 and beyond. (5) The Chemours project is on track for completion in Q1FY27, Navin is the only manufacture of the product. (6) Project nector utilization to be around 70%-75% in FY27. (7) Globally agrochemical pricing continues to remain under pressure while volumes are recovering. (8) In CDMO segment cGMP -4 commenced, commercial supplies started to European players, strong revenue outlook for FY27 and beyond. (9) Working on 50-55+ molecules for CDMO, 50%-50% mix of early and late-stage molecules. (10) Solid growth momentum for the Fermion project

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

.jpg)