Reduce Greenpanel Industries Ltd For Target Rs. 270 By JM Financial Services

Market share takes the wheel

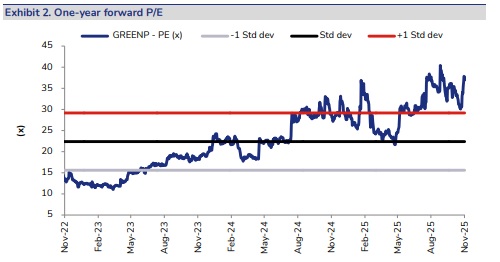

We met the Greenpanel Industries management, represented by Mr Shobhan Mittal (MD & CEO), Mr Vishwanathan Venkatramani (President – Finance) and Mr Himanshu Jindal (CFO). Key highlights from the interaction are: (1) The management reiterated MDF volume growth guidance of high-teens for FY26, with adjusted EBITDA margin (ex-EPCG impact and forex losses) expected to remain in high single digits to low double digits. (2) The company is transitioning towards a volume-led operating strategy focused on market-share consolidation and unlocking incremental operating leverage. (3) It is evaluating broader performance-linked incentive structures and potential ESOPs for senior leadership to strengthen organisational alignment. (4) It does not anticipate any sequential margin impact in 3Q, citing stable timber prices and easing chemical costs. (5) Margins are expected to see incremental improvement driven by ongoing cost-optimisation initiatives and a more efficient input mix. (6) Rising competitive intensity is likely to drive industry consolidation in the near term. We maintain our REDUCE rating on the stock with a target price of INR 270/share, based on 23x Dec’27E P/E.

* Continued focus on market share gain/margin improvement; FY26 guidance maintained: The management reiterated its MDF volume growth guidance of high-teens for FY26, with adjusted EBITDA margin (ex-EPCG benefits and forex losses) expected to remain in high single digits to low double digits. Export volume is likely to stay muted given weak demand in key Middle East markets. The company noted that OEM and export channels currently contribute ~30% and ~10% of revenue, respectively—both operating at relatively lower margins. The management remains constructive on the medium-term outlook for MDF and intends to sustain its market leadership, now at ~20% share (vs. 30–35% earlier). At utilisation levels approaching ~90%, the company expects incremental operating leverage benefits of ~INR 1,700/cbm.

* Evolving business strategy: The company has shifted towards a volume-led growth strategy focused on market-share consolidation and improved operating leverage, moving away from its earlier approach of prioritising pricing stability through exports and moderate utilisation. It highlighted increased market engagement, including its first overseas dealer event and enhanced salesforce incentive structures with monthly reward programmes. It is also evaluating broader performance-linked incentives and potential ESOPs for senior management to strengthen organisational alignment.

* Operating leverage to support margin trajectory: With timber prices expected to remain broadly stable—potentially softening marginally—and chemical costs easing from elevated levels, the management does not foresee any sequential margin impact from resin prices in 3Q. Over the medium term, margins are expected to improve further, driven by ongoing rawmaterial cost optimisation, employee-cost rationalisation, better input-mix management and operating-leverage benefits. The company is also evaluating additional wood species beyond eucalyptus and plans to gradually diversify procurement based on availability, pricing and efficiency considerations.

* Rising competitive intensity: The management expects heightened competition to drive industry consolidation in the near term. While QCO implementation has curtailed imports, effective enforcement of BIS norms remains a key monitorable. Further, the proposed revision of BIS standards for MDF could introduce more stringent quality requirements over the medium term.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361