Oil and Gas Sector Update : Crude Compass: Attack on Energy Infrastructure by Choice Institutional Equities

What has happened:

* Brent price spiked to ~USD112/b on March 18, 2026, 9% higher compared to closing price of USD103.42/b the previous day. The spike in Brent prices is on the back of an attack on Iran’s South Pars gas field, part of the world’s largest natural gas deposit.

* According to S&P Global Platts, Dubai spot crude assessments for May-loading cargoes hit a record USD157.66/b on March 17, 2026, surpassing the previous all-time high of USD147.5/b set by Brent crude oil futures in 2008. Meanwhile, Oman crude futures hit a record high of USD152.58/b respectively.

* Singapore refining margins have turned negative during the week. According to market reports, the negative margin is on the back of feedstock shortage which led to lower throughput and negative impact on margins.

In our opinion:

* The rise in Dubai and Oman crude prices reflect the scarcity premium that we have discussed in the earlier editions of Crude Compass. However, the increase in Brent is limited – which we believe is underpriced at the current levels.

* Despite a physical disruption of 7–11 mb/d, the current Brent prices are not yet baking in precautionary demand or hoarding premium. Therefore, we see upside risk to Brent prices.

? If the Hormuz situation remains status quo without progress in US–Israel–Iran negotiations, declining floating inventories and tightening marginal storage could drive a sharp increase in oil prices. This could push Brent towards ~USD 130/b over the coming weeks.

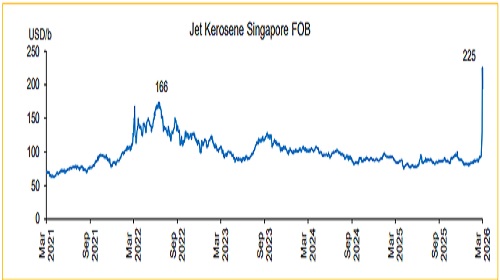

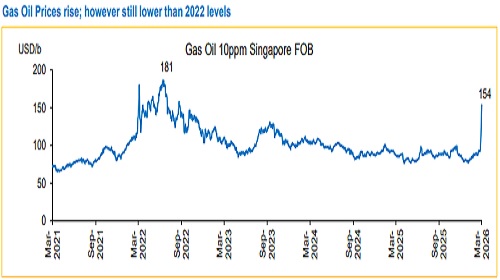

* The stark difference between the Singapore GRMs and the margins for Indian pure-play refiners lies in the fact that product slate for Singapore GRM is skewed towards gasoline. However, most Indian refiners have a middle-distillate-heavy product slate. The increase in diesel cracks is expected to more than offset the impact of lower utilization. Moreover, negative Singapore margins are against Dubai crude. Meanwhile, Indian refiners are currently replacing Middle East grades by Urals, therefore we see healthy margins for pure-players.

Bear case scenario:

* If US-Israel intervention leads to renewed negotiations and the reopening of the Strait of Hormuz, Brent prices could retreat towards ~USD 80/b over the coming weeks. This would largely reflect the unwinding of the precautionary demand premium, although a residual geopolitical risk premium may persist.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131