Neutral Tata Communications Ltd for the Target Rs.1,790 by Motilal Oswal Financial Services Ltd

Steady 3Q, albeit slightly weaker than our expectations

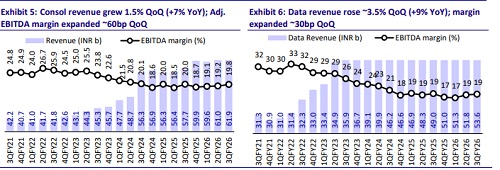

* Tata Communications (TCOM) delivered a steady 3Q, with 9% YoY (~3.5% QoQ, in line) data revenue growth, driven by a recovery in core connectivity (+4% YoY) and sustained growth in the Digital portfolio (+15% YoY). However, adjusted for FX, the consolidated revenue growth was muted at 2.2% YoY.

* TCOM’s consolidated EBITDA grew 7% YoY (5% QoQ), but came in ~3% below our estimate as margin expanded 60bp QoQ to 19.8% (35bp miss), as growth recovery in higher-margin core connectivity and seasonal strength in Kaleyra were offset by lower contribution from Voice and TCTS.

* The order book remains strong with healthy double-digit growth YoY (and QoQ), driven by large deal wins in core connectivity. The funnel remains robust with digital portfolio contribution at ~70%.

* TCOM announced Mr. Ganesh Lakshminarayanan (ex-CEO, Airtel Business – India) as the MD and CEO designate. He will assume the role of MD and CEO after the current MD’s retirement in Apr’26.

* We model ~9% data revenue CAGR over FY25-28E, with data revenue reaching INR249b by FY28. We believe the ambition of doubling data revenue (INR280b by FY28) remains a tall ask without further acquisitions.

* We cut our FY26-28E EBITDA by 2-4%, driven by slower-than-expected margin recovery. We build in ~10% EBITDA CAGR over FY25-28, with margin expanding to ~21% by FY28 (lower than management guidance of 23-25%).

* We value TCOM’s data business at 9.5x FY28E EV/EBITDA and the voice and other businesses at 5x EV/EBITDA to arrive at our revised TP of INR1,790. We reiterate our Neutral rating. Acceleration in data revenue growth, along with margin expansion, remains the key for re-rating

Core-connectivity growth recovers; data margin continues to improve

* Consolidated gross revenue grew ~1.5% QoQ (7% YoY on a like-for-like basis) to INR61.9b (1.5% below our est. INR62.8b). However, adjusted for FX benefits, the growth was modest at ~0.5% QoQ (+2.2% YoY).

* Data revenue at INR53.6b (in line) grew 9% YoY (+3.5% QoQ), driven by ~15% YoY (~4% QoQ) growth in the digital portfolio and recovery in the coreconnectivity revenue growth to ~4% YoY/(+2.5% QoQ).

* Consolidated net revenue (a proxy for gross margin) at INR34.8b continued to grow at a slower pace, rising ~4% YoY (+2% QoQ) due to continued weakness in net revenue growth for the digital portfolio (down 4% YoY vs. 15% YoY gross revenue growth).

* Consolidated adjusted EBITDA grew 5% QoQ (+7% YoY on a like-for-like basis) to INR12.3b (3% below our est. of INR12.7b) due to higher network costs (+4.5% QoQ, +13% YoY) and weaker performance in Voice and TCTS segments.

* Consolidated adjusted EBITDA margin expanded 60bp QoQ (though down ~15bp YoY on an LFL basis) to 19.8% (35bp) miss driven by growth recovery in higher-margin core connectivity and a seasonally strong quarter for Kaleyra.

* Reported consolidated PAT was 10% above our estimate at INR3.6b (-46% YoY, - 2.1X QoQ), largely due to higher other income (INR2.6b, up 9x YoY, tax refunds).

* Net debt declined INR12b QoQ to INR101b with net debt to EBITDA moderating to 2.2x (vs. 2.1x in Mar’25).

* Committed capex surged to ~INR8b in 3Q (vs. INR6b in 2QFY26), while cash capex rose ~14% QoQ to INR5.8b (up ~18% YoY).

* Reported FCF improved to INR10.5b (vs. INR2.2b QoQ, INR8.2b YoY).

* Reported RoCE (annualized) dips further to 14.4% from 15.1% in 2QFY26.

* For 9MFY26, TCOM’s revenue grew 7%, while EBITDA grew ~6% YoY as the margin contracted ~20bp YoY.

Key takeaways from the management commentary

* Leadership transition: The Board has approved the appointment of Mr. Ganesh Lakshminarayanan as CEO and MD designate, following the retirement of the current MD & CEO in Apr’26.

* Order book and funnel: The order book remains strong with healthy doubledigit growth QoQ and YoY. The company won a large deal in core connectivity from one of the world’s largest OTT content providers for a multi-continent subsea connectivity project. The funnel remains robust, with ~70% contribution from the digital portfolio.

* Normalized revenue growth: Adjusted for INR depreciation, the revenue growth was muted at 0.5% QoQ (+2.2% YoY).

* Net revenue decline in the digital portfolio was attributed to a couple of onerous deals in the CIS portfolio. The company took the hit in 3QFY26 and expects the trends to improve going ahead with a focus on growing the salience of higher margin non-SMS channels and AI integration with Kaleyra.

* Margin improvement was led by a recovery in core-connectivity growth and lower losses in digital. Management remains committed to 23-25% margin guidance over the medium term. The incremental margin drivers would be operating leverage, strategic bets (new product launches, more like SAAS), and moving away from SMS to channels such as Voice, RCS, etc. in CIS. Among the digital portfolio, management expects breakeven to be first hit in the CIS and Media verticals.

Valuation and view

* We currently model ~15% CAGR in digital revenue over FY25-28 and expect digital to account for ~54% of TCOM’s data revenue by FY28 (vs. ~50% currently). Acceleration in digital revenue remains key for re-rating.

* We cut our FY26-28 revenue estimates by ~1% each and believe TCOM’s ambition of doubling data revenue by FY28 remains a tall ask without further acquisitions. Overall, we build in ~9% data revenue CAGR over FY25-28, with data revenue reaching INR249b by FY28 (vs. TCOM’s ambition of INR280b).

* We cut our FY26-28 EBITDA estimates by 2-4% due to slower-than-expected margin recovery. We believe that margin expansion to 23-25% by FY28 could be challenging, given the rising share of inherently lower-margin businesses in TCOM’s mix. We expect margins to reach ~21% by FY28 (vs. ~19.4% in 9MFY26).

* We continue to ascribe 9.5X FY28E EV/EBITDA to the data business and 5X EV/EBITDA to voice and other businesses. We ascribe an INR39b (or INR136/share) valuation to TCOM’s 26% stake in STT data centers to arrive at our revised TP of INR1,790 (earlier INR1,830).

* After a significant time correction (no return since the 2023 analyst meet in Jun), the stock now trades at ~10.5x one-year forward EV/EBITDA (on par with its long-term average).

* We reiterate our Neutral rating as we await sustained acceleration in data revenue growth and margin expansion before turning more constructive on TCOM

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)