2025-10-15 06:21:44 pm | Source: Motilal Oswal Financial Services Ltd

Neutral Bosch Ltd for the Target Rs. 36,375 by Motilal Oswal Financial Services Ltd

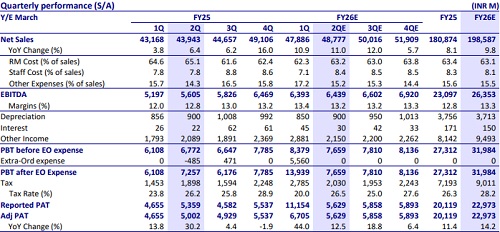

* We expect 11% YoY revenue growth, driven by aftermarket growth in the mobility division and pickup in demand in CV and 2Ws in 2Q.

* Margins to largely remain stable QoQ at 13.2%.

* As a result, we expect Bosch to post 12.5% YoY growth in PAT.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

More than 6.32 crore people join MyGov as citizen en...

Nearly 1.11 crore candidates certified under PMKVY 1...

Government gives nod to RBI for field trials of Rs 1...

India?s data centre capacity likely to surge 40 pc a...

Advanced Sys-Tek files preliminary papers with SEBI ...

Market Commentary (closing) for 27th July 2026 by Ba...

SBI MF introduces Nifty Midcap 150 Momentum 50 ETF FOF

Edelweiss MF introduces BSE LargeMid (60:40) Stable ...

ICICI Pru AMC announces change in creation unit size...

Quote on Daily Market Commentary for July 27th 2026 ...

More News

Financials Banking Sector Update : Reconciling banking business updates with systemic data b...

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motilal Oswal Financial Services Ltd

Financials Banking Sector Update : Are there upside risks to FY27E credit growth by Motilal Oswal Financial Services Ltd

Consumer Sector Update : Earnings outlook materially improves for the sector by Motilal Oswal Financial Services Ltd