Indian equity benchmarks closed a tad above the previous session close at 25461 - ICICI Direct

Nifty : 25461

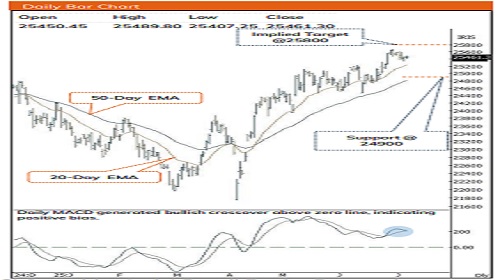

Technical Outlook

Day that was…

* Indian equity benchmarks closed a tad above the previous session close at 25461. Broader markets relatively underperformed the benchmark. Midcap and Small cap indices closed on a flat to negative note. Sectorally, IT, Metal and Consumer Durable underperformed, while, FMCG, Oil & Gas and Realty outperformed.

Technical Outlook:

* Index remained lackluster throughout the session, trading within an 80-point band. This resulted into the formation of a small Doji candle with short upper and lower wick, indicating a pause after the recent two-week upmove.

* The index is sustaining well above the recent consolidation breakout, which coincides with 20-days EMA a level that has been largely respected since April-2025. We believe this ongoing retracement is healthy for the market and sets the stage for a move towards 25800 in the coming week. Going ahead, all eyes will be on outcome of US-India bilateral trade deal coupled with onset of Q1FY26 earning season which would dictate the further course of action. The better-than-expected outcome would fuel momentum to challenge All Time High in coming month wherein strong support is placed at 24900. From the seasonality perspective, July has been the favourable month for Nifty since 1991, 71% of the time returns have been positive with an average of 2.5%.

* Structurally, over past three months index has maintained its winning streak while absorbing host of negative news around geo-political uncertainties coupled with clarity of trade tariff. In the process, market breadth has shown gradual improvement as currently ~60% stocks of Nifty 500 universe are trading above 200 days EMA compared to last month's reading of 52% that bodes well for durability of ongoing up move.

* On the broader market front, the Nifty midcap and small cap indices have witnessed flat to negative close relatively underperformed the benchmark and now just 3-4% away from their life time highs. Meanwhile, northward inching ratio of Nifty 500 / Nifty 100 makes us believe that broader market would continue with its outperformance.

* On the global macro front, weakness in US Dollar index would result into FII's inflow in emerging markets while cool off in Brent crude oil would boost the market sentiment.

* The formation of higher peak and trough makes us maintain our support base at 24900 for the Nifty which is based on 61.8% retracement of recent rally (24473-25654) and 20-day EMA.

Nifty Bank : 56949

Technical Outlook

Day that was :

* The Bank Nifty began the week on a softer note, closing at 56 ,949 , down 0 .15 % . The Nifty Pvt Bank index mirrored this sentiment, ending flat to slightly negative at 28 ,055 .70 , down 0 .04 % .

Technical Outlook :

* The Bank Nifty experienced mild profit booking after struggling to surpass the previous session’s high . This resulted in a small Doji candle with modest upper and lower wicks, signaling a healthy pause within the prevailing uptrend .

* A key highlight is that Bank Nifty respected the nine -month rising trendline as support, reaffirming bullish intent in line with the rule of polarity . The index remains above its 20 -day EMA a level it has consistently held since April . This, coupled with positive market breadth, supports the ongoing higher -high -low structure, underscoring a well -established uptrend . A decisive close above the prior session’s high may confirm trend continuation, with a projected upside toward 58 ,800 in the coming quarter, which is the implied target of the consolidation range (56 ,098 –53 ,483 ) . The support base is maintained at 55 ,500 , which represents the 50 % retracement of (53 ,483 –57 ,628 ) and aligns with the 50 -day EMA . Consequently, any dip from current levels could offer fresh buying opportunities .

* PSU Bank, moving in tandem with the benchmark, also witnessed profit booking and closed marginally below the previous session’s close, indicating a pause after the recent rally . The index continues its higher -high -low structure on the daily timeframe, reflecting inherent strength and trend continuity . After breaking out from an eleven - month falling trendline on 19th May, the index has maintained a higher -high -low structure on the weekly chart, signaling an intact uptrend . While Bank Nifty trades below ~ 1 % from its all -time highs, the PSU Bank index remains about 13 % below its all -time high, presenting a compelling case for a catch -up move . Immediate support on the downside is placed at 6 ,700 , which is the recent swing low and coincides with the 20 -week EMA .

* Structurally, Bank Nifty is undergoing phase -wise expansion, with each rally establishing new price zones of acceptance . Instead of sharp directional moves, the index is progressing through brief consolidations that serve as launchpads for subsequent advances . This transition from volatility -driven swings to range -bound bases suggests increasing market maturity, with demand emerging at higher levels . The narrowing amplitude of corrections indicates that stronger hands are absorbing supply, maintaining trend continuity .

Please refer disclaimer at https://secure.icicidirect.com/Content/StaticData/Disclaimer.html

SEBI Registration number INZ000183631

More News

Stocks in News & Key Economic Updates 23rd December 2025 by GEPL Capital Ltd