India’s Data Centre Capacity to Grow 4x to ~4 GW by 2030: CareEdge Ratings

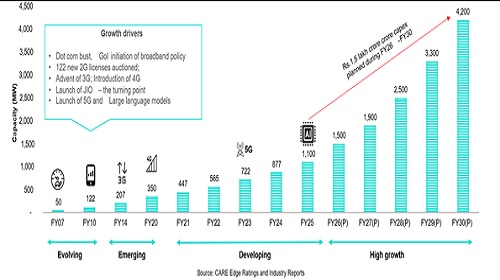

According to CareEdge Ratings, Indian Data Centre capacity is expected to increase to ~ 4 GW by FY30, with a large underlying investment potential of Rs. 1.5 lakh crore over the next year period ending FY30.

India’s Data Centre capacity per million internet users remains significantly lower at 1.2 MW per million users, compared with the world average of 5 MW per million users. Digitisation, India’s cost competitiveness in building Data Centres, and the increasing adoption of Artificial Intelligence (AI) are key factors driving strong growth in Data Centres in the country. India’s share in the global Data Centre market is approximately 4% in 2025, with a capacity of 1.2 GW, which is likely to reach 4 GW by 2030.

India’s co-location (co-lo) Data Centre capacity has registered major growth since FY21 and doubled to 1.2 GW during the four years FY22–FY25 (FY refers to April 1 to March 31). The capacity growth thus far has been complemented by high absorption levels with utilisation above 90% on average during FY22–FY25. Going forward, strong demand is expected to support steady absorption.

It notes that the sector enjoys strong revenue visibility through long term contractual arrangements, which ensure stable cash flows and promote high customer stickiness. With continued capacity growth and sustained absorption levels, the industry is expected to witness a revenue CAGR of around 24% during FY26–FY30. EBITDA margins are likely to remain broadly stable (40%–42%), although leverage levels may remain relatively elevated due to a high capex cycle in the development phase.

Puja Jalan, Director CareEdge Ratings, says, “The industry is in an upswing with high capex, fundraising capability of strong sponsors and large equity investments targeted to the Indian Data Centre entities. The industry is likely to witness a revenue CAGR of 24% during FY26-30, with steady-state margins ranging between 40% and 42%. The AI-led demand shall catapult the growth story. However, power infrastructure support is critical to realise the industry's potential. Also, the capability to manage cash flows amid rising costs and escalating commissioning timelines shall be key to sustenance.”

Over the last few years, the Data Centre cost has witnessed an increase (ranging between 50% - 70%) led by higher land prices, adoption of advanced cooling technology and investment in RE. At the same time, the commission timelines have also been escalated with changes in scope, delays in receipt of clearances, etc. The increased share of RE in power consumption and the adoption of newer cooling technologies support the industry's sustainability goals, while improving PUE and increasing the share of Green Data Centres.

India’s Data Centre Capacity Vs Global Peers

Digital transformation is catalysing economic growth and driving large-scale data creation. When India’s digital penetration is superimposed on that of global counterparts, it is observed that India has a fairly similar digital landscape to the rest of the world. For instance, the share of mobile subscribers (77%) and internet penetration (67%) as of 2025 is closer to the world average of 70% and 73%, respectively. CareEdge Ratings notes that India has attained digital parity with the world average, despite a low Data Centre share of ~4% of the world average capacity of ~30 GW, thereby implying immense growth potential. It estimates an investment of Rs. 1.5 lakh crore for the above-mentioned capacity augmentation during FY26-30. In addition, tenants are expected to spend 1.5x – 2x of this amount on IT equipment, taking the overall investment potential to nearly Rs. 3–4 lakh crore.

It highlights that the cost of constructing and operating Data Centres in India is significantly lower compared with global peers. India’s construction costs are roughly 30–40% lower than those of China and the U.S., supported by relatively lower land prices and benefits from competitive electricity tariffs. These factors, combined with supportive Government measures, make India an attractive destination for Hyperscalers and global Cloud Providers.

Tej Kiran, Associate Director CareEdge Ratings, adds, “Global AI investments have crossed nearly USD 1 trillion between 2020–2025, with India witnessing strong momentum supported by government initiatives. While data centre demand is currently driven by enterprise IT and cloud storage, AI-led workloads are expected to power the next phase of growth over the next 5–7 years, with the pace of adoption in India linked to the timely scaling of high-performance Graphics Processing Unit (GPU) availability.”

CareEdge Ratings also highlights that the global macroeconomic disruptions, amid West Asia conflicts, are unlikely to adversely impact the industry or heighten project execution risks in the medium term. It could potentially add to the demand prospects in the long term. However, in the near term, the impact remains monitorable.

Above views are of the author and not of the website kindly read disclaimer

.jpg)

More News

SBI sees inflation below RBI projections, calls it a regulatory policy too