Economics- Fed Policy: Inflation upside shuts the door on cuts Elara Capital

The US-Iran conflict has exerted incremental inflationary pressure on the US economy in CY26E, against a backdrop of softening but steady labour market conditions and growth. Amid the US-Iran war, the trajectory of inflation is upwards with 2% goal not possible in our view. With upside inflation risks set to outweigh downside risks to the labor market for a major part of the year, we withdraw our call of three rate cuts of 75bp in CY26E and now expect the Federal Reserve to hold rates. We see the negative spillovers from the Iran-US conflict to be long drawn, keeping inflation upside intact through CY26.

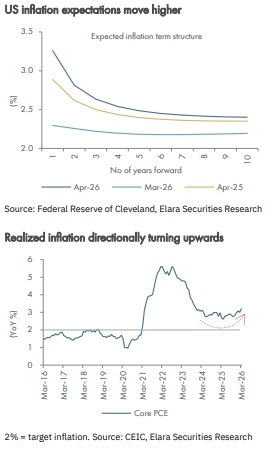

We expect the FOMC from the next meet to drop its easing bias from the policy minutes and communications, which remain in place as reaction to soft labor market. With inflation beyond the target for five straight years and potentially remaining for long, we expect the Fed to transition into policy tightening bias hereafter. This would lead to higher tolerance for softer labor market (unless the unemployment rate is >4.8%) when inflation remains elevated by 80-100bp consistently vs the target.

Assign 20% probability of a hike in CY26: The risks of next move being a hike is rising, in our view. But this is not our base case. However, if the Strait of Hormuz remains closed until September 2026, energy prices spike further, supply chain bottlenecks amplify and spill over to core PCE; thereby dislodging inflation expectations (core PCE > target for five years) amid relatively steady growth of 1.5-2.0%, our models assign a 20% probability for a 25bp hike in December 2026 meet. The 2026 FOMC rotation leaves the December 2026 voting mix more hawkish or cautious, with Hammack, Logan, Kashkari and Paulson as regional voters.

Can Warsh change the outcome? We do not think so. The constitution of FOMC, with inflation at 3%+ inflation (with upside risks), a 4.3-4.6% unemployment rate, and 2% growth will make it difficult for Kevin Warsh to build a consensus for any more cuts. Any attempt at that may see UST yield going up with 10y yield testing 5% levels -- an outcome that will eventually tighten financial conditions disproportionately.

Inflation projection revised higher: Reflecting the prospective spillover from elevated energy and food prices into core inflation, we revise our US core PCE forecast upward to 2.9% (Q4/Q4; previously 2.6%), with risks on the upside and see headline PCE at 3.0-3.5%. Tariffs along with surge in energy and food prices would keep inflation elevated and sticky. A runaway inflation is not our base case scenario this time, because the support to private demand via fiscal transfer payments akin to CY22 is missing.

Labor market holding up: We believe peak uncertainty regarding the US labor market has passed and hereon, the labor market is set to soften at a gradual pace. Our Composite Index of Lead Indicators from Regional Fed Surveys points to hiring optimism (15.3 on 3mma basis, the highest since February 2025) as tariffs-related uncertainty has eased, private payrolls (ADP) are turning up (21,000 3mma basis overall ex-education & health) vs layoffs in February and March 2026. The labor market momentum is at its highest levels in 18m as Kansas City Fed’s indicator stands 0.1SD above mean for two consecutive months vs negative print during January 2025-26. Considering existing domestic and foreign policy uncertainty in the US, easing labor demand due to automation, and overall tighter financial conditions, we retain our unemployment rate projection at 4.6% for CY26E (Q4 average).

Do not see tangible growth risks in CY26: On the growth front, the risks are moderate and are likely to be visible with a lag of at least a year and hence are unlikely to be a focus for the FOMC in CY26. With the US-Iran conflict leading to the surge in energy prices, the potential transmission channel to growth is likely to emerge from softening consumer demand supplemented by moderation in business spending, due to supply chain bottlenecks. The Middle East conflict can work as a tailwind for US energy exports, which can provide 10-15bp growth upside. We retain our 2.2% (Q4/Q4) growth projection for CY26E.

Please refer disclaimer at Report

SEBI Registration number is INH000000933