Economic : CPI Inflation : Uptick led by food and fuel; some passthrough to core visible By Emkay Global Financial Services Ltd

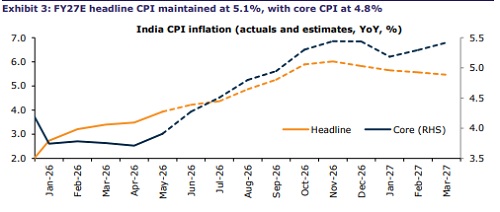

May-26 headline inflation ticked up to 3.9%, driven by higher food inflation (4.9%), along with retail fuel price hikes during the month. Core inflation also rose, to 3.9%, with some passthrough of higher energy prices visible in categories such as clothing and footwear and HH furnishings. Inflation in restaurants and accommodation services continued to intensify (1.8% MoM), reflecting continued price hikes amid the energy crisis. Core CPI ex-precious metals remained benign at 2.35% YoY. We maintain FY27E headline CPI at 5.1%, with food/core inflation at 5.8%/4.8%, respectively. The RBI is now likely to focus on domestic growth inflation dynamics going ahead, and we maintain that the bar for a conventional rate hike remains high. With downside risks to growth also intensifying, we believe the RBI may only raise rates to curb domestic demand or anchor inflation expectations.

Headline inflation at 3.9%; broad-based increase in food price momentum

Headline CPI inflation ticked up to 3.93% in May-26 (prior: 3.48%; Emkay estimate: 4.06%), with food inflation rising further to 4.78% YoY (prior: 4.2%). There was a sharp uptick in monthly momentum to 0.75% MoM (prior: 0.3% MoM), with that for food rising to 0.92% MoM (prior: 0.24% MoM). There was a broad-based increase in food price momentum, led by vegetables (3.3% MoM), eggs (2.6% MoM), ready-made food (1.6% MoM), meat (1.1% MoM), milk (0.9% MoM), and oils and fats (0.8% MoM). Pulses (0.2% MoM) and cereals (0.2% MoM) remained benign, while fruits and nuts (-0.5% MoM) declined on the month. Household energy inflation rose 0.4% MoM, with prices for LPG/PNG and kerosene rising in May-26. The transport index rose 1.9% MoM, with diesel and petrol price hikes of ~3% MoM each.

Core inflation rises to 3.9%, with some signs of energy price passthrough

Core inflation (ex-transport fuels) also rose, to 3.9% (prior: 3.7%), with monthly momentum at 0.5% (prior: 0.35%). This was primarily due to the rise in precious metal prices, with gold and silver jewelry prices rising 1.7% and 5.4% MoM, respectively. Inflation continued to intensify for restaurant and accommodation services (1.8% MoM; prior: 0.4% MoM), reflecting price hikes amid higher energy costs due to the Middle East conflict. Momentum for some other core inflation categories is also creeping up (clothing and footwear, and household furnishings, both logged 0.5% MoM), reflecting some passthrough of higher input costs. Core CPI ex-metals remained benign, however, at 2.35% YoY (0.4% MoM).

FY27E headline inflation at 5.1%, with core inflation at 4.8%

We are currently tracking Jun-26 CPI at 4.2%, as food price momentum continues to rise, with the remaining effect of fuel price hikes also playing out. Notably, this implies 1QFY27E headline inflation at 3.9%, vs RBI’s forecast of 4.2%. Nevertheless, we maintain FY27E headline inflation at 5.1%, assuming a Rs10/ltr fuel price hike in FY27 (partly reversed by Q4 as oil falls to sub-USD80/bbl), along with higher food price pressures due to El Nino-led adverse monsoons and second-order energy price spillovers. Our food/core CPI forecast stands at 5.8%/4.8%, respectively.

RBI’s focus to shift to domestic dynamics; bar for rate hike remains high

With the RBI and GoI having put a comprehensive set of measures in place to attract capital flows and stem pressure on INR, the RBI MPC will now focus on domestic growthinflation dynamics. We continue to believe that the bar for any conventional rate hike remains high. The MPC is likely to continue with its cautious, wait-and-watch approach, in line with its recently reiterated view in the MPC minutes that monetary policy cannot directly offset supply-driven inflation shocks, but should respond only when second-order effects begin to emerge. In this regard, the MPC flagged concerns around the potential passthrough of higher input costs to headline inflation going forward (with this being partially visible in some core inflation categories). However, with downside risks to growth also intensifying, we believe the RBI may only raise rates to curb domestic demand pressures or anchor inflation expectations.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354