India Strategy Weekly IdeaMetrics : FCNR (B) scheme – Positive for currency, rates, and credit cycle by Emkay Global Financial Services Ltd

The RBI FCNR (B) scheme contours are taking shape, and market expectations are building up to USD50bn inflows in the next 4M. This has multiple positives – we think it reverses the currency weakness, as the expected BoP deficit of USD75bn could get wiped out with the help of ECB inflows and FPI gilt purchases. Moreover, domestic liquidity gets a boost, which helps mid-tier banks like IDFC, IIB, and RBL, along with NBFCs. A large part of the flows should be cornered by big banks – SBI, BOB, HDFC, ICICI, Axis, and KMB. However, the direct earnings impact for these banks would be minuscule.

Likely flows

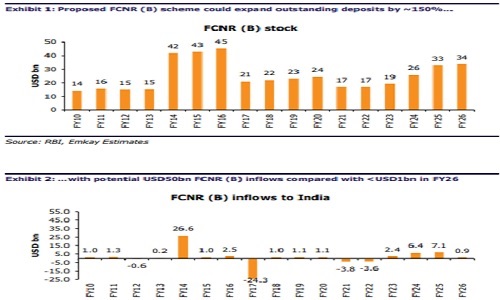

We estimate ~USD50bn inflows through the FCNR (B) scheme, at ~1.5x of existing stock of such deposits as on 31-Mar-26 (2013: incremental flows were ~1.8x of stock). We expect leverage of ~6-7x on aggregate (5-9x for individual customers), implying core deposit flow of USD6-7bn and the rest through leverage. This compares to unleveraged flows of USD7bn flows in FY25 These are preliminary estimates, and there are a few imponderables that could lead to a material undershoot. There is also some clarity needed by banks from the RBI on the availability of leverage to individual depositors.

Impact on banking system

We expect flows to be cornered by large banks, with a large share accruing to SBI, BOB, ICICI, HDFC, Axis, and Kotak. The entire industry does indirectly benefit, though. The scheme should add ~1.8% to the domestic deposit base and ~260% to overall liquidity. Even after RBI intervention to mop up excess liquidity, we think this should ease wholesale deposit rates (elevated for the last 2-3M) and steepen the yield curve. This is a tailwind for the credit cycle, as it removes the banking system’s worries about being able to fund deposit growth. We expect credit growth to sustain at 14.7% for FY27, funded by 13% FCNR-aided deposit growth.

Key winners and losers

Offshore deposits give collecting banks (listed above) a 50-100bp incremental advantage, but these translate to a minor earnings gain (~1%). HDFCB will be the biggest winner, given its recent deposit constraints. However, the spillover benefits banks with a weak retail franchise, and we see IIB, RBL, and IDFC as secondary beneficiaries from the softness in wholesale deposit costs. NBFCs should also gain, as we expect short-term funding costs to fall – though this is more a positive sentiment with no material earnings impact in the short term.

Currency outlook

We expect a material impact on the external account. In addition to the USD50bn projected from the FCNR (B) scheme, we expect an additional USD25bn from ECBs and gilt flows. This should wipe out our base case forecast for the BoP deficit of USD75bn before these RBI announcements, with a possible surplus for the rest of the year. We expect the currency to appreciate to ~Rs94/USD on the back of these flows, and further progress to the pre-war levels of Rs92/USD if the Middle East conflict is resolved.

Key risks to the thesis

This is a blue-sky scenario, and we see multiple risks to this thesis. i) Banks have to sanction limits for the leveraged funding to play out. The US was in a near-ZIRP era in 2013, whereas US rates are now at 1-year highs, so lenders may not have the same appetite for low-spread lending. ii) The proposition for depositors is an attractive midteens assured dollar return with no exchange risk and minimal counterparty risk – these deposits will compete with other high-risk asset classes, like US equities, for customer wallets. iii) A strengthening rupee does not guarantee resurgence of FPI flows – India continues to be vulnerable because of high valuations and being left out of the AI theme. Incrementally, this is good news, but we await the projected inflows, and will track developments in the coming days (like availability of leverage, etc).

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354