Bank Theme Report - Large private banks to benefit from rising interest rates by PL Capital

RBI could hike the repo rate in Oct’26 as CPI, which is rising, may firm up to ~6% in Q3FY27. Tight liquidity over Dec’25 to May’26 led to increase in bulk TD rates by 60- 144bps. As G-Sec to NDTL ratio for system fell to 27% in Mar’26 (H2’25: 30%), RBI has limited headroom to shore up liquidity. While the FCNR scheme may cushion interest rates, system loan growth may decline to 12-13% YoY in Mar’27 from 15-16% in Mar’26. In a tighter credit cycle exposed to growth/asset quality shocks, PSBs/MidCs are more vulnerable due to higher corporate/MSME share (47%/30%), while PVBs are resilient due to higher retail mix (47%). Over FY24 to FY26 end, PSBs/MidCs under our coverage have re-rated by 10-15%/35-50%, while PVBs have de-rated by 8-30%. We expect PVBs to outperform PSBs/MidCs given higher EBLR/unsecured share and better ability to garner deposits. Among PVBs, we like ICICIBC/KMB, and in PSBs, we pick SBI.

Liquidity utilized to protect the INR to USD:

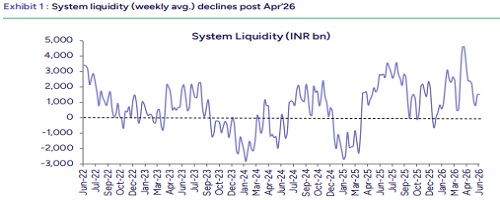

System liquidity is volatile since Sep’25. OMOs totaling INR 11.5trn from Oct’24 till Mar’26 were utilized by RBI toward dollar sales of INR 8.3trn to arrest INR fall led by FII outflows. The ongoing Middle East conflict has resulted in a global oil crunch, leading to weakening of INR vs. USD, which is sucking up liquidity that fell from INR 5.5trn in mid-Apr’26 to INR 1.5trn by mid Jun’26.

Inflation inching up, could rise faster:

After falling from Oct’24 to Oct’25, CPI is inching up; it rose from 0.3% in Oct’25 to 3.9% in May’26. As per RBI in its Jun’26 policy meet, baseline projections point toward CPI firming up to the upper tolerance level of 6% in Q3FY27. This forecast is subject to upside risks due to global supply chain disruptions, commodity price shocks and uncertainty about monsoon and El Niño conditions.

Repo hike may affect FY27 loan growth:

Given the likely inflation trajectory, RBI could hike the repo rate in its Oct’26 policy meet. Due to fall in system liquidity and expected repo hikes, PVBs have raised bulk deposit rates. As G-Sec to NDTL ratio declined from 31% in Sep’23 to 27% in Mar’26, there is limited headroom to shore up liquidity. Hence, system credit growth may contract to 12-13% YoY in Mar’27 from 15-16% YoY in Mar’26

PSBs/MidCs more exposed to system shocks:

From Mar’14 to Mar’26, corporate/MSME loan growth has been more volatile, suggesting greater vulnerability to system shocks. In contrast, retail/agri loans have been more resilient, given they haven’t seen negative growth due to housing and agri-gold respectively. In the upcoming rising interest rate cycle, MSME /agri would be more exposed to asset quality risk.

Large PVBs would be more resilient:

We would prefer banks having a higher retail credit exposure and a strong balance sheet. MidCs are exposed to maximum asset quality risk due to highest MSME/agri share (30%/17%), while PSBs are exposed to growth risk as corporate & MSME make up for 58%. PVBs are least exposed to growth and asset quality risks given their highest retail exposure is 47%, while agri share is lowest at 5.9%.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271