Renewable Equipments Sector Update : Growth outlook remains cautiously positiveby Prabhudas Liladhar Capital

We expect healthy performance in Q1FY27 across our solar equipment manufacturing coverage, supported by

(1) Sustained domestic solar capacity additions

(2) Continued demand support from ALMM and government-led initiatives

(3) Healthy order inflows and execution

(4) Ongoing capacity expansion and backward integration initiatives. For Premier, we expect revenue growth of 36.1% YoY, driven by improved capacity utilization and higher contribution from cell revenue. For Waaree, we forecast robust revenue growth of 82.7% YoY with 4.7% QoQ decline, and EBITDA margin at 18.5%, supported by module price hikes, but partly offset by higher raw material costs and weaker export realizations. For Vikram, we expect revenue to grow 52.6% YoY, with EBITDA margin contracting to 12.3% amid a weak module pricing environment and a relatively higher cost base. We expect our coverage universe to register sales/EBITDA/PAT growth of 66.6%/35.1%/16.5% YoY in Q1FY27. Furthermore, we anticipate Waaree to likely outperform on revenue growth, while continuing to lead on profitability.

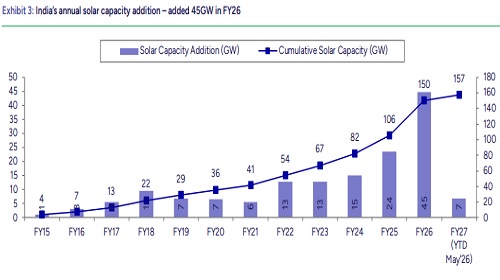

Healthy solar capacity addition continues:

India’s solar capacity additions in FY26 reached a record 45GW, surpassing FY25 additions of 23.8GW, taking cumulative installed solar capacity to 150GW. ALMM-I approved module capacity has been scaled up to ~173GW as of Mar’26 against 75GW of annual domestic DC demand, while ALMMapproved cell capacity has reached 31.1GW as of Jul’26. With 13.5GW of installed capacity under PM Surya Ghar: Muft Bijli Yojana as of Jul’26, along with 1.4GW installed under PM-KUSUM against 10GW sanctioned capacity along with utility and C&I, we expect the ongoing scale-up of government-led solar programs to drive sustained demand for domestic modules and related solar equipment.

* Premier Energies - Growth remains on track: We expect revenue to grow 36.1% YoY, aided by increased production volumes following improved utilization of manufacturing facilities. Cell/module production is estimated at 0.84GW/0.93GW in Q1FY27, with cell revenue expected to contribute a higher share of overall revenue. Premier Energies secured orders worth INR30.1bn (+17% QoQ) for 1.8GW of solar cells and modules from IPP, module manufacturers, EPC companies and other customers in Q1FY27. We upgrade the stock to ‘Accumulate’ from ‘HOLD’ due to recent movement in the stock price.

* Waaree Energies - Margins contract: We forecast robust revenue growth of 82.7% YoY, with 4.7% QoQ decline. EBITDA margin is expected at 18.5% (flat QoQ) supported by module price hikes, partly offset by higher raw material costs and weaker export realizations. Module sold is estimated at 4.2GW for Q1FY27. We maintain our ‘BUY’ rating.

* Vikram Solar - Margin under pressure: We expect revenue to grow 52.6% YoY, with EBITDA margin contracting to 12.3% (-910bps YoY), driven by moderation in module realizations and a relatively higher cost base amid a weak pricing environment. Recent commissioning of the 6GW Gangaikondan facility (Tamil Nadu) will strengthen Vikram Solar's manufacturing capacity and support future growth, with a gradual ramp-up expected to drive higher volumes and improve operating leverage. We maintain our ‘Accumulate’ rating.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...