India Strategy : BFSI - Going UW with SMID bias by Emkay Global Financial Services Ltd

We go UW on Financials and cut our exposure from 29% to 25%, with no exposure to large-cap and PSU banks. Structurally, rising competition has ended hyper-growth for large private banks, and they are unlikely to gain meaningful market share from here. The recent rally has pushed multiples back above fair value, and we see a time-correction ahead. We do expect a strong cyclical earnings recovery for lenders in FY27, led by a reviving credit cycle and bottoming margins at large private banks. We prefer to play that through SMID banks and NBFCs, with capital markets being our other preferred sector.

Cyclical earnings recovery

We expect FY27 to be a recovery year, with sector EPSg rebounding to ~15% after two years of single-digit earnings growth. Credit growth should stay elevated at 15% after a strong FY26 (FY22-25 CAGR: 15.4%), led by retail revival – vehicle and unsecured loans first, with mortgages later in 2HCY27. Deposit growth is the swing factor: as RBI rupee defense eases and liquidity improves, M3 and deposits should rise, relieving the stressed loan-deposit ratio. RoA repair is the key profitability story – NIMs normalize after the upfront hit from 125bps of rate cuts, lower deposit repricing reduces funding costs, and credit costs normalize further. We see 90-280bps RoE improvement for large private banks, though still stuck at 14-16%

Structural issues

The cyclical upturn masks a tougher structural reality. Competitive intensity is rising on three fronts – larger banks struggling to gain market share; disintermediation in the wholesale space through bond markets; and disruption of payments, distribution, and unsecured lending hurting long-term profitability. Consequently, the hyper-growth for private banks is largely over, with rich RoAs also under threat. FDI and strategic capital are key positives for SMID banks – recent investments (eg Warburg/ADIA into IDFC First) provide long-term growth capital, ease dilution overhangs, and signal confidence in franchise-building runway.

Valuations

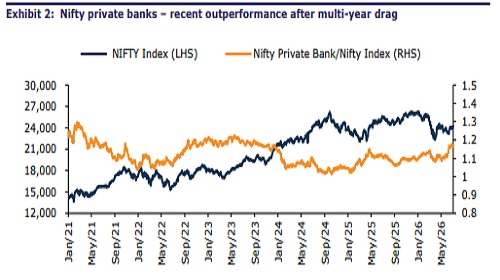

We believe that large-cap bank valuations are still above the fair-value zone, despite the multi-year de-rating. On a DDM basis, all ‘quality’ names price in BVPSg above RoE, which is unlikely given the high base and the lack of risk appetite. We, therefore, remain cautious on this space, as the market continues to extrapolate past some of the hypergrowth despite the structural downward shift in growth. The re-rating potential lies in franchises with a credible RoA-repair path, with historic valuation ranges largely irrelevant

Segmental preference

We go Underweight on the sector and recommend a stock selection approach. We prefer SMID private banks, capital-market plays, and NBFCs over large private banks, PSU banks, and Insurance. SMID private banks offer the clearest RoA-recovery story, backed by improving CASA and a turnaround in asset quality, while capital-market intermediaries benefit from the structural shift in household savings toward equities. We are Neutral on NBFCs, where we see growth beta, and cautious on PSU banks, which face a tough FY27 from the collapse in treasury profits

Key stock ideas

We exit HDFC Bank and have zero exposure to large private banks and PSUs. We switch our NBFC exposure from SHFL to MMFS, as we see stronger rerating potential (both playing on the auto theme). In AMCs, we switch from ICICIAMC to ABSLAMC as a more high-beta exposure, in line with our positive view on the markets. Our Financials exposure falls from 30% to 25% and we add Godrej Consumer to fill the gap.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354