Pharma Sector Update : Another quarter of domestic growth, currency tailwinds by Prabhudas Liladhar Capital

Pharmaceutical companies under our coverage are expected to see muted EBITDA growth of 1% YoY (up 12% QoQ) in Q1FY27. The primary drag continues to be a high base in the US segment. However, strong domestic growth and currency tailwinds will help drive growth. Strong traction in chronic therapies, and recovery in acute demand are expected to drive robust growth in the domestic formulations business. Launch of generic semaglutide following the Mar’26 patent expiry is expected to further support domestic growth and will be a key monitorable over the coming quarters. Meanwhile, the US business is likely to remain under pressure due to lower gRevlimid sales and continued pricing erosion in select generic products, although companies with exposure to complex generics, specialty products and limited-competition launches should continue to outperform. Our top picks are: SUNP, AJP, IPCA and ANTHEM

Favorable EBITDA growth expected for LPC, TRP and ARBP:

We expect strong YoY EBITDA growth from LPC (30%), DIVI (16%) and ARBP (16%). LPC’s performance should be driven by sustained momentum in the US generics business, led by niche products, including gTolvaptan, gSpiriva and gMirabegron. Further, we expect healthy revenue growth aided by currency tailwinds in DIVI, while ARBP EBIDTA growth should benefit from reduced losses from China and ramp-up of its PenG facility. TRP is expected to deliver 51% growth, aided by the consolidation of JBCP and steady performance across the base business. SUNP is likely to report ~6% YoY revenue growth, supported by the traction in its specialty and branded formulations business, with specialty sales expected to increase 15% YoY.

Healthy Q1 likely for IPCA, AJP:

We estimate EBITDA growth of 18% and 17% for IPCA and AJP, respectively. IPCA is likely to benefit from a recovery in its core business, while UNICHEM’s profitability is expected to improve from a low base. AJP's EBITDA is expected to improve, supported by strong revenue growth across branded generic segment. ERIS is likely to report moderate 9% YoY growth, impacted by weak export business

Margin pressure to persist for DRRD, CIPLA, ZYDUSLIF and ANTHEM:

We expect a sharp YoY decline in EBITDA for these companies, driven by a high US base and an unfavorable product mix. For ANTHEM, delay in shipments is likely to impact revenue growth (23% YoY decline).

IPCA, TRP and DIVI to lead margin expansion:

These companies are expected to report YoY margin expansion, supported by a better product mix and currency tailwinds. In contrast, margins for CIPLA, ZYDUSLIF and DRRD are likely to remain under pressure due to lower gRevlimid sales

High base weighs on reported US growth:

US revenue across our coverage universe is expected to post YoY decline in constant currency, due to the high base of gRevlimid sales. Excluding gRevlimid, the underlying business is likely to deliver steady growth. For DRRD, US revenue is expected to improve QoQ, aided by the normalization of the one-time gRevlimid write-off in Q4FY26. CIPLA and ZYDUSLIF are likely to see steady QoQ sales. LPC will continue to see strong YoY growth, supported by the continued traction in its niche portfolio.

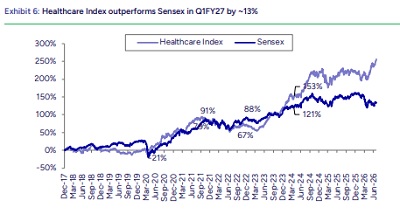

Healthcare Index outperforms Sensex; favorable outlook:

The Healthcare Index outperformed the Sensex for another quarter, by ~13%. Fundamentally, the sector continues to benefit from stable pricing dynamics, resilient domestic demand, currency tailwinds from INR depreciation, and relatively benign input costs. Looking ahead, earnings growth should gradually improve, supported by strong domestic formulations, increasing contribution from US specialty and differentiated products, and better operating leverage. Companies with exposure to complex generics and limited-competition launches are expected to outperform in the US market. Overall, we remain constructive on the sector, with a preference for companies having strong India franchises and better visibility in the US market. Our top picks are: SUNP, AJP, IPCA and ANTHEM.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...