ECOSCOPE : The Economy Observer : Broad-based inflation risks begin to emerge by Motilal Oswal Financial Services Ltd

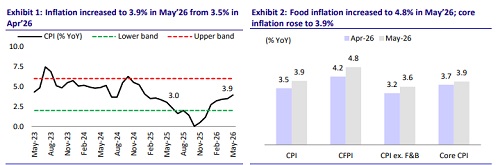

* India’s CPI inflation edged up to 3.9% YoY in May’26 from 3.5% in April, reflecting the impact of higher food and fuel prices. The increase was primarily driven by a rise in transport inflation following the phased petrol and diesel (petrol and diesel have 4.8% weightage in CPI) price hikes announced in May’26.

* Transport inflation rose to 1.8% in May’26 from 0% in Apr’26, while restaurant and accommodation services inflation accelerated to 5.7% in May’26 from 4.2% in Apr’26, reflecting the pass-through of higher commercial LPG prices. Inflation in personal care and effects also remained elevated at 18.5% in May’26, supported by continued strength in precious metals prices.

* Food inflation increased to 4.8% in May’26 from 4.2% in Apr’26, mainly led by vegetables and pulses. Vegetable and pulse inflation rose to 4.3% in May’26 from 2.3% in Apr’26, led by a sharp increase in tomato prices (48.4% YoY in May’26). Edible oil inflation remained elevated at 9.5% in May’26, while cereals (5.3% in May’26 vs. 3.8% in Apr’26), fruits (8.2% in May’26), milk, and ready-made food products also recorded higher inflation. Although domestic vegetable arrivals and reservoir levels remain comfortable, the rise in fuel costs could increase transportation and freight expenses, creating second-round effects on food prices in the coming months.

* Core inflation also showed signs of firming up. Headline core inflation excluding food and fuel increased to 3.9% in May’26 from 3.7% in Apr’26, while core inflation excluding gold, silver, and precious metals edged up to 2.2% in May’26 from 2.1% in Apr’26.

* Within core inflation, the primary drivers have been the transportation component and restaurant & accommodation services, reflecting the pass-through of higher fuel and commercial LPG prices. Beyond these categories, other demandsensitive components have also shown signs of firming up. Clothing and footwear inflation edged up to 3.0% YoY in May’26 from 2.8% in Apr’26. Similarly, inflation in household equipment and routine household maintenance increased to 1.9% in May’26 from 1.6% in Apr’26. We believe that going forward, upside risks to core inflation will intensify, as firms have yet to fully pass on higher input costs to consumers.

* Overall, headline CPI continues to remain below the 4% mark; however, the composition of inflation indicates that underlying price pressures are widening. Food inflation has started to edge up, supported by rising prices of vegetables, pulses, and edible oils, while weather-related risks from heatwave conditions and the increasing probability of an El Niño event could further aggravate food price pressures. In addition, the recent domestic fuel price hikes have already begun feeding into transport and services inflation, raising the likelihood of broader second-round effects. The RBI has revised its FY27 CPI inflation forecast upward to 5.1% from 4.6% earlier.

* We believe that inflation risks are becoming increasingly broad-based. Rising food prices, fuel price pass-through, potential El Niño-related disruptions, and gradually strengthening core inflation suggest that price pressures are likely to intensify over FY27. Accordingly, we expect headline CPI inflation to average 5.7% in FY27.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

RBI`s rate pause balances inflation control, growth support: Analysts