ECOSCOPE : The Economy Observer India CPI: Second month of sub-1% inflation by Motilal Oswal Financial Services Ltd

- In Nov’25, CPI stood at 0.7% YoY vs. 0.3% YoY in Oct’25, led by food price deflation. Core inflation was at 4.4% YoY, marginally lower than the previous month. Excluding gold, core inflation fell to 2.5%.

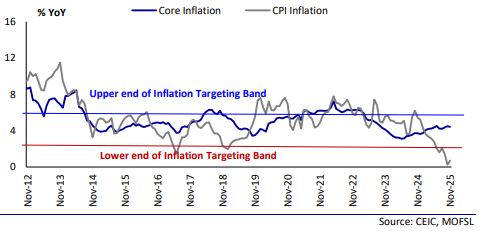

- Despite a slight pickup in headline inflation, it remains well below the RBI’s inflation target level of 4% and even below the lower threshold of the inflation band, i.e., 2%.

- The impact of the GST cut is visible on FMCG categories for the second consecutive month, with soaps, toothpaste, oils, shampoo, luggage, and shoes witnessing continued moderation.

- More importantly, rural inflation is at a meagre 0.1% YoY, while urban inflation is at 1.4% YoY.

- For FY26, the RBI forecasts CPI inflation at 2%, down from 2.6% earlier. We see downside risks of 20bp to this forecast. Excluding the impact of precious metals (which could add roughly 50bp), both core and headline inflation are likely to remain subdued, going into FY27. We expect the underlying weak inflation pressures to support the case for an additional 25bp rate cut in Feb’26.

Food disinflation continues

Nov’25 food prices declined by 2.8% YoY (+0.5% MoM) vs. (-) 3.7% YoY (-0.2% MoM) in Oct’25. The decline was led by vegetables, pulses, and spices. Cereals posted a modest increase of 0.1% YoY. The food inflation outlook remains soft, supported by higher kharif production and healthy rabi sowing. Reservoir levels remain adequate, providing further comfort on the food price outlook.

Core inflation at 4.4%. Ex-gold, core inflation drops to 2.5%

Nov’25 core inflation inched marginally lower by 10bp to 4.4%. The moderation was led by footwear, education-related expenses, downside correction in gold and silver, and lower FMCG prices. Excluding the impact of gold and silver, core inflation fell further to 2.5% in Nov’25 (2.6% in Oct’25). According to the RBI, if we exclude the impact of rising precious metal prices (~50bp), the underlying inflation pressures are even lower.

Rural inflation at 0.1% YoY; urban inflation at 1.4% YoY Nov’25 rural inflation remains extremely low at 0.1% YoY, although it picked up from the last month’s negative print of 0.3% YoY. The main reason for the low inflation is the decline in food prices, which have remained in the negative territory for the sixth consecutive month. Urban inflation is slightly higher than rural, with food price deflation continuing for three consecutive months. After food, the clothing and footwear category exhibits lower inflation growth for both rural and urban areas.

Outlook

Around 60% of the CPI basket is being impacted by GST rate cuts (food items, health, education, hair oils, shampoos, toothpaste, toilet soaps, consumer durables, etc). We are already observing the impact of this on both rural and urban inflation. For FY26, the RBI forecasts CPI inflation at 2%, down from 2.6% earlier. We see downside risks of 20bp to this forecast. Excluding the impact of precious metals (which could add roughly 50bp), both core and headline inflation are likely to remain subdued, going into FY27. In his recent monetary meeting, the Governor noted that extremely low inflation (sub-2%) is unhealthy for an economy that aspires to grow by 7% or higher. We expect the underlying weak inflation pressures to strengthen the case for an additional 25bp rate cut in Feb’26.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412