ECOSCOPE : The Economy Observer : Reflects broad-based inflation trends by Motilal Oswal Financial Services Ltd

* India has overhauled its wholesale inflation framework by introducing a new Wholesale Price Inflation (WPI) series with 2022-23 as the base year and launching Output, Input, and Service Producer Price Indices (PPIs). The WPI and PPI will run in parallel for five years, after which WPI will be phased out. The introduction of SPPI is a significant step toward measuring producer-level inflation in India's services sector, which now accounts for a substantial share of economic activity.

* The revised WPI basket is broader and more representative, with the number of commodities increasing from 697 to 953 items. The new series incorporates renewable energy sources, reclassifies crude oil and natural gas under fuel and power, and adopts a Gross Value of Output (GVO)-based weighting methodology.

* Wholesale inflation accelerated sharply to 9.7% YoY in May’26, driven mainly by rising fuel and commodity prices. The increase also reflects favorable base effects and the impact of higher global commodity prices amid geopolitical tensions in West Asia. The newly introduced Output Producer Price Index (OPPI) rose to 9.4% YoY in May'26 from 8.1% in Apr'26, closely tracking the rise in WPI inflation (9.7%).

* Inflationary pressures are becoming increasingly broad-based. Core WPI inflation rose to 7.9% in May’26 from 7.1% in Apr’26, indicating that higher input costs are spreading beyond energy into manufacturing and food products.

* Fuel inflation remains the primary driver, with fuel and power inflation surging to 30.3% in May’26. Crude petroleum, natural gas, and mineral oils continue to contribute significantly to the rise in wholesale prices.

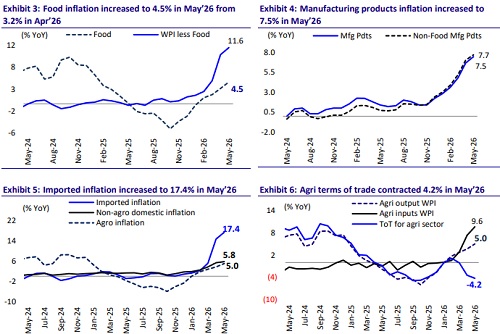

* Manufacturing inflation is gaining momentum, rising to 7.5% in May’26 from 6.7% in Apr’26. Given that manufactured products account for over 63% of the WPI basket, the increase suggests growing pass-through of higher energy and raw material costs across industrial supply chains.

* Food inflation has begun to reaccelerate (4.9% in May’26 from 3.2% in Apr’26), with processed food inflation rising to 6.1%. Higher transportation, packaging, and energy costs are increasingly feeding into consumer-oriented products.

* Agriculture's terms of trade deteriorated further in May’26 (-4.2% in May’26 vs. -3.4% in Apr’26), as input cost inflation (9.6% YoY) significantly outpaced output price inflation (5% YoY), potentially weighing on farm profitability.

* Wholesale inflation may be nearing its peak, provided food price pressures remain contained and energy prices moderate. The recent easing of tensions in West Asia could help cool crude oil prices and provide some relief in the June WPI print. Weather remains the key upside risk. A potential Super El Niño event and the risk of a double-digit rainfall deficit could disrupt agricultural production, increase food prices, and delay the expected moderation in wholesale inflation.

Introduction of PPI

A key structural reform announced alongside the new inflation series is the introduction of Output PPI, Input PPI, and Services PPI, marking India's transition towards a comprehensive PPI framework. These indices are designed to capture price movements at different stages of production and across both goods and services, bringing India's inflation measurement system closer to international standards.

The newly introduced OPPI rose to 9.4% YoY in May'26 from 8.1% in Apr'26, closely tracking the rise in WPI inflation (9.7%). This suggests that producer-level price pressures remain broad-based across the economy.

The government has stated that the WPI and PPI series will coexist for the next five years, allowing policymakers, businesses, and researchers sufficient time to adapt to the new framework and build historical comparability. After this transition period, the WPI will be phased out and replaced by the PPI framework, making producer price inflation the primary measure of upstream price pressures in the economy. The move is expected to provide a more accurate assessment of production costs, inflation transmission, and supply-chain dynamics, particularly given the growing importance of the services sector in India's economy.

Outlook:

* We believe wholesale inflation could be approaching its peak, provided food price pressures remain contained over the coming months. While the recent surge in WPI has been driven primarily by higher fuel and commodity prices, favorable base effects are likely to keep headline wholesale inflation elevated and close to double-digit levels in the near term, even if the pace of monthly price increases moderates.

* At the same time, the recent easing of tensions in West Asia could lead to some correction in global crude oil and energy prices, providing partial relief to wholesale inflation. As a result, the June WPI print may witness some moderation in energy-led price pressures if commodity markets remain stable.

* However, the inflation outlook remains subject to significant weather-related risks. The potential emergence of a Super El Niño event and forecasts of a double-digit rainfall deficit raise concerns about agricultural production and food supply conditions. Any adverse impact on crop output could lead to a renewed increase in food prices, adding to existing cost pressures from energy and commodities. Consequently, although wholesale inflation may be nearing its peak, sustained moderation will depend on both a normalization in global commodity prices and a favorable monsoon outcome.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

RBI`s rate pause balances inflation control, growth support: Analysts