Cross Sector Analysis - Artificial Intelligence Theme Report - MW to Managed Services, DC downstream opportunity by PL Capital

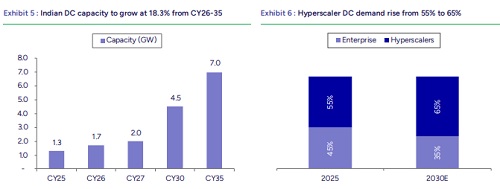

India is one of the world’s fastest-growing data center (DC) markets, with domestic installed capacity likely to expand from ~1,350MW in 2025 to ~4,500MW by 2030, implying a strong multi-year infra expansion cycle (27.2% CAGR over 5 years). The sector is expected to attract US$20–25bn of investments over the next 5–6 years, supported by rising hyperscaler participation, whose share in the Indian DC market is projected to increase to ~66% by CY30 from ~33% in CY25.

India’s DC expansion extends well beyond colocation and infrastructure deployment, as the rapid buildout of localized cloud and compute infrastructure is creating a significantly larger downstream opportunity across cloud migration, managed services, cybersecurity, AI, sovereign digital architecture, and enterprise modernization. With cloud penetration projected to jump to ~75% by 2030 from ~44% in 2024 as enterprises increasingly shift workloads from on-premise to cloud-based architectures. With this exponential increase in cloud adoption for Indian enterprises, the addressable market (TAM) for Indian IT service providers is poised for commensurate growth. IT vendors with higher India exposure and stronger positioning across telecom, cloud, cybersecurity, enterprise migration/modernization, and government digital infrastructure, would be direct beneficiaries of growing TAM. As cloud migration activity gains momentum, Indian IT vendors are likely to see a multifold increase in opportunities across government-led projects before they secure deals or engage with private enterprises.

Indian cloud market opportunity:

India's DC sector is expected to attract US$20–25 bn of investments over the next 5–6 years, driven by strong hyperscaler participation, while cumulative capex commitments over the next decade are estimated at US$130–145 bn. Hyperscaler capacity is projected to expand from 437 MW in CY25 to 2.9 GW by CY30, implying a CAGR of ~46%.

Managed services:

Driven by the rapid DC expansion in the country, the Indian cloud managed services market is projected to reach ~US$7.3bn by CY34E, at 14.3% CAGR over CY25-34.As India’s DC capacity potentially scales 2–3x over the next 5 years, the addressable market for infrastructure management, cloud operations, and AI-enabled managed services is expected to expand proportionally.

Software services:

India’s SaaS market is projected to reach US$ 50 bn ARR. India’s digital infrastructure and enterprise technology ecosystem is expected to witness strong multi-year growth, with domestic SaaS, PaaS and IaaS markets projected to grow at 25%, 28% and 23% CAGR, respectively, over the next 5 years.

Cybersecurity:

Led by the strong growth in cloud security, SOC monitoring, zero trust architecture, and AI-led threat management, the Indian cybersecurity market is projected to grow from ~US$11.3bn in CY25 to ~US$44bn by CY34, at 16.3% CAGR.

Overview of India’s DC ecosystem

India is fast emerging as a global DC and AI hub supported by its strategic geographic positioning, rapidly expanding internet ecosystem, and increasing data generation. But the country is yet to come up with a binding national policy framework for DC development. State governments have taken the lead in shaping the sector’s growth, with 15 states having already notified dedicated DC policies or used IT/ industrial policies to attract DC investment. The Union Budget 2026-27 announced of a long-term tax holiday extending to 2047 for foreign cloud providers operating from India-based DCs to attract investments.

India has seen massive digital transformation under the Digital India initiative. The internet subscriber base has increased by ~30% over the last 5 years, from ~0.8bn in CY20 to ~1.02bn in CY25. Average mobile data consumption in the country reached ~31GB per user per month in 2025, significantly above the global average of ~23GB, and is projected to nearly double by CY30. By CY30, the digital economy is expected to contribute 20% of national income, compared to ~12% in FY23.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

Tag News

Quote on Markets 30th June 2026 by Mr. Vikram Kasat, Head Advisory, PL Capital