Consumer Discretionary Sector Update : India AlcoBev: Aged to premium by Elara Capital

Premiumization has decisively gained traction in India AlcoBev , per Brand Champion 2026 data . P&A now dominat es volume, legacy mass brands are in a structural decline, and consumers and firms are pivoting upmarket. Category leadership has churn ed: Royal Stag overtook McDowell's in whisky, Old Admiral toppled Mansion House in brandy, and Allied Blenders and Distillers ’ (ABDL ) ICONiQ emerged as the cycle's breakout standout. United Spirits (UNITDSPR IN) is our top sectoral pick , led by resilient McDowell’s (MCD ), mid -prestige momentum and UK FTA optionality . We prefer Radico Khaitan (RDCK IN) among mid -caps given its diversified P&A growth in whisky, brandy and vodka. ABDL is set to benefi t from scale -up at ICONiQ and renewed focus . Tilaknagar Industries ( TLNGR ) faces near -term challenge on portfolio integration and growth revival

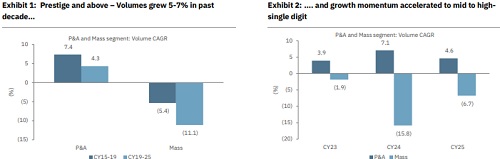

Premiumization reshapes growth dynamics:

P&A volumes compounded at 4.3% while mass declined from 5% to 11.1%, in CY19 -25. The shift is led by aspirational consumption and deliberate portfolio premiumization to chas e margin accretion. Legacy mass /entry P&A brands – Imperial Blue (-11.4%), Officer's Choice (-4.7%), and 8PM (-4.2%) – continue to bleed as consumers and companies pivot upmark et. This has generated tailwind s for RDCK and ABDL given the renewed focus on premiumization .

Whisky – Leadership rewritten; Royal Stag topples McDowell’s: India's whisky leaderboard was rewritten in CY25 :

a) Royal Stag (33mn cases) beat McDowell’s (32mn) to end two decades of leadership for the latter, led by focus post sale of Imperial Blue (IB ). But likely revival of McDowell’s from Maharashtra could intensity t he war,

b) ABDL's ICONiQ White emerged as the breakout standout, more than doubling to 9.5mn cases (+111%) after a 181% surge in CY24 , drawing share directly from McDowell's and IB

Brandy – Radico Khaitan takes the lead:

RDCK 's Old Admiral surged >100% in CY25 to 10.9mn cases, beating TLNGR ’s Mansion House (9.7mn) , propelled by aggressive capture of share in Andhra Pradesh post the opening of market there. TLNGR has also staged a recovery in Mansion House (+24% in CY25 post drop), but with its newly acquired Imperial Blue at a seven - year low volume (-11.4%in CY25 ), growth may be delayed

Prefer UNITDSPR and RDCK:

UNITDSPR’s P&A volume growth contribution is now mid - prestige -led – Royal Challenge (+2.9%) and Signature (+1.2%) offset McDowell's 0.6% drag in CY25. RDCK’s P&A volume growth contribution is led by two key brands – Magic Moments at 7.5% and After Dark sharing 9.5%. McDowell's No 1 declined 0.9% YoY in CY25 due to adverse excise duty in Maharashtra and could stage a recovery in H2CY26. Mid - prestige (Royal Challenge) continued to drive growth. UNITDSPR is our top sectoral pick, supported by India -UK FTA -led volume growth and margin rise (bulk scotch), recovery at MCD, and the potential for a special dividend from the sale of its IPL franchise. For RDCK, P&A growth continues – Magic Moments grew 15 -16% (led by flavor innovation), After Dark doubled its volume in CY25, and Old Admiral overtook Mansion House. We see FY27E growth at 17% (guidance 15%+). For ABDL, ICONiQ White is approaching 10mn cases (2x YoY), gaining share from MCD and IB, led by its sharp deluxe positioning. Recent management changes at ABD could sharpen the focus on P &A, helping arrest the drop in OC and SRB brands. For TLNGR, we see two monitorables in FY27 ; Mansion House's growth continues to lag Old Admiral, while the recently acquired Imperial Blue, down 11% YoY, will require attention to revive growth. Expect premiumization to continue (select performances in mass brands). We raise RDCK’s TP to INR 4,100 (from INR 3700), as we roll -forward to Sep -28E, on 48x (unchanged) P/E.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

600-400.jpg)

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...