Finance Sector Update : LCR and NSFR headroom to support healthy credit growth by Motilal Oswal Financial Services Ltd

LDR ratio can increase 3-12% across our coverage banks; PSBs to benefit more

* The RBI MPC highlights that bank liquidity assessment is increasingly driven by the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) rather than the Loan-to-Deposit Ratio (LDR). As the system moves away from deposit-linked reserves, LDR’s relevance as a standalone liquidity indicator has diminished.

* Under the LCR and NSFR frameworks, liquidity buffers are calibrated based on total liabilities, not just deposits. Since funding is sourced from deposits, borrowings, and equity, banks can maintain higher LDRs without compromising liquidity resilience.

* The LCR-NSFR framework is structurally more supportive of growth and profitability than LDR. By focusing on stress liquidity and funding stability, it enables asset expansion without one-for-one deposit growth, allowing banks to optimize balance sheets and enhance returns.

* Under the LCR and NSFR frameworks, surplus liquidity and stable funding can be redeployed into loans without a corresponding increase in deposits, theoretically raising LDRs by ~3-23% based on both methods. PSU banks emerge as key beneficiaries, possessing greater liquidity deployment headroom than large private banks. Using a conservative approach—taking the lower end of gains from LCR and NSFR optimization—the LDR can theoretically increase by 3–12% across banks.

* We thus note that this optimization of LDR and NSFR could enable an incremental ~7% credit expansion for the system, assuming deposits remain constant. Consequently, the system-wide LDR could theoretically increase to ~89% from the current ~82%.

* Our top picks: ICICI Bank, HDFC Bank, SBI, and AU Bank.

LCR and NSFR gaining significance over LDR

The RBI, in its MPC conference (Link), suggested that LDR is not the sole factor to determine the banking system's ability to pursue loan growth; liquidity is more important, as assessed by the LCR and NSFR framework. Thus, the relevance of the LDR needs to be re-evaluated in the context of the evolving regulatory architecture with respect to the evaluation of a bank’s liquidity. Historically, LDR was a meaningful indicator because reserve requirements, CRR, and SLR were explicitly linked to deposit liabilities. In that regime, higher LDRs directly implied thinner liquidity buffers and raised concerns around solvency during periods of stress. However, the recent communications by the RBI indicate that the Indian banking system is transitioning to a framework dominated by LCR and NSFR, where reserve creation is no longer deposit-centric. This structural shift materially weakens the signaling power of LDR as a measure of balance sheet liquidity.

Liquidity buffers now centered on total liabilities, not deposits alone

Under LCR and NSFR, banks are required to maintain sufficient high-quality liquid assets and stable funding against estimated outflows and asset books, respectively. Crucially, these buffers can be created using a combination of deposits, wholesale borrowings, and equity capital. This means that incremental loans do not need to be matched one-for-one with incremental deposits. As long as a bank maintains adequate LCR and NSFR, it can operate with a higher LDR without compromising liquidity resilience. In this context, focusing narrowly on loans-to-deposits risks ignores the broader funding flexibility embedded in modern bank balance sheets.

LCR-NSFR framework: More supportive of growth and profitability

Moving away from LDR as a binding constraint helps expand banks’ growth runway. LDR has been a more static indicator and completely hinged on deposits, ignoring the dynamic nature of the market, such as the stress period liquidity requirements and the funding stability. LCR and NSFR reframe this by focusing on stress liquidity (30 days) and funding stability (one year), enabling asset growth without one-forone deposit expansion. A shift toward LCR–NSFR-led balance-sheet management allows banks to optimize their balance sheets by unlocking assets, thus supporting credit growth and underlying profitability

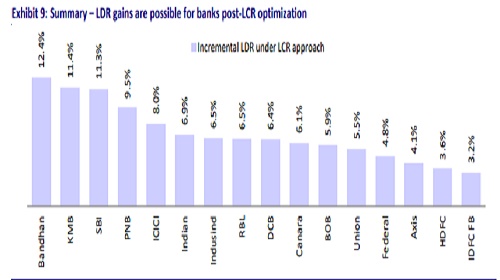

Excess liquidity deployment may theoretically drive a 3-12% increase in LDR

Unlike LDR, which implicitly links lending capacity only to deposits, the LCR framework creates liquidity buffers from the entire liability base – deposits, borrowings, and equities. As the bank maintains the targeted LCR cushion above regulatory minima, surplus liquidity parked in low-yielding assets can be redeployed into loans without requiring incremental deposit mobilization, thereby supporting loan growth. Based on the outstanding LCR of our coverage banks, we reckon that the transition to an LCRbased framework to assess liquidity and growth potential will enable 7% growth in banking credit as banks deploy the excess liquidity on the balance sheet. LDRs could thus theoretically increase by 3-12% across our coverage universe, with PSU banks emerging as the key beneficiaries. Large private banks may see a relatively lower LDR uplift of 4-11%, while PSU banks will have the highest gains of 6-11%.

NSFR optimization can lift LDR by 3-23%; PSU banks again better positioned

Optimization under the NSFR framework can help raise LDRs by ~3-23%, with PSU banks being better positioned given their surplus stable funding buffers. By focusing on one-year funding stability, NSFR allows banks with ratios well above 100% to redeploy excess Available Stable Funding (equity, long-term borrowings, and stable deposits) into incremental loans without matching deposit growth. This excess can support incremental loan growth without a commensurate rise in deposits, pushing LDRs higher while preserving structural funding strength. Under this NSFR-based optimization, banks are estimated to witness a 3-23% increase in LDR. The analysis continues to indicate that PSU banks remain the preferred segment (details inside), as they maintain higher NSFR ratios and will benefit more from surplus liquidity deployment.

Several global banks operate at an LDR>100%

Global banking systems operating under LCR and NSFR frameworks routinely function with LDRs at or above 100% without raising investor concerns. In these markets, analytical focus has decisively shifted away from simple deposit–loan matching toward stress liquidity coverage, funding maturity, and capital adequacy. As long as banks maintain strong LCR/NSFR buffers and healthy capital ratios, higher LDRs are viewed as an outcome of efficient balance sheet utilization rather than a measure of inadequate balance sheet liquidity and funding stretch.

Valuation and View

* The transition from an LDR-centric lens to an LCR–NSFR framework to assess the available lending headroom materially improves visibility on sustainable credit growth. Under LCR–NSFR, lending capacity is determined by overall liquidity buffers and stable funding, not deposits alone, reducing the structural constraint implied by elevated LDRs.

* As Indian banks increasingly operate and are viewed from this framework, similar to global peers, the concern that high LDRs will limit growth should gradually fade, supporting credit growth that can outpace deposits over time.

* Valuation differentiation is therefore likely to shift from headline LDRs to liquidity surplus, funding maturity profile, and capital strength. Large private banks, trading at ~1.8–2.3x FY27E P/BV with ~1.6–1.8% RoAs, remain well placed, as surplus LCR/NSFR cushions allow growth without funding constraints. This also opens room for PSU banks to narrow valuation gaps as surplus liquidity deployment improves growth outlook and potential returns.

* We believe that banks that are nimble and well-positioned to monetize excess liquidity under the LCR–NSFR regime are better poised to grow the balance sheet.

* Our top picks: ICICI Bank, HDFC Bank, SBI, and AU Bank.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

More News

Top Conviction Ideas: Real Estate & Building Materials by Axis Securities Ltd