CPI Inflation Increased to a 16-Month High of 3.9% in May by CareEdge Ratings

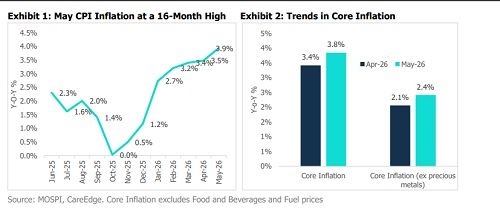

The CPI inflation has remained on an upward trend, inching higher to 3.9% in May from 3.5% in April. While CPI inflation came in lower than expected, it rose to its highest level in 16 months. A sharp increase in transport inflation and higher food inflation were the primary drivers of headline inflation during the month. Higher inflation in transport, restaurants & accommodation services, and precious metals pushed core inflation to 3.8%. Prices of precious metals rose in May despite a correction in the global prices. This was due to a hike in import duty and rupee depreciation. However, excluding precious metals, core inflation stood close to a benign 2.4% in May, implying that the current uptick in inflation is supply-driven rather than demand-driven.

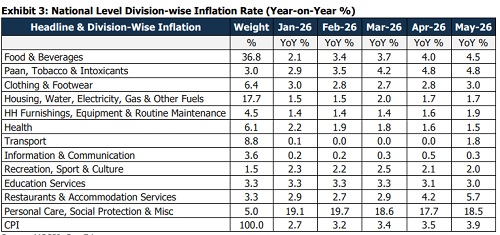

Food & beverage inflation increased to 4.5% in May (from 4% in April) as the favourable base effect from last year waned and a seasonal uptick set in. Heatwaves across several regions also adversely impacted the supply of several food items, pushing up the inflationary pressures. Amid the elevated global energy costs, the price of a 19 kg commercial LPG cylinder has witnessed several hikes since the onset of the West Asia conflict. Cumulatively, commercial LPG cylinder prices have risen by around Rs 1,200 so far. Inflation in restaurants & accommodation services inched up to 5.7% in May from 4.2% in April. Against the backdrop of rising fuel and food costs, this suggests that restaurants may be passing on part of the increase in input costs to consumers. Furthermore, retail fuel prices have been adjusted upward, with petrol and diesel each witnessing a cumulative hike of approximately Rs 7.5 per litre. As a result, transport inflation increased sharply to 1.8% in May, compared to the marginal deflation of April. We estimate that the cumulative increase in retail fuel prices following the conflict in West Asia has a direct impact of around 35 bps on headline CPI inflation. Indirect inflationary pressures may add another 10–15 basis points to overall CPI inflation. Despite the recent increase in retail fuel prices, there remains further scope for upward revisions, depending on the trajectory of global crude oil prices. This could exert upward pressure on fuel inflation going forward.

Way Forward Looking ahead, the global inflation outlook faces risks from external uncertainty and weather-related disruptions. While the government has already begun passing on the impact of higher global energy prices to consumers, there remains scope for further upward revisions. There could be a faster pass-through of prices to consumers, given the much higher levels of WPI inflation. On the domestic front, there are challenges due to below-normal rainfall, with a chance that El Niño conditions will develop during the monsoon season. India remains relatively better placed with higher reservoir levels and robust foodgrain buffer stocks compared to the past El Niño years. Nevertheless, food items, especially vegetables, pulses and edible oils, could witness upward price pressures. Factoring in these aspects, we project CPI inflation to average at 5% during FY27, assuming global crude oil prices average at USD 90/bbl during the year. The recent correction in energy prices following the positive developments around the West Asia crisis is favourable for the inflation outlook. However, the situation remains fluid and needs to be monitored.

Above views are of the author and not of the website kindly read disclaimer