Buy Siemens Energy India Ltd for the Target Rs. 3,800 by Motilal Oswal Financial Services Ltd

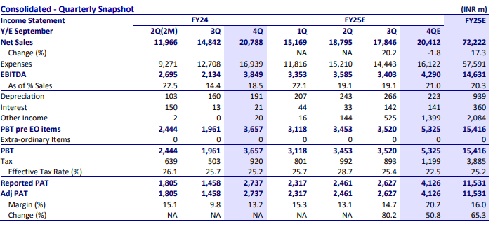

* We expect revenue to decline 2% YoY on a high base.

* Key monitorables include the status of capacity expansion, HVDC orders and margin trajectory.

* T&D sector ordering and execution ramp-up on commissioning of additional capacities will be in focus.

* We expect EBITDA margin to expand ~250bp YoY, with sequential improvement expected in power transmission and generation on better pricing.

* TP was increased to INR3,800 to factor in better execution.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Indian General Insurance Sector Update : Industry GWP YoY growth improves to 17% YoY by Moti...