Buy Park Medi World Ltd for Target Rs. 320 by Choice Institutional Equities

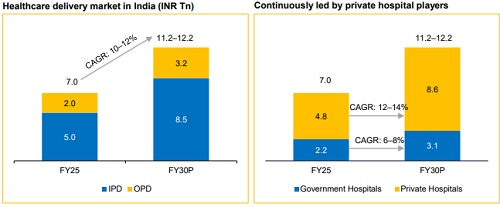

Aggressive capacity expansion with lowest capex per bed: PARKHOSP is executing one of India's most capital-efficient hospital expansions, scaling up from 3,960 beds today to eventually 5,460 by FY28 and doubling to over 10,000 beds in the following 5 years. The entire rollout is self-funded through internal accruals, with zero equity dilution. The cluster model delivers capex of just INR 34Lakh/bed against INR 80–100Lakh/bed for greenfield peers, without compromising NABH accreditation, robotics or ICU standards. Upfront payment for acquisitions of distressed assets secure valuation which competitors structurally cannot match. The bed configuration of 40% general ward, 30% ICU/critical care, 20–22% twin-sharing and remainder single rooms, maximises bed density per square foot. With a de-risked pipeline and a selfsustaining cash engine, PARKHOSP's compounding trajectory remains firmly intact.

Shift towards high-end case mix and optimising ALOS: PARKHOSP is executing a purposeful, multi-year clinical upgrade which remains in its early innings. Internal Medicine's structural retreat to ~30% is being systematically replaced by highacuity, high-margin specialties, anchored by three fifth-generation da Vinci robotic systems, Meril Robotic and Robo lens. With robotic volumes running at just 20–25% of maturity benchmarks, the operating leverage ahead remains substantial. Simultaneously, ALOS compression and ARPOB expansion confirm genuine clinical efficiency gains. The full-time doctor model ensures institutional alignment, while HIS standardisation across facilities creates compounding operational advantages which deepen with scale. PARKHOSP's clinical flywheel is still accelerating

Improving payor mix and benefit from revised CGHS rate: PARKHOSP's 83% government payor mix is its most durable competitive moat, creating a dual-sided barrier which premium chains cannot breach downwards and standalone operators cannot sustain upwards. The CGHS rate hike of 12–15% (first in a decade) delivers a sovereign-guaranteed, cost-free revenue uplift of ~7.5% flowing directly to EBITDA. Full cascade percolation across ECHS, Railways and state governments by H2FY27 creates a clearly dated earnings inflection. Simultaneously, the payor mix is organically shifting, from 83%/17% towards 75%/25% government/private, compressing the collection cycle from ~5 months towards 3.5 months, structurally improving free cash flow conversion. With management conservatively guiding 7.5% CGHS benefit against an actual 12–15% hike, the FY27 EBITDA delivery above current guidance is a high-conviction expectation

Investment View: We expect Revenue/EBITDA/PAT to expand at a CAGR of 26.3%/27.1%/34.6% over FY26–29E. The growth will be driven by aggressive capacity expansion with low capex per bed, a shift towards a higher-end case mix, optimisation of ALOS, improvement in payor mix and gains from revised CGHS rates. Thus, we initiate coverage on PARKHOSP with a ‘BUY’ rating and a target price of INR 320, with an upside of 36.0%, by valuing the company at 18x EV/EBITDA on FY28E.

Optionality: Currently concentrated in North India, expansion into new regions would reduce concentration risk. An upgrade in case mix is expected to drive higher ARPOB.

Key risks: Possible delays in achieving synergies from acquisitions and probably slower-than-anticipated ramp-up of the new hospitals.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131