Buy Nippon Life India AMC Ltd for the Target Rs. 1,200 by Motilal Oswal Financial Services Ltd

An all-round beat

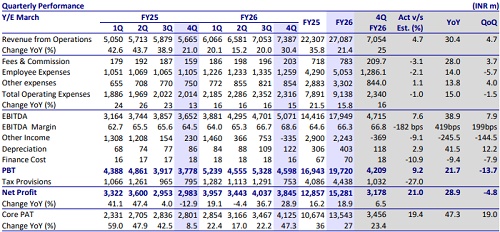

* Nippon Life India AMC’s (NAM) operating revenue came in at INR7.4b (5% beat) in 4QFY26, up 30% YoY/5%QoQ. For FY26, revenue grew 21% YoY to INR27.1b. Yield on management fees stood at 40.8bp in 4QFY26 vs. 40.7bp in 4QFY25 and 40.2bp in 3QFY26.

* Total opex came in at INR2.3b (in line), up 15% YoY but down 1.5% QoQ. 4Q EBITDA stood at INR5.1b (8% beat), up 39% YoY/8% QoQ, with EBIDTA margins at 68.6% (vs. 64.5% in 4QFY25). For FY26, EBITDA grew 25% YoY to INR17.9b with margin at 66.3%.

* 4Q PAT stood at ~INR3.8b (21% beat), up 29% YoY/down 5% QoQ. 4Q PAT margins stood at 52% vs. 52.7% in 4QFY25 and 57.2% in 3QFY26. For FY26, PAT grew 19% YoY to INR15.3b.

* The recent regulation (effective Apr’26) is expected to dent equity yields by ~3.5-4.0bp, though the impact will be fully passed on to distributors, limiting the effect on company profitability.

* We have maintained our earnings estimates to reflect stable AUM growth and better yields, offset by a slight increase in employee expenses. We expect a CAGR of 19%/15%/16%/16% in AUM/revenue/EBITDA/PAT over FY26-28E. We reiterate our BUY rating on the stock with a TP of INR1,200, based on 42x FY28E core EPS.

Market share across categories continues to expand

* Total MF QAAUM grew 30% YoY/3% QoQ to INR7.25t. Equity/ETFs/Index /Debt funds saw YoY growth of 23%/57%/21%/17%.

* The share of Equity/ETF/Debt/Liquid in total QAUM stood at 45.6%/33.4%/ 8.4%/9.5% in 4QFY26 vs. 47.6%/27.6%/9.3%/12% in 4QFY25.

* NAM’s market share in QAAUM rose 63bp YoY/24bp QoQ to 8.9% (highest), with equity market share rising 24bp YoY/3bp QoQ to ~7.2%.

* ETF market share continues to surge, rising 234bp YoY/109bp QoQ to 21.4%, with NAM maintaining a dominant position in this space at 45% of total industry folios and 52% of ETF trading volumes on NSE/BSE.

* Gold and silver ETF AUM stood at INR848b, growing 23% QoQ. Gold and silver ETFs accounted for 36% of ETF AUM and 12% of total MF AUM.

* SIP flows declined marginally to INR108.7b in 4Q from INR109.8b in 3Q, due to market volatility (in line with industry), reflecting monthly SIP inflows of INR36.2b (+12% YoY). The SIP book grew to INR1.5t (+17% YoY). SIP market share inched up to 9.84% as of Mar’26 from 9.82% in Dec’25.

* Total opex came in at INR2.3b (in line), up 15% YoY and down 1.5% QoQ. As bp of QAAUM, the cost stood at 12.8bp in 4QFY26 vs. 14.5bp in 4QFY25 and 13.4bp in 3QFY26.

* Employee costs rose 14% YoY/fell 6% QoQ to INR1.3b. ESOP-related costs stood at INR110m in 4Q and ~INR430m in FY26. For FY27, it is expected to be ~INR350m. Total ESOP cost over the next four years is estimated at INR720m-750m, with a front-loaded impact in initial years. Other expenses grew 14% YoY/4% QoQ to INR854m.

* Non-ESOP expense growth guidance remains at ~15-16% YoY. Management expects operating leverage to play out as AUM scales up, leading to a gradual decline in cost ratios over time.

* Loss from other activities stood at INR335m (in line), impacted by MTM effect.

* In the investor mix, the retail share stood at 49% in 4QFY26 (vs. 50% in 4QFY25), while HNI/corporate share stood at 37%/14%.

* Cumulative AIF commitments stood at INR93.3b (+26% YoY). During 4QFY26, INR4b was raised. Credit Opportunity Fund Series II was launched and achieved the first close in 4Q, with 25% capital deployed.

* Offshore AUM stood at INR1.4b. The company continues to expand across Europe, Asia, and Latin America. Under the advisory segment, AUM declined to INR17b from INR20b in 4QFY25.

* In Gift City, two feeder funds are operational, with combined AUM growing to USD38m. Future product pipeline includes Digital Innovation Fund 2B: Fund of Funds, which shall invest in India-focused venture capital funds.

* Digital purchase transactions contributed 77% of total new purchase transactions. The company recorded its highest-ever monthly transactions of 1.8m in Jan’26.

* NAM has the largest investor base in the industry with 23.8m unique investors and a market share of 38.8%. It added 2.7m folios QoQ, taking the total to 39.4m.

Key takeaways from the management commentary

* Equity net sales market share and equity AUM market share remained in high single digits and above overall market share. The company achieved high singledigit market share in equity and hybrid net sales. Adjusted for NFO-related flows, equity net sales market share would be in double digits.

* SIP trends are stabilizing after a temporary slowdown, with signs of recovery visible in Mar’26. The company has started building SIP books in new categories as well, particularly in hybrid funds and commodity-based funds. It focuses on growing in categories, including flexicap funds and sector/thematic funds.

* SIF is being viewed as a strategic long-term growth opportunity. Significant backend work and product development are underway. The focus is on creating differentiated offerings rather than incremental MF-like products.

Valuation and view

* NAM remains the fastest-growing AMC among India’s top 10 AMCs, gaining market share across segments—particularly in passive—driven by strong flows, sticky investors, and launches across segments. Recent regulations may dent its equity yields by ~3.5-4bp, though management expects to offset this impact by passing it on to distributors, limiting any P&L impact.

* We have maintained our earnings estimates to reflect stable AUM growth and better yields, offset by a slight increase in employee expenses. We expect a CAGR of 19%/15%/16%/16% in AUM/revenue/EBITDA/PAT over FY26-28E. We reiterate our BUY rating on the stock with a TP of INR1,200, based on 42x FY28E core EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412