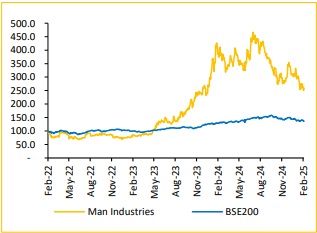

Buy Man Industries Ltd For the Target Rs.409 by Choice Broking Ltd

Revenue below street expectations, while EBITDA improved backed by better product mix.

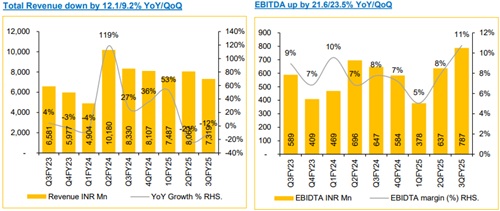

* Q3FY25 consolidated revenues came at INR 7,319 Mn, (vs CEBPL est. INR 10,384 Mn), down 12.1/9.2% YoY/QoQ.

* Consolidated EBITDA for Q3FY25 was reported at INR 787 mn, (vs CEBPL est. INR 751 Mn), up 21.6/23.5% YoY/QoQ and EBITDA margins improved by 299bps to 10.8%.

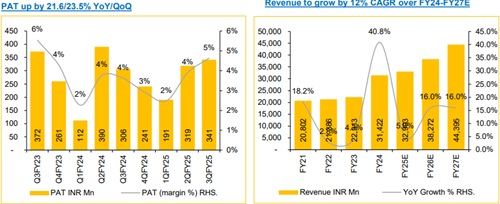

* PAT for Q3FY25 reported at INR 341 Mn, (vs CEBPL est. INR 389 Mn), up 11.5/7.1% YoY/QoQ. EPS for the Q3FY25 came in at INR5.3.

Guides 20% Revenue growth for FY26 :

Management aims for a 20% YoY revenue growth to INR 40,000 Mn for FY26 supported by strong order book of INR 29,000 Mn as on Feb 25 and heathy volume growth of 20 to 25%. For FY25 targeted revenue of INR 33,000 Mn, appears achievable. The company has achieved a revenue CAGR of 15% over FY21-24.

Capex on completion stage:

The company is making two major investments to expand production capacity, with a total capex of INR 4,500 Mn for the Jammu project (20,000MT capacity) and INR 7,000 Mn for the Saudi project (300,000MT capacity). These additions will increase the total production capacity by 171% to 3,20,000MT by Q3 FY26. Management expects these new facilities to contribute approximately INR 15,000 Mn in revenue during the second half of FY26, with the full impact materializing in FY27. Production at both plants is set to commence in Q3FY26. The Jammu plant will focus on high-demand products such as stainless steel (SS) pipes and ERW pipes, strengthening the company’s market position while also driving a margin improvement of 100-150 bps over the next two years.

View and Valuation:

We revise our FY25/26/27 EPS estimates downwards by -11.6%/6.6%/-1.4%, whereas outlook remains strong due to higher revenue growth and margin guidance. We maintain our ‘BUY’ rating with revised target price of INR 409, valuing the company at 12x (vs 15x) FY27 EPS. We expect volume growth of 20 to 25%, driven by healthy order book. Additionally, the revenue contribution from the Jammu and Saudi plant is expected to further drive the company's growth.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131