Buy Godrej Consumer Ltd for the Target Rs. 1,400 by Motilal Oswal Financial Services Ltd

Expectation building up for 2HFY26

* Godrej Consumer’s (GCPL) consolidated revenue rose 4% YoY to INR38.3b (est. INR39.3b), while volume growth stood at 3%. EBITDA declined 4% YoY (est. -5%) due to soft margins for the Indian and Indonesian operations.

* India’s revenue rose 4%, while volume grew 3%. The GST transition’s impact was 3-4%. Excluding soaps, volume growth was in double digits. Home Care delivered 6% revenue growth. GCPL entered the Toilet Cleaner space (INR30b market, growing at a strong double digit) with the launch of Godrej Spic Toilet Cleaner in October in South India.

* The Personal Care portfolio’s sales declined 2% YoY. The Personal Wash and Hair Color categories were adversely impacted by the GST-led supply disruption. Two-thirds of the Soaps portfolio experienced grammage increases, while the rest saw price cuts. GCPL has entered the men’s facewash category (valued at INR10b and growing at ~25% YoY) through the acquisition of the ‘Muuchstac’ brand for ~INR4.5b.

* International revenue rose 5%, led by a 25% growth in GAUM. Indonesia and LATAM declined ~7% and ~9%, respectively. Indonesia’s performance was impacted by weak economic conditions, changes in distributor arrangements, and increased competition.

* India’s EBITDA declined 7% YoY, impacted by sustained GM pressure (440bp down). GCPL stated that Indian margins have bottomed out, and 2HFY26 margins are expected to be at the lower end of its guidance of 24-26%.

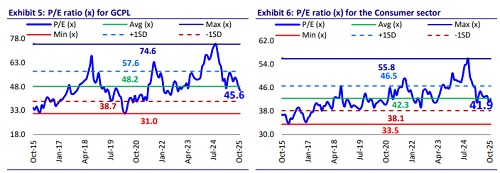

* The Indian business is witnessing a gradual recovery, with a steady 1H performance reinforcing confidence in an improving trajectory toward accelerated volume growth. With easing palm oil prices, the company is well-positioned for margin recovery in 2HFY26, supporting overall profitability. This combination of volume traction and margin tailwinds strengthens earnings visibility. We model 10%/12% revenue and EBITDA CAGR for FY25-28E. The company is expanding its TAM by foraying into new, faster-growing categories and continues to strengthen its core portfolio. Given the growth-centric focus, we remain constructive on GCPL and reiterate our BUY rating with a TP of INR1,400 (based on 50x Sep’27E EPS).

India’s (ex-Soap) UVG in double digits; pressure on margins continues

Consolidated performance

* Steady volume growth: Consolidated net sales grew 4% YoY to INR38.3b (est. INR39.3b). Consolidated volume growth was 3%.

* Continued pressure on margins: Gross margins contracted 350bp YoY to 52.1% (est. 52.2%). EBITDA margin contracted 160bp YoY to 19.2% (est. 18.4%). Other expenses rose 2% and ad spends rose 3%, while employee expenses declined 13%.

* Miss on profitability: EBITDA declined 4% YoY to INR7.3b (est. INR7.2b). PBT was at INR6.5b (est. INR6.7b), declining 9% YoY. APAT declined 3% YoY to INR4.8b (est. INR5b).

* In 1HFY26, consolidated revenue/EBITDA/APAT grew 7%/declined 4%/declined 1%.

* International performance: Indonesia delivered 2% UVG, with sales declining 7% in CC and INR terms and EBITDA declining 6%. The company expects pricing pressure to ease in a few months. In Indonesia, Hair Colours continued its strong performance, delivering double-digit growth led by Shampoo Hair Colour. Baby Care continued to gain market share. GAUM revenue grew 25%. GAUM EBITDA grew 20%. The strong growth was led by Hair Fashion and the scale-up of Air Fresheners. In GAUM, Aer Pocket maintained its strong traction for the second consecutive quarter across markets. The Hair Care range continued to deliver strong double-digit growth across Africa.

* Standalone performance: Net sales (including OOI) grew 4% YoY to INR23.6b in 2QFY26. The Indian business reported underlying volume growth of 3% YoY. Excluding soaps, India’s UVG growth was in double digits. The Home Care business registered robust 6% revenue growth, while Personal Care posted a 2% decline. Gross margin contracted 510bp YoY to 51.3%. Gross margin contracted 440bp YoY to 51.6%. GP declined 4%. EBITDA margin contracted 250bp YoY to 21.7% (est. 20.8%). EBITDA declined 7% YoY to INR5.2b.

Highlights from the management commentary

* The transition following the recent GST rate reduction led to short-term trade disruptions, as channels adjusted to new pricing and cleared old inventory, particularly impacting Soaps and Hair Colour. Despite this, GCPL continued to gain market share in Soaps and other key categories. Demand is expected to normalize in the coming months as trade channels stabilize.

* The GST rate reduction caused short-term trade disruption. Management has quantified ~3-4% hit to the standalone topline for the quarter, driven by destocking and channel price adjustments.

* Palm oil has been volatile but range-bound (~4,000–4,500 MYR recently). The company states that it is largely priced for current levels and does not anticipate any material additional margin pressure from palm oil at current prices. Adequate domestic refined palm availability and favorable pricing further support margins.

* Management expects the Indian standalone business to achieve high single-digit underlying volume growth for the year, alongside consolidated high single-digit revenue growth, with 2HFY26 anticipated to outperform 1HFY26.

Valuation and view

* We cut our EPS estimates by 2-3% over FY26-FY28 on account of a miss on margin.

* GCPL faced supply chain disruptions in its Indian business during the quarter due to GST rate revisions, which impacted sales. However, as palm oil prices ease, the benefits of this decline are expected to flow through in 2HFY26.

* The company is expanding its TAM by foraying into new, faster-growing categories and continues to strengthen its core portfolio. Besides, the company has made consistent efforts to address gaps in profitability and growth across its international business. Given the growth-centric focus, we remain constructive on GCPL and reiterate our BUY rating with a TP of INR1,400 (based on 50x Sep’27E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412