Buy Equitas Small Finance Bank Ltd For Target Rs.77 by Motilal Oswal Financial Services Ltd

Navigating through uncertainty

Near-term credit cost to stay high; RoA to recover to 1.5% by FY27E

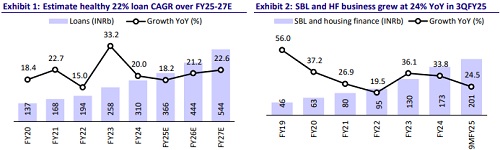

* EQUITASB has delivered a strong business growth trajectory, with a 26% CAGR in its loan book and 38% CAGR in deposits during FY22-24. This growth has improved the bank's CD ratio from 102% in FY22 to 87% currently, with the retail deposit mix standing at a healthy 67%.

* Margins have declined ~100bp YoY to 7.39% in 3QFY25 due to rising funding costs and high interest reversals along with a shift to secured products. Notwithstanding near term pressure on margins we expect medium term trajectory to remain steady benefitting from stabilization in funding costs, rationalization in SA rates while fixed rate nature of loan book (~80% of loans being fixed-rate) support yields in a declining rate environment.

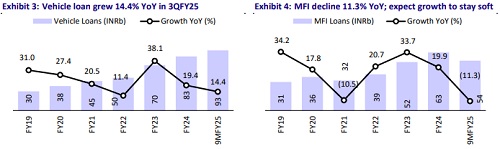

* The ongoing stress in the MFI segment has impacted profitability and will keep credit costs elevated in near term. CE across states has been showing improvement (barring Karnataka which accounts for 10% of bank’s MFI book) while Vehicle and SBL businesses are doing well. We thus expect overall credit cost to moderate to 1.5% by FY27E vs 3.1% in FY25.

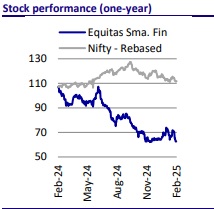

* The stock has corrected 43% since Jan’24 and now trades at 1.0x Sep’26E ABV. Healthy growth momentum with an estimated loan CAGR of >20% and a gradual recovery in profitability with RoA recovering to ~1.5% by FY27E will support stock performance in the medium term. We retain our BUY rating on the stock with a revised TP of INR77 (1.3x Sep’26E ABV).

Growth outlook steady; MFI mix to decline further

EQUITASB reported 21% YoY loan growth in 3QFY25, driven by strong growth in small business loans (SBL) at 26.7% YoY. The bank remained cautious in MFI segment amid elevated stress. The bank is shifting its focus toward secured products and has reduced its MFI concentration to ~14% of AUM, with a further decline expected in the coming quarters. The bank is ramping up disbursements in the micro-LAP segment, focusing on the top 15% of its MFI customers and driving growth in affordable housing, used CVs, and SBL. The affordable housing book is expected to turn profitable by FY26. EQUITASB has launched personal loans for deposit customers this quarter and plans to roll out credit cards by Mar’25. We estimate the bank to deliver a 22% CAGR in advances over FY25-27, primarily fueled by secured segments.

CASA mix has declined sharply; retail deposit mix steady at 67%

EQUITASB has significantly scaled up its liability franchise, achieving a 30% CAGR in total deposits over the past four years. However, the CASA ratio declined sharply from 46.2% in 3QFY23 to 28.6% in 3QFY24, due to a wide rate differential between savings account (SA) deposits and term deposits (TDs), as depositors opted for TDs amid uncertainty over interest rates. Despite this, the retail deposit mix remains strong at 67%. The bank has adjusted its SA rates, focusing on the mass affluent and HNI segments. With a healthy CD ratio of 87% in 3QFY25, the bank is well positioned to deliver steady growth while trying to prevent any further erosion in CASA mix. We estimate a 21% CAGR in deposits over FY25-27 and expect CASA mix to improve to 31% by FY27E

NIMs to remain under pressure in near term; turn in rate cycle to offer some relief

EQUITASB has reported a ~100bp decline in margins over the past one year, standing at 7.39% in 3QFY25, due to rising funding costs and a shift from high-yield MFI loans to secured products. However, with stabilizing funding costs, a comfortable CD ratio of 86-87%, and its ability to moderate SA rates as the interest rate cycle turns, the bank is expected to maintain steady margins, especially as fixed-rate loans (~80% of the book) support margins in a favorable rate environment. The moderation in MFI mix may put pressure on portfolio yields; however, the bank is aiming to offset some impact by focusing on other highyielding segments, viz. used CV, micro-LAP, etc. The bank’s ongoing investments in branch expansion, digital infrastructure, and employees (strengthened its collection team) pushed the C/I ratio to 68.5% in 3QFY25. With continued investments, C/I ratio may remain elevated in the near term and gradually improve to ~64% by FY27E.

Asset quality stress (MFI) to linger in near term; credit cost to remain elevated

EQUITASB’s GNPA ratio rose to 2.97% in 3QFY25, driven by increased slippages in the MFI segment, which rose from 8.3% to 14.2% due to customer overleveraging. In contrast, the non-MFI portfolio showed improvement, with slippages falling from 2.3% to 1.1%. While stress in the non-MFI segment remains contained, the MFI segment continues to pose challenges, with the next two quarters being critical for managing credit costs and improving asset quality. The bank has strengthened its collections efforts by adding 1,000 employees. MFI stress is particularly pronounced in regions like Karnataka, where collection efficiency (CE) has dropped to 90% and the government intervention has created significant uncertainty in collection outlook. Despite these challenges, the bank’s continuous efforts to reduce MFI exposure (currently at 14% and expected to go down to single digits) and recovery in vehicle finance are expected to ease the slippage run rate in the medium term. We estimate a credit cost of 1.6% in FY27, which will reduce cyclicality in overall business.

Valuation and view

EQUITASB has demonstrated healthy growth, achieving a 26% CAGR in its loan book and a 38% CAGR in deposits over FY22-24. CD ratio has thus eased from 102% in FY23 to 87% in 3QFY25. Although ongoing stress in the MFI segment has impacted profitability, the bank's MFI exposure has declined to ~14% (from 28% five years ago). In order to reduce cyclicality in the business, the bank aims to further bring down the MFI mix over the coming years. EQUITASB has hired ~1,000 employees to boost CE, which has affected cost ratios, which we estimate will ease gradually over the coming years. The stock has corrected 43% since Jan’24 and now trades at 1.0x Sep’26E ABV. The bank’s sustained growth momentum with an estimated loan CAGR of 22% and a gradual recovery in profitability with RoA of 1.5% by FY27E will support stock performance in the medium term, especially as MFI segment regains stability. We retain our BUY rating on the stock with a revised TP of INR77 (1.3x Sep’26E ABV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412