Buy Adani Ports & SEZ Ltd for the Target Rs. 1900 by Motilal Oswal Financial Services Ltd

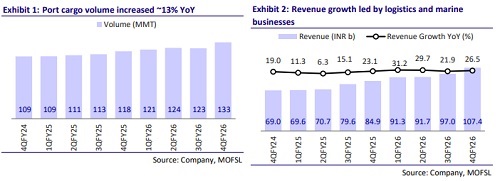

Adani Ports & SEZ (APSEZ) reported revenue growth of ~27% YoY to INR107b in 4QFY26 (12% above our estimate). Cargo volumes grew 13% YoY to 133.4mmt. This growth was primarily fueled by containers.

EBITDA margin was 56.1% in 4QFY26 vs our estimate of 58.8% (-290bp YoY,

-350bp QoQ). EBITDA grew ~20% YoY to INR60b (7% above our estimate), while APAT increased ~16% YoY to INR33b, aided by lower tax outflow.

The all-India cargo market’s share stood at 26% (vs. 26.3% in 4QFY25). The container segment’s market share stood at 45.2% (vs. 46.3% in 4QFY25).

Logistics’ revenue/EBITDA stood at INR11.3b (+10% YoY)/INR2.3b (26% YoY).

In FY26, revenue/EBITDA/APAT grew 27%/24%/26% on a YoY basis.

The Board announced a dividend of INR7.5 per share.

APSEZ posted a healthy performance in 4QFY26, meeting its full-year revenue and EBITDA guidance, driven by strong growth in international port operations led by the consolidation of NQXT and healthy traction in the marine business. The logistics segment also emerged as a key growth driver, aided by significant improvement in network scale and last-mile connectivity, thereby further strengthening the integrated port-to-logistics ecosystem.

Overall, supported by ongoing capacity additions and expansion into value-added segments such as logistics, the company remains well-positioned to outpace broader industry growth. We broadly retain our FY28 estimates and expect APSEZ to post 11% growth in cargo volumes over FY26-28. This would drive a CAGR of 17%/18%/22% in revenue/EBITDA/PAT over FY26-28E. We reiterate our BUY rating with a revised TP of INR1,900 (premised on 15x FY28E EV/EBITDA).

Performance led by strong growth in the international port segment

APSEZ handled 133.4 MMT of cargo in 4QFY26, up 13% YoY, driven by growth in container volumes. Mundra Port contributed 35%/42% to total volume/domestic volume in 4QFY26 (vs. 43%/51% in 4QFY25), marking diversification across ports.

Domestic cargo volume growth was flat and stood at 111.7MMT, while international cargo volume rose 262% YoY from 6MMT to 21.7MMT, driven by the consolidation of NQXT and Colombo terminals.

Revenue from domestic ports grew 8% YoY to INR65b, while EBITDA margins stood at 71.6% (vs. 71.8% in 4QFY25). Revenue rose 58% YoY to INR14.2b, and EBITDA grew 355% YoY, fueled by the consolidation of NQXT and better operations at the Colombo Port.

Logistics and marine businesses gain momentum

Logistics revenue rose 10% YoY to INR11.3b, driven by the recently launched asset-light Trucking and International Freight Network service. It handled 0.17m TEUs of container rail volume (-1% YoY) and ~5.6 MMT GPWIS volume (-5% YoY). APSEZ received approval to commence EXIM operations at Virochannagar (Gujarat), Kishangarh (Rajasthan), and Malur (Karnataka) ICDs.

The marine segment’s revenue jumped 101% YoY to INR7.3b, driven by a significant increase in vessel count from 76 (Jun’24) to 136 (Mar’26). The ramp-up reflects APSEZ’s aggressive expansion and consolidation in marine services.

As of Mar’26, APSEZ strengthened its integrated logistics network with a total rake count of 132. It operates 12 multi-modal logistics parks (MMLPs) and has expanded its warehousing capacity to 3.1m sq. ft. Agri silo capacity rose to 1.4MMT, with expansion already in place to take the capacity to 4MMT.

Key highlights from the management commentary

APSEZ experienced subdued dry bulk volumes across certain terminals, which impacted both overall volumes and margins during the period; however, management remains optimistic on a recovery in coal volumes, supported by expectations of a subdued monsoon and government directives for coal-based power plants to operate at higher utilization levels to meet rising power demand.

APSEZ maintained its target to handle ~1b MT cargo by FY31.

The company continued to deepen its international presence by commencing operations at the Colombo West International Terminal and completing the acquisition of NQXT Port in Australia, positioning itself for future growth in global trade corridors.

Logistics revenue rose 10% YoY to INR11.3b, driven by the recently launched asset-light Trucking and International Freight Network services (representing 52% of Q4 FY26 Logistics revenue vs. 48% in Q4 FY25).

The integration of its marine services business (including Ocean Sparkle, Astro, and TAHID) has been progressing well, and APSEZ achieved INR26.8b in FY26 marine business revenue vs. the 2x target from INR11.4b in FY25.

Management has given revenue and EBITDA guidance of INR430-450b and INR250-260b, respectively, for FY27.

Valuation and view

With strong cash flows, a healthy cash balance of INR122b, and net debt-to-EBITDA at 1.9x, APSEZ is well-positioned for further expansion. Capacity enhancements at key ports, ongoing infrastructure projects, and global port acquisitions provide visibility for sustained growth in FY27 and beyond.

We broadly retain our FY28 estimates and expect APSEZ to post an 11% growth in cargo volumes over FY26-28. This would drive a CAGR of 17%/18%/ 22% in revenue/EBITDA/PAT over FY26-28E. We reiterate our BUY rating with a revised TP of INR1,900 (premised on 15x FY28E EV/EBITDA).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041