Buy Motherson Sumi Wiring Ltd for Target Rs.48 by Choice Institutional Equities

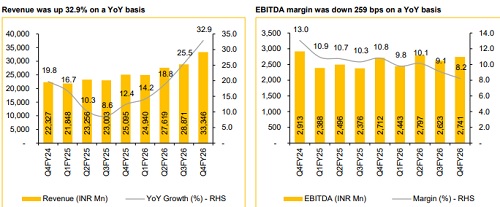

Structural Growth Intact; Margin Normalisation Awaited: MSUMI, led by new model launches and higher content per vehicle, delivered a strong 32.9% YoY revenue growth in this quarter, outperforming the industry average. However, gross margin was adversely impacted by elevated copper prices, resulting in a sequential margin decline of 293 bps. Additionally, margin was weighed down by start-up losses from greenfield plants. Despite these headwinds, MSUMI maintained a debt-free balance sheet supported by healthy cash flows. We believe EBITDA margin will remain under pressure due to commodity volatility and improve gradually from FY27E and strengthen further in FY28E as cost is passed on to customers, utilisation improves and operating leverage kicks in.

.

.

View and Valuation: We revise our FY27/28E EPS estimate downwards by 2.7%/0.9%, respectively, factoring in margin pressure, which will impact profitability. We maintain our target price at INR 48 on FY28E EPS. Considering the recent decline in the stock price, we upgrade our rating from ‘ADD’ to ‘BUY’.

Q4FY26: Revenue Beats Estimate; Margin Pressure Persists

? Revenue was at INR 33,346 Mn, up 32.9% YoY and up 15.5% QoQ (vs CIE est. at INR 28,745 Mn) ? EBITDA was up 1.0% YoY and up 4.5% QoQ to INR 2,741 Mn (vs CIE est. at INR 2,587 Mn). EBITDA margin was down 259 bps YoY and down 87 bps QoQ to 8.2% (vs CIE est. at 9.0%), led by higher raw material cost

? PAT was up 1.4% YoY and up 12.0% QoQ to INR 1,673 Mn (vs CIE est. at INR 1,521 Mn)

Expansion-led Capacity Ramp-up: The company’s greenfield plants in Gujarat, Pune and Kharkhauda (ICE, EV and hybrid platforms) are ramping up steadily. The plants are expected to achieve optimal utilisation in the next 2–3 quarters as volumes scale up. The management follows a disciplined expansion strategy, initiating new capacity as utilisation approaches ~80%. EBITDA at new plants is expected to improve sequentially as start-up cost declines and operating leverage kicks in, supporting margin recovery in the next few quarters.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131