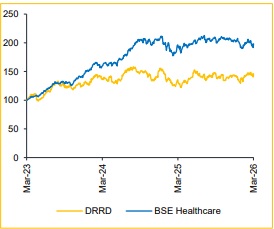

Add Dr. Reddy’s Labs Ltd for Target Rs.1,315 by Choice Institutional Equities

Early-mover Advantage Building Premium GLP-1 Franchise We interacted with DRRD’s Head of IR, Aishwarya Sitharam, following the company’s successful day-1 launch of Semaglutide. DRRD is the first to introduce a DCGI-approved version in India under the brand name Obeda, establishing an early-mover advantage in the domestic GLP-1 market. The company’s premium pricing at ~INR 4,200 per month versus peers at ~INR 1,300 reflects its dosage form, with a prefilled disposable pen format as compared to vial-based alternatives, which could support greater physician preference and patient stickiness. We view this launch as positioning the company strategically within the emerging GLP-1 opportunity, with a differentiated focus on quality, delivery format and brand trust rather than price-led competition. Overall, in the medium term, we expect a shift towards a more consolidated, quality-led market, with DRRD well-placed to benefit given its early entry and manufacturing strengths.

Key Takeaways from the Meeting

Product Positioning & Pricing:

* The premium pricing is primarily driven by the auto-injector pen format, which enables convenient self-administration.

* The management believes that pricing remains competitive when compared to other pen-based offering in the market.

* The company follows a “one product, one quality” approach, ensuring that Indian patients receive the same quality as global markets.

* The strong brand equity of DRRD is expected to drive both, doctor prescriptions and patient confidence.

Product Positioning & Pricing:

* The premium pricing is primarily driven by the auto-injector pen format, which enables convenient self-administration.

* The management believes that pricing remains competitive when compared to other pen-based offering in the market.

* The company follows a “one product, one quality” approach, ensuring that Indian patients receive the same quality as global markets.

* The strong brand equity of DRRD is expected to drive both, doctor prescriptions and patient confidence.

Strategy and Market Approach:

* The company’s strategy is focussed on building a long-term, sustainable franchise rather than aggressively chasing market share. ? The management has indicated that it is unlikely to engage in aggressive price cuts to drive volumes.

* The company is also targeting a potential approval in Canada around May 2026, subject to regulatory outcome. It is also one of the few Indian companies in the filing and review process. ? An early entry into the market could result in meaningful margin upside in the initial phase.

* A successful approval would also enhance global credibility and reinforce brand positioning.

Margin and Profitability:

* Margin for the product is expected to remain muted in the near term due to investments in brand building and field force expansion.

* Over the medium term, margin is expected to align with or exceed those of India-branded generics.

* Profitability is likely to improve as the business scales up and operating leverage kicks in.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131