Accumulate Asian Paints Ltd For Target Rs.2,700 By Elara Capital

Stability restored, growth improve

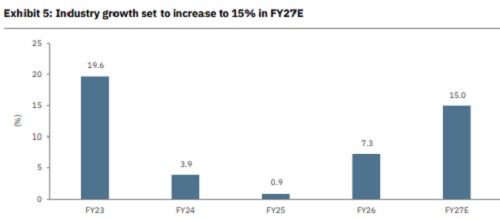

Asian Paints' (APNT IN) has endured prolonged underperformance due to two key headwinds: market share erosion and muted revenue growth. Its market share currently has stabilized at ~56% through 9MFY26, and we expect this to hold in Q4FY26. Industry revenue growth should accelerate to 15%+ in FY27E, fueled by price hikes of 6-8% across peers. Strong Summer demand, a late Diwali, and more wedding days could bolster volume. Near-term margin pressure persists but improving growth and market share underpin our stance upgrade. We upgrade to Accumulate with a higher TP of INR 2,700.

Input inflation to fuel revenue growth and operating leverage: A major investor concern has been whether rising competition would block the paints industry's ability to pass through raw materials inflation. Recent 6-8% price hikes by paint companies alleviate this concern. Crucially, paints category differ from other consumer categories: here, competitive intensity has primarily benefitted intermediaries, such as dealers and painters, not end-consumers. As these price hikes take effect, the industry’s price-value gap of ~5-7% reverses. We expect a double-digit price increase to lead to 15%+ revenue growth in FY27E, up sharply from ~5% revenue growth in FY26E for incumbents.

Large firms to gain share amid RM scarcity: Our channel checks with smaller paint manufacturers highlight shortages and cost spikes in key raw materials, such as titanium dioxide (TiO2) and styrene. Unorganized firms and smaller companies bear the brunt, lacking procurement scale. In contrast, large firms like APNT enjoy superior leverage to secure input material. This edge intensifies with the company’s new vinyl acetate monomer (VAM) and vinyl acetate ethylene (VAE) operational plant at Dahej, Gujarat, by Q1FY27. This backward integration shields against RM shortage and positions APNT to reclaim market share.

Market share stabilizes with revenue momentum: APNT’s market share fell to ~56% in FY26 from ~62% in FY24 but has stabilized in the past 2–3 quarters – a meaningful sign its corrective measures are working. The company has outperformed large peers on revenue growth for two consecutive quarters, ending a six-quarter slump. FY25 suffered from scheme cuts and inventory destocking. In FY26, APNT mirrored the industry’s subdued trends. In FY27E, we expect revenue growth to improve to 15%, driven by pricing aggression, industry tailwinds, and volume recovery.

Upgrade to Accumulate with a higher TP of INR 2,700: We upgrade APNT to Accumulate from Sell with a higher TP of INR 2,700 from INR 2,517. This reflects a roll-forward to March 2028E from Dec’ 2027E at 50x (unchanged) P/E. FY28 earnings should hold steady, assuming no prolonged geopolitical tensions and sustained market share. We have slightly reduced our FY27E and FY28E EPS estimates by 3.8% and 1.7% respectively. Key downside risk is delay in resolution of the US-Iran conflict or a sharp slowdown in the consumption from broader economic slowdown.

Please refer disclaimer at Report

SEBI Registration number is INH000000933