Writing & Printing Paper Realisations Strained by Imports and Geopolitical Risks by CareEdge Ratings

Synopsis

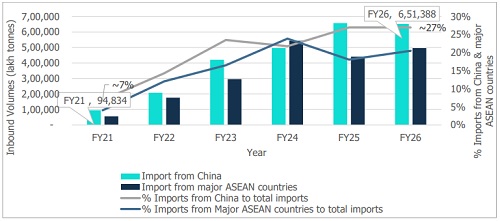

• India’s Writing & Printing Paper (WPP) industry continues to navigate a challenging environment, with realisations under pressure due to a sharp rise in low-priced imports and elevated raw-material costs. Key inputs such as hardwood pulp, domestic wood and wastepaper continue to inflate production costs. Further, the policy-related disparities have accentuated the structural cost disadvantages for the Indian paper manufacturers. Imports from China and ASEAN (Association of South-East Asian Nations) grew by over 80% between FY21 and FY26, reinforcing import-parity pricing.

• India sources a significant portion of its pulp requirements from countries such as China, the United States, Germany, Canada and Russia. At the same time, paper?related chemicals are largely imported from markets including China, Saudi Arabia, Singapore, Sweden and Sri Lanka—reflecting the sector’s reliance on global supply chains for critical inputs. In parallel, the escalation of the West Asia conflict has heightened volatility in freight and shipping costs, particularly due to disruptions to key trade routes, such as the Strait of Hormuz. Higher freight, war?risk insurance, and imported input costs are squeezing margins. At the same time, weaker demand in West Asia could redirect surplus global supply to India and intensify imports, likely keeping operating margins under pressure.

• The GST realignment in September 2025 has resulted in an inverted duty structure, thereby intensifying cost pressures for the Indian paper manufacturers. The GST exemption on notebook paper has eliminated input tax credit (ITC) eligibility for domestic manufacturers, while imports remain subject to zero IGST, exacerbating the cost disparity. At the same time, non?notebook WPP now attracts 18% GST (up from 12%), further distorting pricing. The absence of a uniform GST regime continues to weigh on domestic competitiveness and margins

• Despite these pressures, demand has remained stable, supported by steady education-linked consumption, NEP (National Education Policy) driven curriculum updates, and ongoing government procurement. This has helped sustain volumes and capacity utilisation, even as net sales realisations (NSR) remain under pressure.

• Going ahead, the industry’s resilience will depend on tighter cost control and product-mix improvements. Companies are reducing power and fuel costs through RDF (Refuse Derive Fuel), biomass, waste heat recovery and captive renewable energy, while improving margins by shifting towards higher-value and premium grades. Education-linked paper demand continues to support volumes and capacity utilisation. Integrated, energy-efficient players are better positioned, while smaller companies remain exposed to market volatility. A sustained recovery will require clearer policy direction, including stricter quality enforcement on imports, anti-dumping duties, calibrated trade measures to address pricing distortions, and a more balanced GST structure.

Industry Overview

• India’s paper industry has an annual installed capacity of ~25 million tons, of which the WPP segment accounts for ~30%. While long-term growth in WPP demand is impacted by digitisation and the increasing use of electronic communication, baseline consumption continues to be supported by India’s large education Writing & Printing Paper Realisations Strained by Imports and Geopolitical Risks June 16, 2026 l Ratings 2 ecosystem, including NEP-linked curriculum requirements, along with rising enrolments and recurring institutional demand from schools, colleges, offices and commercial establishments

• Over recent years, domestic production capacity in WPP has remained largely unchanged, while consumption has expanded steadily. This divergence has increased reliance on imports, particularly after the resumption of normal economic activity post-pandemic and the availability of duty concessions under international trade agreements. In addition, the ongoing West Asia conflict remains a risk, with potential implications on exports, imports and logistics.

Demand–Supply Dynamics and Import Pressure

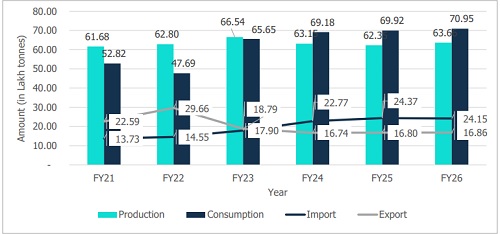

• Consumption of WPP increased from about 0.53 million tonnes in FY21 to nearly 0.71 million tonnes in FY26, while domestic production hovered within a narrow band of 0.62–0.64 million tonnes during the same period. This widening gap has been increasingly met through imports, which nearly doubled from around 1.37 million tonnes in FY21 to approximately 2.42 million tonnes in FY26, as detailed in Exhibit 1.

Exhibit 1: Production, Consumption, Import & Export trend of paper companies in India

Policy Factors and GST-Related Cost Distortions

• The GST realignment implemented in September 2025 has added to challenges because of an inverted duty structure. Notebook paper, which is used for exercise books and school notebooks, has been made GST-exempt, resulting in a loss of input tax credit (ITC) for domestic manufacturers. Imported notebook paper continues to enter India with zero Integrated GST, thereby widening the effective cost gap between imports and domestic production. In contrast, non-notebook WPP now attracts 18% GST (up from 12%), further distorting pricing within the WPP segment. Overall, the lack of a uniform GST structure continues to weigh on domestic competitiveness and margins.

• Industry bodies, including the Indian Paper Manufacturers Association (IPMA) and the Indian Agro and Recycled Paper Mills Association (IARPMA), have made repeated representations to the Ministry of Finance, GST Council and Ministry of Commerce seeking correction of the inverted GST structure, action against low-priced imports and policy support for fibre availability. While discussions are ongoing with an impending resolution, the GST distortion continues to weigh on the competitiveness of domestic WPP manufacturers

Exhibit 2: India’s paper imports from China and other ASEAN countries

Cost Structure: Raw-Material Inflation and Margin Pressure

• The WPP sector continues to face elevated input costs. Hardwood pulp prices have remained above USD 600/MT. In contrast, domestic wood prices have risen materially due to tight fibre availability and competition from allied wood-based industries such as Medium-Density Fibreboard (MDF). Wastepaper prices, although softer than peak levels, remain well above FY21 benchmarks.

• The WPP segment in India largely relies on wood-based fibre mix, with integrated mills typically using ~75– 85% hardwood, ~10–15% bamboo, and a limited ~5–10% wastepaper primarily for blending purposes. Wood remains the dominant input due to its superior fibre properties, which are required for strength, brightness and printability. At the same time, bamboo serves as a supplementary long-fibre source, and wastepaper plays a minor role in higher-quality grades. However, from an input–output perspective, recycled fibre (wastepaper) generally offers a higher pulp yield compared to fibres such as wood and bamboo, as it involves lower material losses during processing.

• The raw?material prices have remained elevated over the years (Exhibit 3, indexed to FY21 = 100), with visible fluctuations across key inputs. Wood prices have increased steadily, reaching an index level of 134.30 in FY26, indicating continued firmness in fibre costs. Wastepaper prices also show marked volatility—rising sharply to an index of 161.57 in FY22, easing to 113.17 in FY24, and climbing again to 144.40 in FY26. Bamboo prices exhibited a relatively stable but firm trajectory, moderating to 84.40 in FY24 before recovering to 101.80 in FY26. Since raw materials constitute the largest share of the WPP cost base (i.e., ~38–40% of the overall cost), this persistent, oscillating trend in input costs continues to compress gross margins.

Exhibit 3: Raw material price trends

Policy Factors and GST-Related Cost Distortions

• The GST realignment implemented in September 2025 has added to challenges because of an inverted duty structure. Notebook paper, which is used for exercise books and school notebooks, has been made GST-exempt, resulting in a loss of input tax credit (ITC) for domestic manufacturers. Imported notebook paper continues to enter India with zero Integrated GST, thereby widening the effective cost gap between imports and domestic production. In contrast, non-notebook WPP now attracts 18% GST (up from 12%), further distorting pricing within the WPP segment. Overall, the lack of a uniform GST structure continues to weigh on domestic competitiveness and margins.

• Industry bodies, including the Indian Paper Manufacturers Association (IPMA) and the Indian Agro and Recycled Paper Mills Association (IARPMA), have made repeated representations to the Ministry of Finance, GST Council and Ministry of Commerce seeking correction of the inverted GST structure, action against low-priced imports and policy support for fibre availability. While discussions are ongoing with an impending resolution, the GST distortion continues to weigh on the competitiveness of domestic WPP manufacturers.

West Asia Conflict: Emerging Export and Cost?Side Risks

• The ongoing conflict in West Asia has emerged as an additional external risk factor for the Indian paper industry, particularly on the export and cost fronts. Overall, paper exports account for ~26% of domestic production, indicating a moderate yet significant reliance on external markets and exposing the sector to global demand cycles and logistical disruptions. Ongoing disruptions to shipping routes through the Strait of Hormuz, following military escalation since late February 2026, have led to vessel diversions, booking suspensions and longer transit times, raising the risk of moderation in export volumes during FY27, particularly in Q1 and Q2.

• Elevated freight rates, war-risk insurance premiums, and higher prices of imported raw materials such as pulp, wastepaper and chemicals continue to exert pressure on operating margins. On the other hand, weaker exports from China and ASEAN countries may further accentuate surplus global supply, which may be diverted to India, thereby exposing WPP players to elevated risk.

Conclusion

“While freight and logistics disruptions arising from geopolitical tensions may prove transient, the WPP segment is expected to remain structurally challenged and any meaningful margin recovery will be contingent on tangible policy support, including GST rationalisation and stricter quality enforcement on imports, alongside continued progress in cost optimisation and backward integration,” said Puneet Kansal, Director, CareEdge Ratings.

“India’s writing and printing paper industry is under sustained margin pressure from low-cost imports, GST distortions and elevated input costs, with realisations unlikely to see a meaningful recovery in the near term. The ongoing West Asia crisis is further exacerbating freight volatility and supply-chain risks, adding to cost pressures even as demand remains resilient. As a result, while volumes may grow modestly, profitability for industry players, especially non-integrated ones, is likely to stay constrained, with resilience hinging on cost efficiencies and policy support,” said Priti Agarwal, Senior Director, CareEdge Ratings.

Above views are of the author and not of the website kindly read disclaimer